Risk-On Wave Sweeps Asia; Commodity FX Gains Ahead of Central Bank blitz – Action Forex

A powerful risk-on wave swept through Asian markets at the start of the week, propelling commodity currencies higher as equities across Japan and South Korea surged record while China jumped to decade highs. The mood reflected growing conviction that the U.S.–China trade conflict is entering a phase of lasting calm.

Following a “very good two-day meeting” between top officials in Washington and Beijing, U.S. negotiators hinted that additional American 100% tariffs on Chinese goods are now “effectively off the table.” That comment, combined with growing expectations for an extended tariff truce, eased concerns of a fresh escalation ahead of the Trump–Xi summit later this week.

In Australia, equities rose but underperformed their regional counterparts as rare-earth producers and explorers tumbled. Investors reacted to expectations that China will delay the rollout of its rare-earth export licensing regime — a move that could ease global supply tensions but dent near-term revenue prospects for Australian miners. Still, the broader regional risk tone remained overwhelmingly positive.

Attention will also center on the first major meeting between U.S. President Donald Trump and Japan’s new Prime Minister Sanae Takaichi. The pair are expected to discuss trade, security cooperation, defense spending, and investment — contentious issues that could shape the tone of U.S.–Japan relations under Takaichi’s leadership. Her diplomatic debut with the ASEAN summit in Malaysia and the APEC leaders’ meeting in Gyeongju, offering her a high-profile global stage early in her tenure. The Trump–Takaichi encounter is a potential swing factor for Japanese equities. A smooth discussion could reinforce investor confidence in Japan’s policy stability and extend the Nikkei’s record run.

Beyond geopolitics, this week also features a heavy central bank calendar. The Fed and BoC are both expected to cut rates, while the BoJ and ECB are seen holding steady. Traders will pay particular attention to whether the Fed, constrained by a data blackout from the ongoing U.S. government shutdown, signals that it remains on track for another back-to-back cut in December.

In the FX market, the tone aligns perfectly with the broader risk rally. Aussie leads gains, followed by Kiwi and Loonie. Safe havens are under pressure — Yen, Swiss Franc, and Euro are the weakest performers — while Dollar and Sterling hold middle ground.

In Asia, at the time of writing, Nikkei is up 2.12%. Hong Kong HSI is up 1.02%. China Shanghai SSE is up 1.04%. Singapore Strait Times is up 0.48%. Japan 10-year JGB yield is up 0.012 at 1.671.

Yuan surges as US-China move toward tariff truce framework

Chinese yuan rallied in Asian session after weekend reports signaled tangible progress toward a new U.S.–China trade framework. Senior economic officials from both countries agreed on the broad outline of a deal that could be finalized when Presidents Donald Trump and Xi Jinping meet later this week at the APEC summit in Gyeongju, South Korea. The accord aims to extend the existing tariff truce and suspend China’s planned rare-earth export controls, easing one of the key geopolitical risks that has hung over markets for weeks.

U.S. Treasury Secretary Bessent described the outcome of the fifth round of talks as “a very successful framework” for the leaders to discuss on Thursday, noting optimism that the tariff pause beyond its November 10 expiry is all but assured. He added that China is expected to resume substantial purchases of U.S. soybeans, ending a complete halt in September when Chinese buyers turned to Brazil and Argentina.

Bessent also said Beijing plans to delay by a year the rollout of its rare-earth licensing regime while the policy is reviewed. That concession effectively removes a major supply-chain concern for U.S. manufacturers in the short term.

Trump reinforced the upbeat sentiment, telling reporters he believes “we’re going to have a deal with China.”

The positive momentum coincided with stronger domestic data from China. Industrial profits surged 21.6% yoy in September, accelerating from 20.4% in August and marking the fastest pace since late 2023. The data lent further support to Chinese assets and Yuan, reinforcing the perception that policy stimulus and improving export volumes are feeding through to corporate earnings.

Technically, USD/CNH’s gap-down move today confirmed renewed downside momentum. The rejection by 55 D EMA (now at 7.1532) indicates the corrective bounce from 7.0843 has ended, with sellers regaining control. Break below 7.0843 would resume the broader downtrend from the April high of 7.4287 toward 61.8% projection of 7.2239 to 7.0843 from 7.1532 at 7.0669 next.

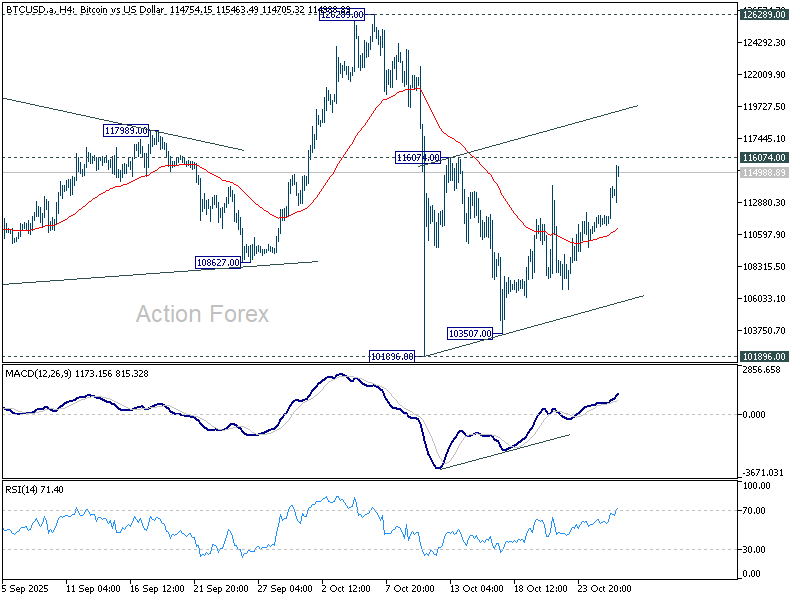

Bitcoin tests 116k resistance as risk-on rally builds in Asia

Bitcoin advanced notably today as risk appetite surged across Asia, with equity benchmarks in Japan and South Korea hitting historic milestones. Nikkei 225 jumped more than 2%, breaking above the 50,000 mark for the first time, while South Korea’s KOSPI surged 2.1% to cross 4,000. The broad rally reflected optimism that U.S.–China trade negotiations are progressing toward an extension of the tariff truce, fueling a powerful risk-on tone across regional assets.

Improving sentiment spilled over into digital markets, with Bitcoin rising in tandem with equities and commodities. Traders appear to be rotating back into higher-risk assets amid easing geopolitical tensions and steady global liquidity.

Technically, immediate focus is now on 116,074 resistance. Firm break above that level would confirm that the entire pullback from 126,289 represents only a consolidation to the five-wave rally from 74,373, rather than a larger scale correction. In that case, another rally toward 126,289 would be favored, though that prior high could still act as a cap within the range. Even if the consolidation extends with another downleg, the downside should remain contained above 101,896.

Conversely, rejection by 116,074 would undermine the range-bound view and raise the risk of a deeper slide below 101,896. While such a move would likely remain a correction, it would signal that the selling momentum has yet to fully exhaust.

Policy marathon: Fed and BoC to cut, BoJ and ECB to hold

Markets head into one of the busiest weeks of the year with a full slate of central bank meetings and top-tier data releases. Investors are bracing for decisions from the Fed, BoC, BoJ, and ECB — all set to test the durability of last week’s global risk rally.

The Fed meeting on Wednesday takes center stage. Markets have fully priced in a 25bps rate cut, which would bring the federal funds rate to 3.75–4.00%. Last week’s cooler CPI print reinforced expectations of a follow-up cut in December, with traders increasingly confident the Fed will stay on its easing path into early 2026.

A pre-CPI Reuters poll showed 71% of economists anticipated a December cut, and that figure likely rose after the inflation surprise. All eyes will turn to Jerome Powell’s press conference for subtle signals about how comfortable the Fed is with this dovish market path. He is expected to keep guidance deliberately vague, emphasizing data dependency and patience while steering clear of firm commitments.

North of the border, the BoC is also expected to deliver a 25bps rate cut this week, lowering its benchmark rate to 2.25%. While inflation has recently re-accelerated, growth momentum remains tepid and wage pressures are moderating, giving policymakers room to act. Around two-thirds of those surveyed in a Reuters poll expect the BoC to end the year at 2.25%, effectively reaching the lower limit of its 2.25–3.25% neutral band.

Looking further ahead, a majority of forecasters — roughly 60% — see the BoC holding rates at 2.25% through the end of 2026. Only a small minority expect deeper easing. That view underscores a growing belief that the current cycle is nearing completion.

In Asia, the BoJ is widely expected to stand pat at 0.50% this week. Most economists anticipate the next hike will come in December or January as officials gauge the new administration’s pro-growth policies. Reuters polling shows around 60% expect a move to 0.75% in Q4, rising to nearly full consensus by the end of March 2026. Markets will also pay close attention to the BoJ’s updated forecasts, which may reflect the positive spillovers from the U.S.–Japan trade agreement.

The ECB’s decision is expected to be a quiet one. Policymakers are set to keep the deposit rate steady at 2.00%. Investors view the October meeting as a placeholder, with December’s update — including new staff projections — likely to set the stage for 2026 guidance. Eurozone GDP and CPI flash data released this week could nonetheless shape rate expectations heading into year-end.

Beyond the central bank agenda, a packed data calendar will keep traders on alert. Key releases include, Eurozone GDP and CPI, Germany’s Ifo and Gfk sentiment, Australian CPI, Japan industrial production and Tokyo CPI, Canada GDP, and China PMIs. The convergence of these reports — alongside four central bank meetings — ensures an eventful week that could reset global market direction heading into November.

Here are some highlights for the week:

- Monday: Germany Ifo business climate; Eurozone M3 money supply.

- Tuesday: Germany Gfk consumer sentiment; US consumer confidence.

- Wednesday: Australia CPI; BoC rate decision; Fed rate decision.

- Thursday: New Zealand ANZ business confidence; BoJ rate decision; Swiss KOF economic barometer; Eurozone GDP; ECB rate decision.

- Friday: Japan Tokyo CPI, industrial production, retail sales, unemployment rate; Australia PPI; China PMIs; Swiss retail sales; Eurozone CPI flash; Canada GDP.

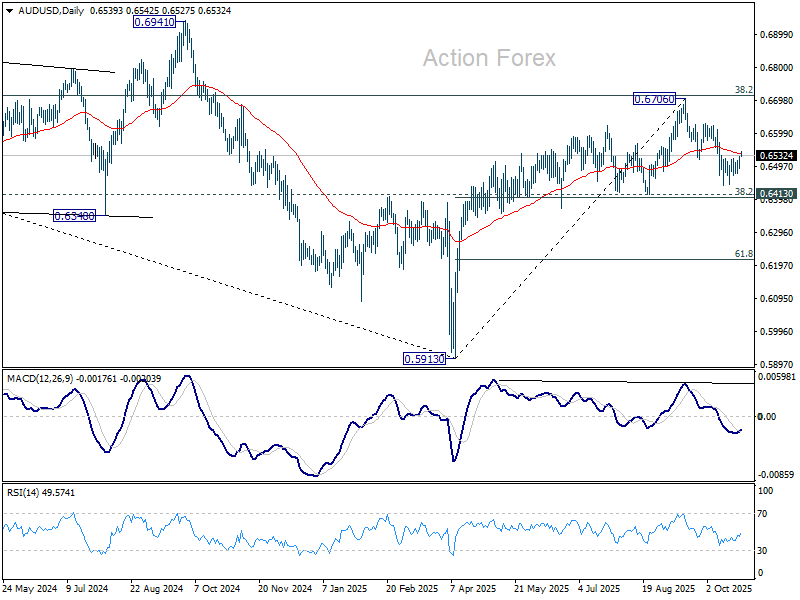

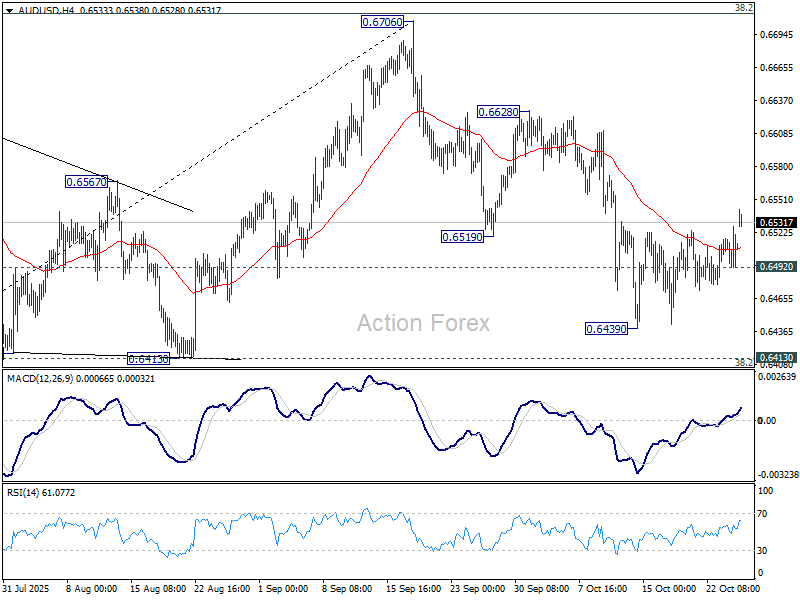

AUD/USD Daily Report

Daily Pivots: (S1) 0.6494; (P) 0.6511; (R1) 0.6530; More...

AUD/USD edges higher today and immediate focus is on 55 D EMA (now at 0.6538). Sustained break there will argue that fall from 0.6706 has completed as a three wave correction at 0.6439. Further rally should then be seen to 0.6628 resistance, and then retest 0.6706 high. On the downside, though, below 0.6492 minor support will turn bias back to the downside to resume the fall from 0.6706 to 0.6413 cluster support (38.2% retracement of 0.5913 to 0.6706 at 0.6403. Decisive break there will indicate bearish reversal after rejection by 0.6713 fibonacci level.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.