Dollar Rebounds on Hawkish Fed Cut, Momentum Capped by Trade Optimism – Action Forex

Dollar tried to rebound overnight after markets pared back expectations for a December Fed rate cut, but momentum faded quickly in Asia. Optimism over a thaw in U.S.–China relations quickly reversed the rally attempt.

Fed’s three-way split decision to cut the federal funds rate by 25bps to 3.75–4.00% was interpreted as slightly more hawkish than expected. While Governor Stephen Miran again voted for a deeper 50bps move—consistent with his persistent dovish stance—the surprise came from Kansas City Fed President Jeffrey Schmid, who dissented in favor of holding steady.

More importantly, Fed Chair Jerome Powell emphasized during his press conference that another rate cut in December is “not a foregone conclusion.” He added that there were “strongly differing views” among policymakers on how to proceed, reinforcing the notion that the policy debate is far from settled.

Following Powell’s remarks, Fed funds futures repriced swiftly, now implying roughly a 70% chance of another 25bps cut in December, down from 90% before the meeting. The adjustment suggests investors are reassessing the pace and extent of policy easing heading into 2026 amid ongoing inflation and employment concerns.

Meanwhile, the Trump–Xi summit produced tangible progress. US President Donald Trump declared that “we have a deal,” announcing a one-year agreement on rare earths and critical minerals and halving fentanyl-related tariffs on Chinese imports. Trump also confirmed that total tariffs on Chinese exports will be reduced from 57% to 47%. He added that he would visit China in April, while Xi is expected to visit the U.S. “sometime after that”.

Markets welcomed the outcome as a sign of easing trade tensions. Risk-sensitive currencies such as New Zealand and Australian Dollars leading gains. Kiwi was the day’s top performer so far, followed by Aussie and Swiss Franc.

Yen, meanwhile, weakened after the BoJ stood pat. Forecasts and language were largely steady. From a policy perspective, a December rate hike remains a 50/50 call, contingent on both incoming data and Prime Minister Sanae Takaichi’s approach to monetary normalization. Dollar was the second weakest major on the day, with Loonie rounding out the bottom three. Meanwhile, Sterling steadied after a bruising week and traded mid-pack with Euro.

Focus to the ECB later today, and it’s meeting later today, and it’s expected to deliver no change in rates and little new guidance. Policymakers are likely to reiterate that current policy settings are appropriate. The implications would be that the bar for any policy move—up or down—remains high.

In Asia, at the time of writing, Nikkei is down -0.43%. Hong Kong HSI is down -0.32%. China Shanghai SSE is down -0.32%. Singapore Strait Times is down -0.47%. Overnight, DOW fell -0.16%. S&P 500 fell -0.00%. NASDAQ rose 0.55%. 10-year yield rose 0.075 to 4.058.

BoJ holds at 0.50%, keeps gradual tightening bias intact

The BoJ left its overnight call rate unchanged at 0.50% as widely expected. The decision came by a 7–2 vote, with Hajime Takata and Naoki Tamura again dissenting in favor of a 25bps rate hike to move policy a little closer to neutral. The repeat split highlights the growing divergence within the board as policymakers debate how quickly to normalize monetary conditions.

In its quarterly Outlook Report, the BoJ made only marginal revisions to its forecasts, signaling that the economic and inflation outlook remains broadly stable. The bank raised its fiscal 2025 GDP forecast slightly from 0.6% to 0.7%, while projections for 2026 and 2027 were left unchanged at 0.7% and 1.0%, respectively.

On prices, the BoJ kept its core CPI forecast at 2.7% for 2025, 1.8% for 2026, and 2.0% for 2027. Core-core CPI (excluding both fresh food and energy) was nudged higher to 2.0% in 2026 from 1.9%, with other years unchanged (2026 at 2.8% and 2027 at 2.0%). The bank reiterated that underlying inflation is expected to reach 2% in the latter half of the projection period through March 2027, retaining language from July that risks to the inflation outlook remain “roughly balanced.”

The BoJ also reiterated that it would continue to raise its policy rate and adjust the degree of monetary support “in accordance with improvements in the economy and prices.”

New Zealand ANZ business confidence surges to seven-month high, green shoots emerging

New Zealand’s ANZ Business Confidence Index surged sharply in September, rising from 49.6 to 58.1, the highest level since February. Own Activity Outlook also improved modestly, up from 43.4 to 44.6, marking its strongest reading since April.

Inflation expectations, meanwhile, remained broadly steady. The share of firms expecting to raise prices over the next three months eased slightly from 46% to 44%. Those anticipating cost increases ticked up from 75% to 76%. One-year-ahead inflation expectations edged higher from 2.71% to 2.75%.

ANZ noted that “green shoots are emerging, particularly for interest-rate-sensitive sectors.” The bank highlighted stronger retail sentiment as evidence that the economy is beginning to warm alongside the spring season, with monetary easing and high rural incomes supporting regional confidence and broader recovery momentum.

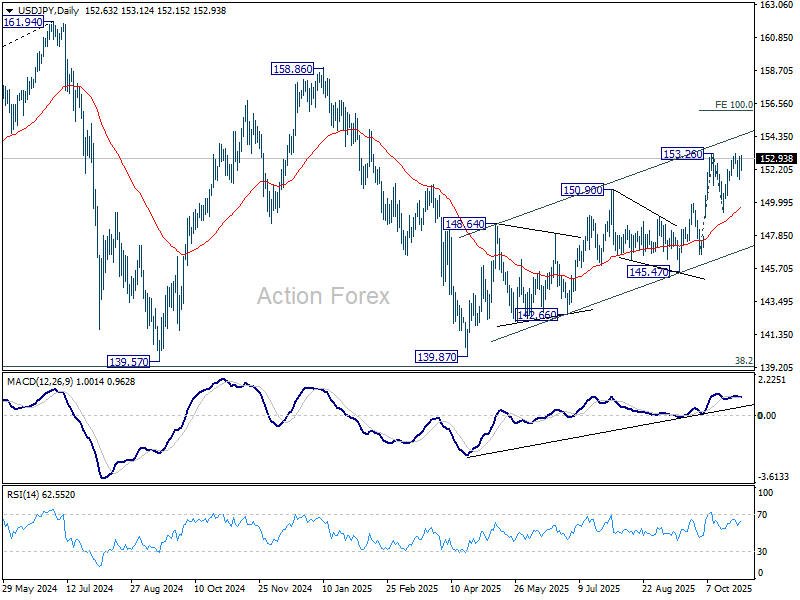

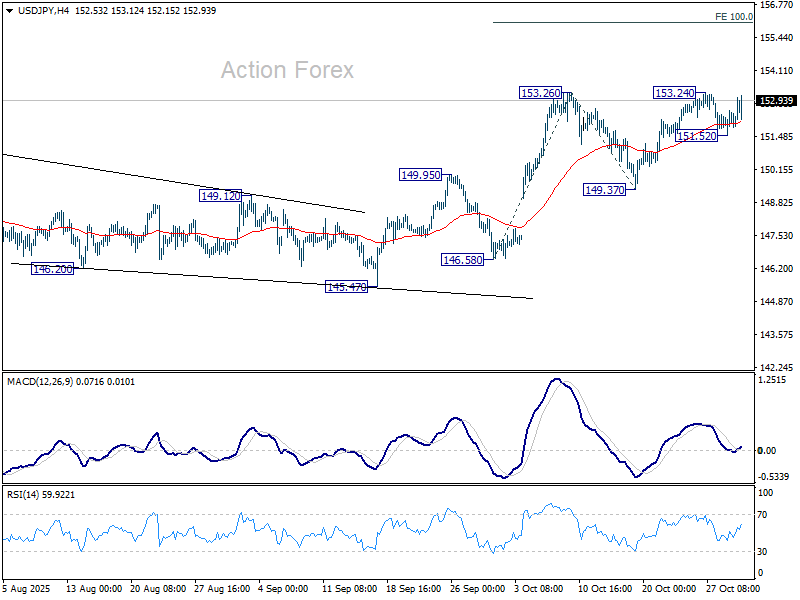

USD/JPY Daily Outlook

Daily Pivots: (S1) 151.83; (P) 152.45; (R1) 153.35; More…

USD/JPY’s rebound from 151.52 is still capped below 153.26 resistance and intraday bias remains neutral for now. On the upside, firm break of 153.26 will resume larger rally from 139.87. Next target is 100% projection of 146.58 to 153.26 from 149.37 at 156.05. However, break of 151.52 will extend the corrective pattern from 153.26 with another falling leg, and target 149.37 support instead.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.