AI Selloff Sparks Global Risk Rout; Yen and Dollar Stay Firm – Action Forex

Global markets tumbled on Wednesday as a renewed selloff in AI-linked stocks spread from Wall Street to Asia, driving a wave of risk aversion across assets. Nikkei and Kospi each fell nearly 3%, echoing the overnight decline in NASDAQ, which lost more than 2% as investors unwound positions in high-flying technology names. The correction comes amid growing fears that the AI trade, which has fueled much of this year’s rally, may be reaching unsustainable levels.

The pace and scale of gains in AI-related equities have prompted comparisons to past tech bubbles. Any meaningful correction in the sector could drag broader indexes lower given the heavy market weighting of mega-cap names. Goldman Sachs and Morgan Stanley added to the cautious tone this week, advising clients to brace for potential drawdowns over the next two years as valuations stretch beyond fundamentals.

The risk-off mood rippled into the crypto market, where Bitcoin briefly broke below the key 100,000 psychological level before recovering. Broader equity futures in both Europe and the U.S. also pointed lower, suggesting that the risk reset has yet to run its course.

In the currency market, Yen outperformed as investors flocked to safety, aided by continued verbal intervention from Japanese officials. Dollar also remained firm amid reduced odds of a December Fed cut, while Euro stayed resilient. On the weaker side, Kiwi and Aussie underperformed amid fading risk appetite, while Sterling also softened. Swiss Franc and Canadian Dollar traded in mid-range.

Attention now turns to U.S. ADP employment and ISM Services PMI today, which will serve as key policy signals during the ongoing government data blackout. With official statistics unavailable due to the shutdown, these private-sector indicators will heavily influence expectations for the Fed’s December meeting. However, the interpretations of the data could be nuanced: weaker readings could support hopes for Fed easing, but overly soft data might spark concern that the US economy is faltering faster than expected.

On the trade front, China’s State Council tariff commission announced the suspension of its 24% additional levy on U.S. goods for one year, while keeping a 10% baseline duty. Beijing also said it would lift tariffs of up to 15% on select U.S. agricultural goods from November 10. While the gesture offers a modest boost to sentiment, it was not enough to offset the day’s risk-off tone. With AI-driven volatility dominating markets. The prevailing theme remains caution, with risk assets struggling to find footing amid fears of a broader correction.

In Asia, at the time of writing, Nikkei is down -2.60%. Hong Kong HSI is down -0.29%. China Shanghai SSE is up 0.18%. Singapore Strait Times is down -0.39%. Japan 10-yer JGB yield is down -0.007 at 1.670. Overnight, DOW fell -0.53%. S&P 500 fell -1.17%. NASDAQ fell -2.04%. 10-year yield fell -0.017 to 4.089.

BoJ minutes: Hawks urge gradual tightening, others prefer to wait

Minutes from the BoJ’s September policy meeting revealed a deeply divided board, with members debating the pace and timing of future rate hikes. The nine-member board voted to keep the policy rate steady at 0.5%, rejecting calls by two hawkish members who wanted to raise borrowing costs to 0.75%. The discussion centered on balancing the downside risks to growth against persistent inflationary pressures, particularly from elevated food prices.

Some members argued for moving sooner rather than later. One hawkish participant called for raising rates at “somewhat regular intervals”, citing an improving flow of data, including corporate earnings and the Tankan business survey, as valuable indicators to guide normalization. Another member warned that the cost of waiting too long to tighten policy was “gradually increasing,” even if it would allow the BoJ to gain more clarity on the global outlook, especially from the U.S.

However, the majority on agreed it was better to wait for “a little more hard data” before considering another move. They noted that while conditions for tightening were gradually being met, acting now could “surprise the market” and risk destabilizing financial conditions. Some emphasized that as long as inflation expectations remain insufficiently anchored, maintaining accommodative conditions was appropriate to support Japan’s recovery.

Another member highlighted uncertainty surrounding the U.S. slowdown as a key reason to stay cautious, but conceded that, based purely on domestic fundamentals, Japan might soon meet the conditions for another hike.

New Zealand labor market stagnates, unemployment rate rises to 5.3%

New Zealand’s labor market showed further signs of softening in the Q3, with total employment flat at 0.0% qoq, missing expectations for a small 0.1% qoq rise. On an annual basis, employment fell -0.6% yoy.

Unemployment rate ticked up from 5.2% to 5.3%, in line with forecasts, extending a full year of readings above 5%. The last time joblessness reached this level was in late 2016. Labor-force participation rate slipped 0.2 ppt to 70.3%, suggesting some workers are leaving the active job market.

Wage growth also cooled, with all-sector earnings up 0.4% qoq and 2.1% yoy, indicating reduced pressure on labor costs.

China RatingDog PMI Services falls to 52.6, export orders contract

China’s service sector expansion eased slightly in October, with the RatingDog PMI Services slipping from 52.9 to 52.6, in line with expectations. Composite PMI also moderated to 51.8 from 52.5. While domestic demand improved, weakness in overseas orders capped momentum, reflecting the impact of renewed global trade instability on China’s external-facing industries.

RatingDog founder Yao Yu said new export business “fell noticeably into contractionary territory” amid “increased instability in the global trade environment”. However, total new orders still expanded as domestic demand strengthened. Business expectations remained high even though confidence edged slightly lower. Employment stayed in contraction, but the pace of job losses eased.

Price pressures were uneven. Input costs rose for an eighth consecutive month, reaching their highest level since October 2024. On the other hand, output prices slipped back into contraction, implying margin compression for service providers.

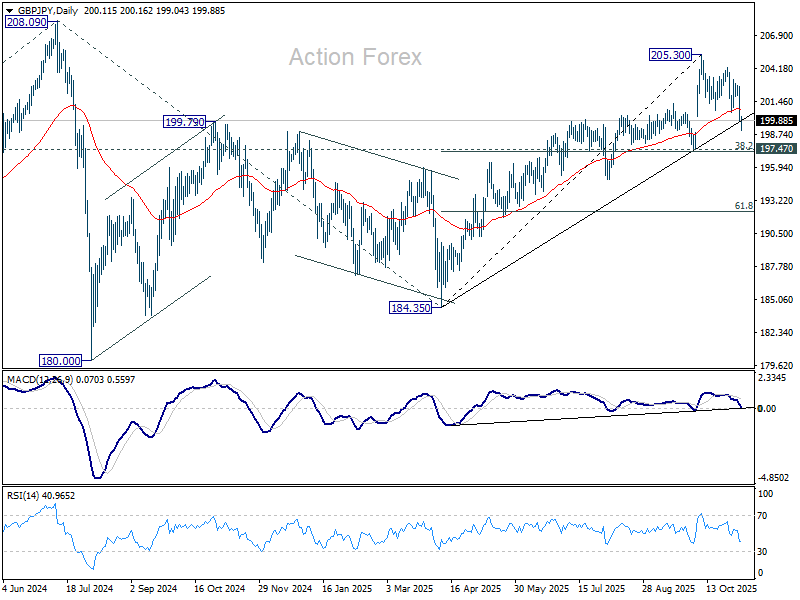

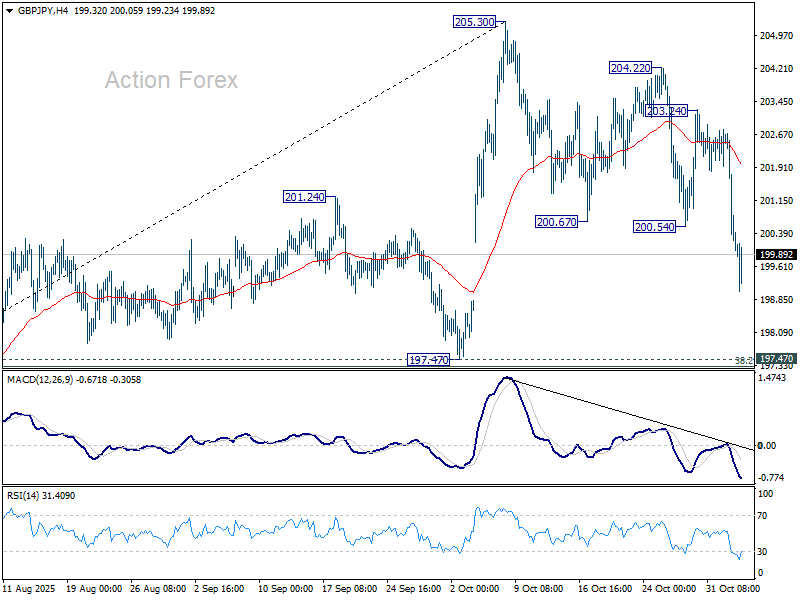

GBP/JPY Daily Outlook

Daily Pivots: (S1) 199.08; (P) 200.90; (R1) 201.91; More…

Intraday bias in GBP/JPY is back on the downside as fall from 205.30 resumed. Deeper decline should be seen to 194.47 cluster (38.2% retracement of 184.35 to 205.30 at 197.29). Strong support could be seen there to contain downside and bring rebound. above 300.54 minor resistance will turn bias neutral first. However, sustained break of 197.39/47 should confirm near term reversal, and target 61.8% retracement 192.35 next.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a corrective pattern which might have completed at 184.35. Firm break of 208.09 high will resume the up trend from 123.94 (2020 low). Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. However, decisive break of 197.47 support will dampen this view and extend the corrective pattern with another fall.