Risk-Off Strikes Again, Yen Awaits Signals from Takaichi–Ueda Meeting – Action Forex

Swiss Franc and Yen led the forex board in Asian session today, buoyed by a fresh wave of risk aversion. U.S. equities closed notably lower overnight, with pressure concentrated once again in AI-linked megacaps. The weakness spilled quickly into Asia, lifting traditional safe havens and putting renewed strain on high-beta currencies.

Nvidia fell around 2% ahead of Wednesday’s third-quarter earnings report, a release that traders are treating as a barometer of whether the AI-driven equity rally still has structural momentum. The company sits at the center of the debate over whether this year’s surge in AI valuations is still fundamentally sound or dangerously dependent on narrow market leadership. With concerns growing about weak breadth and stretched pricing, traders reduced risk heading into a heavy U.S. data week, including September NFP.

Yen also drew some support from Tokyo’s stepped-up verbal intervention efforts. Japan’s Finance Minister Satsuki Katayama intensified her warnings as USD/JPY crossed 155, describing the latest moves as “extremely one-sided and rapid,” and expressing “deep concern.” The comments helped stabilize the currency intraday, though traders remain skeptical about how far verbal guidance alone can go without policy action.

Indeed, expectations surrounding BoJ policy tightening—not ad hoc remarks—remain the primary driver of Yen’s underlying direction. And on that front, markets are looking to a key meeting today: the first direct discussion between Prime Minister Sanae Takaichi and BoJ Governor Kazuo Ueda. Reports suggest Takaichi is preparing a larger-than-expected economic stimulus package and is unlikely to welcome early or aggressive rate hikes.

The messaging after the meeting could meaningfully shape expectations for whether the next BoJ move comes in December, January, or even later. Any signal that the government prefers policy patience could blunt the impact of today’s intervention rhetoric and leave Yen vulnerable unless risk-off sentiment intensifies.

Risk appetite itself is the Yen’s other major swing factor, and today it is clearly leaning toward caution. Asian equities are deep in the red at the time of writing, with Nikkei down -2.90%, HSI down -1.62%, Shanghai SSE down -0.71%, and STI down -0.45%. Overnight U.S. Indexes also closed lower, with DOW -1.18%, S&P 500 -0.92%, NASDAQ -0.84%, and U.S. 10-year yield slipping -0.015 to 4.133.

Across FX markets, Swiss Franc remains the strongest by a wide margin, followed by Yen and then Euro. At the bottom sits Aussie, despite a relatively hawkish set of RBA minutes. Kiwi is the next weakest, followed by Dollar, while Loonie and Sterling sit squarely in the middle of the pack.

RBA minutes show no clear bias toward next move

RBA minutes from the November 3–4 meeting underscored a Board that sees the economy as “broadly in balance” and saw no justification to adjust the cash rate at this stage. While the central projection remains aligned with the RBA’s employment and inflation objectives, policymakers stressed that the next move in rates is not predetermined. Members agreed it was “not yet possible to be confident” about whether holding steady or easing further would become the more likely scenario.

The minutes outlined several conditions that could support keeping policy unchanged. One is a stronger-than-expected recovery in “demand” that lifts employment. Another is if incoming data suggest the economy’s “supply capacity” is weaker than previously assessed — potentially due to persistently high inflation or softer-than-expected productivity growth. A third is a reassessment of whether monetary policy is still “slightly restrictive”. Any of these outcomes, the RBA said, would “limit the scope for further easing”.

But the Board also detailed circumstances that could justify another rate cut. A material weakening in the labor market remains the clearest trigger. A second downside risk is if GDP growth disappoints — for example, if households turn “more cautious about spending” than currently assumed. In these cases, excess capacity would likely reappear, cooling inflation and warranting additional support.

Overall, the minutes confirm a central bank in wait-and-see mode. The RBA is not ruling out further easing, but neither is it leaning strongly toward it. The next several months of data — particularly on productivity, inflation persistence, and household spending — will be crucial in determining whether the Board holds steady or reopens the easing path in 2026.

Fed’s Waller backs December cut, Jefferson urges slow approach

Fed Governor Christopher Waller struck a notably dovish tone in a speech overnight, arguing that inflation risks have diminished and that weakening labor conditions now deserve greater attention.

Waller said he is “not worried about inflation accelerating”, adding that after months of cooling job data, it is unlikely that this week’s September employment report—or any incoming releases—would alter his view that “another cut is in order.” He warned that restrictive monetary policy is weighing disproportionately on lower- and middle-income consumers, reinforcing the case for easing.

Waller said a December cut would offer “additional insurance” against further deterioration in the labor market and help move policy closer to a neutral setting.

Separately, Vice Chair Philip Jefferson offered a more balanced perspective in his speech, acknowledging that policy has already been guided closer to neutral rate. He added, “The evolving balance of risks underscores the need to proceed slowly as we approach the neutral rate.”

Bitcoin eyes temporary support at 92k; broader downside risks stretch to 84k or even 70k

Bitcoin’s downturn has accelerated last week, dragging the cryptocurrency back toward levels last seen at the end of 2024. The retreat is striking: despite surging to a fresh record above 126k earlier this year, the entire advance has now been unwound.

For now, the pace of selloff has slowed, and some signs of stabilization are emerging. Bitcoin is approaching potential technical support near 92k, a level that aligns with measured projection of the current decline. Still, the broader technical picture suggests that this latest leg lower may be part of a correction within a much larger, multi-year uptrend rather than a simple dip to be bought.

History also matters, and a deeper drop could change behavior quickly. Bitcoin has repeatedly seen corrections of more than 50% during major down cycles, and any renewed acceleration lower may reawaken those memories among investors. Panic selling is an unmistakable risk if the decline extends sharply from here, especially given how quickly sentiment has turned since the October peak.

This downturn is not happening in isolation. The slide from the record high has been driven by a confluence of factors: widespread profit-taking by long-term holders, steady institutional outflows, and the forced liquidation of leveraged longs. Adding to the pressure, broader market sentiment has softened as uncertainty over a December Fed rate cut lingers. That policy hesitation has weighed on risk assets broadly, cryptocurrencies included.

Technically, short-term indicators reflect loss of downside momentum. 4H MACD is showing early signs of stabilization, and Bitcoin may find a floor near 100% projection of 126,289 to 101,896 from 116,405 at 92,012. Break of 97,351 minor resistance would signal near-term bottoming and allow for consolidation. However, any rebound is likely to be capped below 10,7493 resistance, keeping the bias tilted toward another decline.

The longer-term chart carries deeper implications. The entire uptrend from 15,452 (2022 low) may have completed as a five-wave rise to 126,289. Bearish divergence in W MACD supports this interpretation, and last week’s break below 55 W EMA (now at 98,483) reinforces the prospect of a broader correction.

From a structural perspective, 38.2% retracement of 15,452 to 126,289 at 83,949 is the minimum medium term downside target for the correction. However, given the combination of momentum loss and macro headwinds, a deeper decline toward 50% level at 70,870 — where a notable support cluster sits — cannot be ruled out.

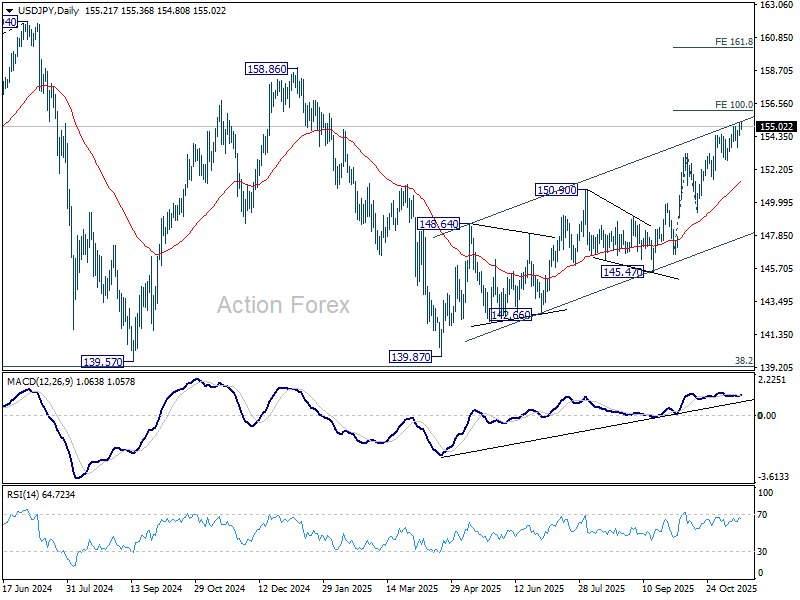

USD/JPY Daily Outlook

Daily Pivots: (S1) 154.43; (P) 154.86; (R1) 155.70; More…

USD/JPY’s rise resumed by breaking through 155.03 temporary top and intraday bias is back on the upside. Current rally from 139.87 should now target 100% projection of 146.58 to 153.26 from 149.37 at 156.05. Break there will pave the way to 158.85 key structural resistance. However, considering bearish divergence condition in 4H MACD, firm break of 153.60 support will indicate short term topping, and bring deeper pullback to 55 D EMA (now at 151.45).

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 149.37 support will dampen this bullish view and extend the corrective pattern with another falling leg.