Tech Slide Continues, Yen Still Lacks BoJ Signal – Action Forex

Global markets remain under pressure today as risk sentiment deteriorates further across regions. Europe opened firmly lower, tracking the broad declines seen earlier in Asia, while U.S. futures point to another weak session. Today’s tone is one of cautious de-risking, with markets showing little appetite to buy dips ahead of several major event risks.

Technology stocks continue to drive the weakness. Selling pressure on Nvidia stayed intense ahead of the company’s third-quarter results due after Wednesday’s close. Nvidia has been the symbolic leader of the AI-driven market rally, and the reaction to its earnings could determine whether sentiment stabilizes or slips into a deeper correction. With concerns over market breadth, excessive valuations, and shaky AI fundamentals resurfacing, traders are positioning defensively.

Attention is on Thursday’s U.S. non-farm payrolls release — the first since the government reopened. Today’s initial jobless claims, at 232k, and continuing claims, at 1.957m, produced almost no market reaction. That muted response raises doubts about how strongly markets will react to the delayed NFP, though the potential for a volatility shock should not be dismissed.

In Japan, the highly anticipated meeting between Prime Minister Sanae Takaichi and BoJ Governor Kazuo Ueda offered far less clarity than markets had hoped. Traders were looking for sharper messaging on policy direction given rising political pressure on the central bank. Instead, the meeting produced broad, non-committal remarks that did little to shift expectations.

Ueda reiterated that Japan’s wage-price dynamics are improving thanks to both government policy and the BoJ’s supportive stance. He described the central bank as “gradually adjusting” monetary support to ensure a stable path toward the 2% inflation goal. Takaichi, he said, appeared to accept his assessments. Yet nothing in his comments hinted at a change in stance or timeline.

Asked about the timing of the next rate hike, Ueda repeated that decisions will be made “appropriately” based on incoming data — a stance that leaves the market no clearer about whether a December move is even on the table. Given the political backdrop, traders remain convinced that January or later is more likely.

In FX, Dollar holds the top spot for the week so far, followed by Loonie and Sterling. At the other end of the spectrum, Aussie is the weakest performer, with Yen and Swiss Franc next in line. Kiwi and Euro sit squarely in the middle.

In Europe, at the time of writing, FTSE is down -1.39%. DAX is down -1.42%. CAC is down -1.40%. UK 10-year yield is up 0.006 at 4.543. Germany 10-year yield is down -0.015 at 2.701. Earlier in Asia, Nikkei fell -3.22%. Hong Kong HSI fell -1.72%. China Shanghai SSE fell -0.81%. Singapore Strait Times fell -0.86%. Japan 10-year JGB yield rose 0.015 to 1.749.

RBA minutes show no clear bias toward next move

RBA minutes from the November 3–4 meeting underscored a Board that sees the economy as “broadly in balance” and saw no justification to adjust the cash rate at this stage. While the central projection remains aligned with the RBA’s employment and inflation objectives, policymakers stressed that the next move in rates is not predetermined. Members agreed it was “not yet possible to be confident” about whether holding steady or easing further would become the more likely scenario.

The minutes outlined several conditions that could support keeping policy unchanged. One is a stronger-than-expected recovery in “demand” that lifts employment. Another is if incoming data suggest the economy’s “supply capacity” is weaker than previously assessed — potentially due to persistently high inflation or softer-than-expected productivity growth. A third is a reassessment of whether monetary policy is still “slightly restrictive”. Any of these outcomes, the RBA said, would “limit the scope for further easing”.

But the Board also detailed circumstances that could justify another rate cut. A material weakening in the labor market remains the clearest trigger. A second downside risk is if GDP growth disappoints — for example, if households turn “more cautious about spending” than currently assumed. In these cases, excess capacity would likely reappear, cooling inflation and warranting additional support.

Overall, the minutes confirm a central bank in wait-and-see mode. The RBA is not ruling out further easing, but neither is it leaning strongly toward it. The next several months of data — particularly on productivity, inflation persistence, and household spending — will be crucial in determining whether the Board holds steady or reopens the easing path in 2026.

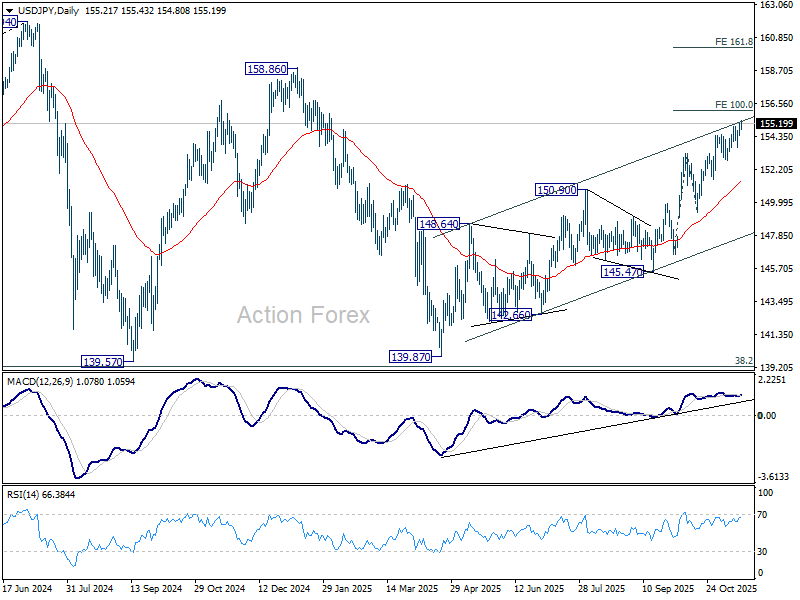

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 154.43; (P) 154.86; (R1) 155.70; More…

Intraday bias in USD/JPY remains on the upside for the moment. Current rise is part of the rally from 139.87. Next target is 100% projection of 146.58 to 153.26 from 149.37 at 156.05. Break there will pave the way to 158.85 key structural resistance. However, considering bearish divergence condition in 4H MACD, firm break of 153.60 support will indicate short term topping, and bring deeper pullback to 55 D EMA (now at 151.45).

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 149.37 support will dampen this bullish view and extend the corrective pattern with another falling leg.