Yen Extends Losses as Japan Floats Tweak to 2013 BoJ Framework – Action Forex

Yen’s selloff accelerated again today despite repeated warnings from top Japanese officials that they are monitoring FX markets with a “strong sense of urgency.” The latest remarks came after Finance Minister Satsuki Katayama met BoJ Governor Kazuo Ueda and Economic Revitalisation Minister Minoru Kiuchi, where all sides reaffirmed their commitment to the 2013 joint agreement to achieve 2% inflation.

Yet markets latched on to Katayama’s admission that she has proposed a technical tweak to the joint agreement while keeping substantial elements intact. Any hint of modification is noteworthy. The original 2013 statement—signed under intense pressure from then-Prime Minister Shinzo Abe—called on the BoJ to achieve its 2% inflation target “at the earliest date possible” and committed both sides to defeating deflation. That language remained unchanged even after inflation has exceeded 2% for more than three years.

What the tweak entails is still unclear, but investors see it through the lens of Prime Minister Sanae Takaichi’s clear pro-growth agenda and her administration’s resistance to any rapid tightening. A revised framework that places greater emphasis on supporting the economy—or softens the urgency around 2%—could effectively tie the BoJ’s hands and delay the next rate hike.

Yen bears also remain emboldened by expectations that Takaichi will deliver a massive fiscal package underpinned by ultra-low borrowing costs. Kyodo reported this week that the stimulus could exceed JPY 20 trillion, funded largely through an extra budget of around JPY 17 trillion. While Katayama said no final decision on size has been made, the political direction is clear: Tokyo wants growth first, tightening later.

Sterling, meanwhile, is holding steady after slightly stronger-than-expected headline UK inflation. But the details still show price pressures peaked in September at levels below the BoE’s own projections. That keeps a December rate cut firmly on the table, with swaps pricing around an 80% probability. Friday’s October retail sales and November PMIs are expected to reinforce the slowdown narrative.

The Autumn Budget next week remains the final catalyst. Markets will watch closely for clarity on whether tax measures will be deployed to plug the fiscal gap—an outcome that could shape the BoE’s path beyond December.

In the broader currency space so far today, Euro is the strongest performer, followed by Dollar and Loonie. Kiwi sits at the bottom, followed by Yen and Aussie, while Sterling and Swiss Franc are trading mid-pack.

In Europe, at the time of writing, FTSE is down -0.06%. DAX is up 0.22%. CAC is flat. UK 10-year yield is up 0.003 at 4.560. Germany 10-year yield is down -0.018 at 2.689. Earlier in Asia, Nikkei fell -0.34%. Hong Kong HSI fell -0.38%. China Shanghai SSE rose 0.18%. Singapore Strait Times rose 0.01%. Japan 10-year JGB yield rose 0.023 to 1.772.

Eurozone CPI finalized at 2.1%, services lead price pressure

Eurozone CPI was finalized at 2.1% yoy in October, edging down from September’s 2.2% and keeping headline inflation close to the ECB’s target. Core CPI held steady at 2.4% yoy, unchanged from the previous month.

Services remained the dominant driver of inflation in Eurozone, contributing +1.54 percentage points, followed by food, alcohol and tobacco at +0.48 pp, while energy once again exerted a mild drag by -0.08pp.

Across the EU, inflation softened slightly to 2.5% yoy from September’s 2.6%. Price dynamics continued to diverge sharply across member states: Cyprus recorded the lowest annual rate at 0.2%, followed by France (0.8%) and Italy (1.3%). At the other end of the spectrum, Romania remained an outlier at 8.4%, with Estonia (4.5%) and Latvia (4.3%) also posting elevated readings. Compared with the previous month, inflation eased in fifteen member states, held steady in three, and increased in nine.

UK CPI slows to 3.6%, keeping BoE on track for December cut

UK inflation eased in October, with headline CPI slowing from 3.8% yoy to 3.6%, just above the market’s 3.5% forecast. Core inflation (excluding energy, food, alcohol and tobacco) matched expectations at 3.4% yoy, down from 3.5% previously.

Goods inflation cooled, slipping from 2.9% yoy to 2.6%, while services inflation—still the stickiest component—eased from 4.7% to 4.5%.

On a monthly basis, headline CPI rose 0.4% mom.

The figures point to steady, gradual deceleration rather than sharp disinflation, leaving the BoE’s December cut narrative largely intact. Markets are unlikely to adjust pricing meaningfully until the Autumn Budget clarifies the fiscal stance. For now, the data reinforces a picture of easing, but not yet subdued, domestic price pressures.

Australia wage price index rises 0.8% qoq in Q3, private sector underperforms

Australia’s wage price index rose 0.8% qoq in Q3, matching expectations and holding the same pace as Q2. The headline stability masks a mild divergence across sectors: private-sector wages increased 0.7% qoq while public-sector wages climbed 0.9% qoq, continuing their recent outperformance.

On an annual basis, wage growth came in at 3.4% yoy, unchanged from Q2. Public-sector pay rose 3.8% yoy, edging up from last year’s 3.7%. Private-sector wage growth slowed to 3.2% yoy from 3.5% in September 2024. This marks the third consecutive quarter in which public wages have grown faster than their private counterparts.

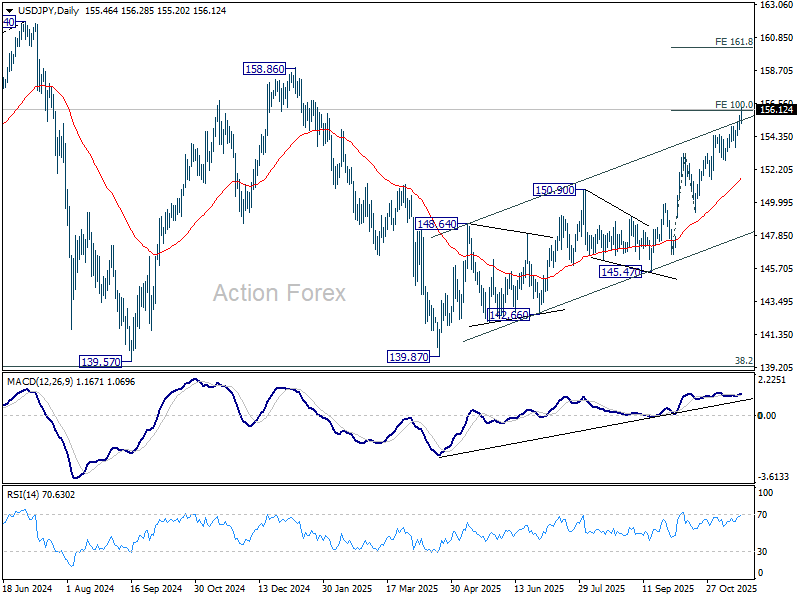

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 154.98; (P) 155.36; (R1) 155.89; More…

USD/JPY’s rally continues today and breaks above 100% projection of 146.58 to 153.26 from 149.37 at 156.05. There is no sign of topping yet and the break of medium term rising channel indicates upside acceleration. Intraday bias stays on the upside. Next target is 158.85 key structural resistance, and then 161.8% projection at 160.17. On the downside, below 155.20 minor support will turn intraday bias neutral and bring consolidations, before staging another rise.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 150.90 restiveness turned support will dampen this bullish view and extend the corrective pattern with another falling leg.