Dollar Holds Firm, Risk Appetite Crumbles as Nvidia Euphoria Fades – Action Forex

Commodity currencies came back under pressure today as the burst of Nvidia-driven optimism evaporated almost as quickly as it arrived. After a strong start, major U.S. indexes staged a staggering reversal and closed sharply lower — marking the biggest midday turn since April. What triggered the shift remains unclear, but the message from markets was unmistakable: investors abruptly backed away from risk and rotated back into bonds.

The reversal spilled into Asian trading as well. Equity indexes in Japan and South Korea saw heavy selling, with risk sentiment deteriorating across the region. The speed of the shift suggests that investors remain highly sensitive to valuation concerns and macro uncertainty, even in the face of upbeat earnings from one of the AI sector’s bellwethers.

The deterioration in sentiment helped solidify the Dollar’s position as the strongest performer for the week so far. Despite Thursday’s stronger-than-expected NFP report, market expectations for a December Fed cut remained largely unchanged, holding around a 35% probability. Traders appear comfortable with the view that the Fed will likely stay on hold in December unless economic data deteriorates materially.

Comments from Fed officials reinforced the tone set by the October FOMC minutes. Many policymakers continued to emphasize caution, signaling reluctance to ease too quickly after delivering two consecutive rate cuts in the last two meetings. That steady drumbeat of hawkish restraint has further dampened expectations for a pre-year-end cut.

In Japan, policymakers were busy on the fiscal side. The cabinet approved a new stimulus package totaling JPY 21.3 trillion, framed around three pillars: addressing rising prices, supporting economic strength, and enhancing defense and diplomatic capabilities. Prime Minister Sanae Takaichi is pushing hard to bolster the slowing economy and cushion households from persistent inflation.

In the currency markets, Dollar leads the weekly performance ladder comfortably, followed by Loonie and Sterling. At the bottom are Yen, followed by Kiwi and then Aussie. Euro and Swiss Franc are sitting squarely in the middle of the pack.

In Asia, Nikkei fell -2.23%. Hong Kong HSI is down -1.61%. China Shanghai SSE is down -1.96%. Singapore Strait Times is down -0.93%. Japan 10-year JGB yield fell -0.029 to 1.791. Overnight, DOW fell -0.84%. S&P 500 fell -1.56%. NASDAQ fell -2.15%. 10-year yield fell -0.027 to 4.106.

BoJ’s Ueda flags bigger FX pass-through to underlying inflation

BoJ Governor Kazuo Ueda told parliament today that Yen weakness is increasingly feeding into domestic inflation. He noted that as companies have become “more active in raising prices and wages,” the pass-through from higher import costs to consumer inflation has intensified. That dynamic raises the risk that currency-driven price gains could influence inflation expectations and “underlying inflation,” he warned.

Ueda added that the central bank will assess a rate hike at upcoming meetings, with the focus firmly on data that sheds light on next year’s wage momentum. He emphasized said policymakers want to “spend a bit more time to confirm whether firms’ active wage-setting behavior won’t be disrupted,”

He added that the Bank is still gathering information from its nationwide branches and intends to incorporate both official data and its own surveys into the next policy discussions.

Japan CPI core accelerates again to 3% in October

Japan’s October CPI data showed inflation firming again, with core CPI (ex-fresh food) rising to 3.0% yoy from 2.9%, matching expectations and marking the second month of renewed acceleration. The measure has now stayed above the BoJ’s 2% target for more than three and a half years, highlighting how persistent the price backdrop has become.

Core-core CPI, which excludes both fresh food and energy, edged up from 3.0% to 3.1% yoy, while headline CPI rose from 2.9% to 3.0%.

Food excluding fresh items surged 7.2%, and utilities rose 2.2%, confirming that household-facing inflation pressures remain elevated. Rice inflation, however, continues to ease sharply, slipping to 40.2% from September’s 49.2% and offering slight relief after months of extreme gains.

Japan PMI composite rises to 52.0 as services lead and manufacturing stabilizes

Japan’s November flash PMIs offered a cautiously constructive signal for the economy, with the Composite Index rising from 51.5 to 52.0 — the best reading in three months and joint-highest since August 2024. Manufacturing activity remained in contraction but improved to 48.8 from 48.2. Services held steady at a solid 53.1.

S&P Global’s Annabel Fiddes noted that the decline in manufacturing output eased to its slowest pace since August, hinting at a gradual move toward stabilization. Business confidence also strengthened, reaching its highest level since January. That pickup in sentiment helped drive the strongest rise in employment since June, as firms look to expand capacity in anticipation of firmer activity ahead.

Inflation pressures remain a lingering concern. Input costs rose at the fastest rate in six months amid higher labor expenses and supplier price increases. In response, firms lifted selling prices at a solid pace to protect margins.

Australia’s PMI composite rises to 52.6, firmer growth with manufacturing rebounds

Australia’s November flash PMIs delivered a surprisingly upbeat signal, with manufacturing jumping back into expansion at 51.6 after October’s soft 49.7. Services PMI also nudged higher from 52.5 to 52.7, lifting Composite Index from 52.1 to 52.6. The rebound in manufacturing is particularly encouraging given the sector’s recent weakness.

S&P Global’s Jingyi Pan noted that new orders in goods returned to expansion for the first time since August, helping lift overall momentum. Rising business optimism—now at a five-month high—also points to firmer activity ahead.

Price pressures, while slightly firmer than at the start of the quarter, remain “broadly muted”. Employment growth slowed, but survey responses indicate this was driven partly by “hiring challenges” rather than a sharp loss in demand, particularly in the services sector.

NZ sees strong EU export growth, yet trade balance hit by China import surge

New Zealand’s October trade report showed exports and imports both rising solidly from a year earlier, yet leaving the country with a monthly deficit of NZD -1.5B. Goods exports climbed 16% yoy to NZD 6.5B, driven by broad-based strength across key markets. However, imports grew nearly as fast—up 11% to NZD 8.0B—as demand for overseas goods remained firm, particularly from China.

Export performance was strong across most major destinations. Shipments to China rose 18% yoy, while exports to Australia increased 14%. Notably, exports to the EU surged 40%—a standout gain that helped offset softer growth in other regions. The U.S. and Japan also saw moderate increases of 5.4% and 7.5% respectively.

On the import side, the story was more uneven. Imports from China surged 29% yoy and those from Australia rose 6.8%, pushing the total higher even as purchases from several other partners fell. The U.S. and South Korea both saw sizeable declines in imports, down -15% and -19% respectively, while the EU recorded a small drop of -2.6%.

Fed’s Goolsbee warns against front-loading cuts amid patchy inflation data

Chicago Fed President Austan Goolsbee struck a cautious tone overnight, warning that the central bank itself risks “front-loading too many rate cuts” before it has enough information to judge whether inflation is truly easing again. He stressed that his concern is not about the Fed’s destination — he still believes rates “are going to go down” over the medium term — but rather about the wisdom of easing too quickly in the short run given the recent inflation uptick.

Goolsbee said he remains uneasy about rising services inflation based on the data published before the government shutdown. He emphasized that the absence of fresh, reliable inflation readings has left policymakers with limited visibility, noting there are few credible private sources to bridge the gap created by missing official data.

Fed’s Paulson urges caution as every cut raises the bar for next

Philadelphia Fed President Anna Paulson said overnight that she is approaching the December FOMC “cautiously,” highlighting a delicate balance between a cooling but still-stable labor market and inflation that remains above target.

The delayed September jobs report was “encouraging,” she said, as it showed the rise in unemployment to 4.4% was largely consistent with softer labor supply, not a collapse in demand. That leaves the job market broadly in equilibrium.

Paulson stressed that the Fed must recognize how its easing cycle compounds over time. “Each rate cut raises the bar for the next cut,” she noted, because every move lowers policy closer to the point where it stops restraining the economy and begins actively stimulating it.

Regarding inflation, Paulson reiterated that tariffs are unlikely to generate sustained price pressures. The bigger driver remains moderating demand, which is helping contain inflation even as it remains above the 2% goal for what will likely be five consecutive years.

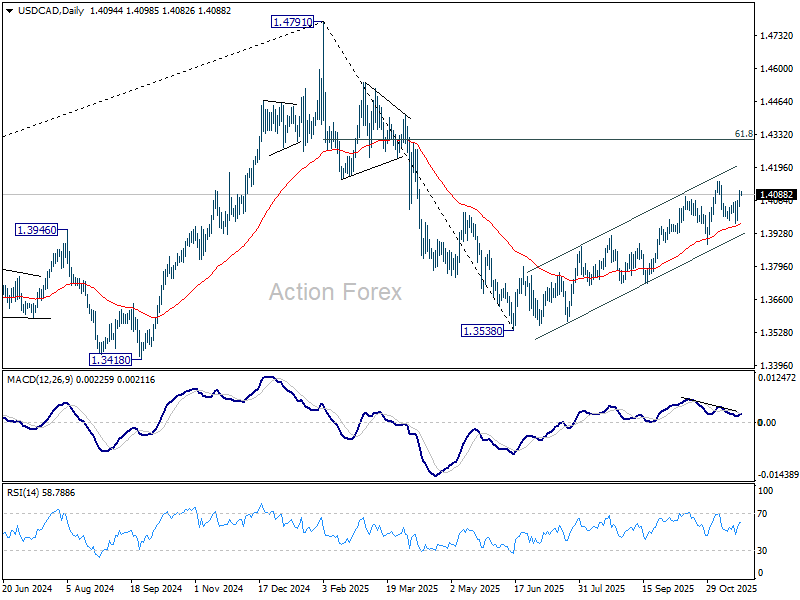

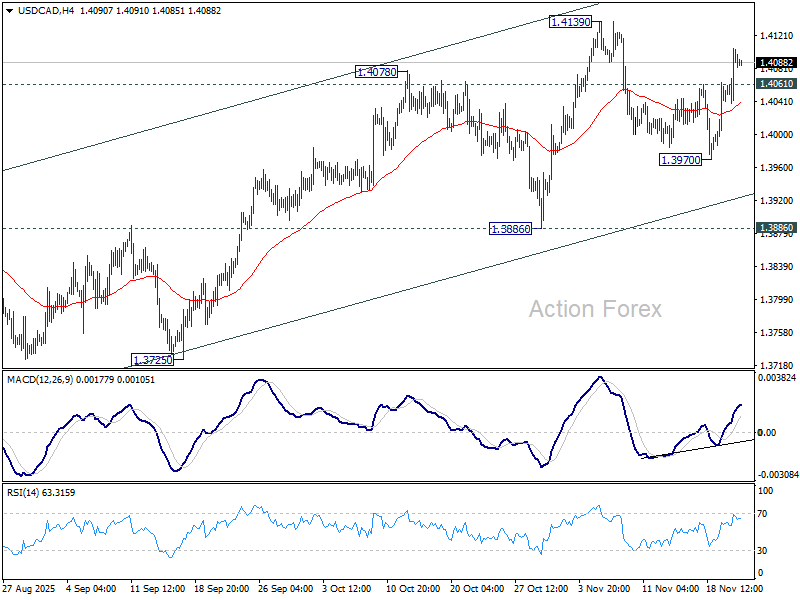

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4058; (P) 1.4082; (R1) 1.4125; More…

USD/CAD’s strong break of 1.4061 resistance should finally confirm that pullback from 1.4139 has completed at 1.3970. Intraday bias is back on the upside. Break of 1.4139 will resume larger rise from 1.3538 towards 61.8% retracement of 1.4791 to 1.3538 at 1.4312. For now, risk will stay on the upside as long as 1.3970 support holds, in case of retreat.

In the bigger picture, price actions from 1.4791 medium term top is likely just unfolding as a correction to up trend from 1.2005 (2021 low), with rise from 1.3538 as the second leg. A third leg should follow before up trend resumption. That is, range trading is set to extend for the medium term. For now, this will remain the favored case as long as 1.3886 support holds. However, firm break of 1.3886 will revive the case that fall from 1.4791 is indeed a larger scale correction.