Yen Falters After Friday Rebound; UK Budget, RBNZ Cut, U.S. Data Catch-Up – Action Forex

Asian trading has been subdued with Japan on holiday. Yen’s sharp rebound at the end of last week has failed to extend, with the currency losing energy amid a lack of fresh catalysts. The pause reflects an uneasy balance. While some investors expect further corrective strength, broader policy expectations continue to lean against the Yen. One of the major headwinds remains the view that BoJ could delay its next rate hike into early 2026, driven increasingly by political pressure rather than macro fundamentals.

Early signals from the next Shunto round show Rengo pushing again for 5%-plus pay hikes in 2026—mirroring the demand that produced the biggest wage increase in 34 years. While companies may not fully comply, manufacturers are already benefiting from the U.S. tariff deal and a competitive Yen. Tight labor conditions further raise the likelihood of continued wage strength.

Despite this structural wage pressure—one of BoJ’s key conditions for tightening—the government is uneasy about premature rate hikes that could undermine last week’s JPY 17.7T stimulus package. That political dimension has become increasingly influential in shaping expectations for the next move, particularly given Prime Minister Sanae Takaichi’s strong approval ratings.

Looking ahead, the UK’s Autumn Budget stands out as a major test for domestic assets. Gilt markets, equities and Sterling all depend on whether Finance Minister Rachel Reeves can deliver credible fiscal consolidation while still supporting growth. A misstep could expose UK bond markets to a confidence shock. Beyond the UK, the U.S. will release more delayed data following the government reopening, and RBNZ is expected to cut rates again.

In the currency markets, Euro is currently the strongest performer, followed by Aussie and Sterling, while Yen sits at the bottom alongside Kiwi and Dollar. Swiss Franc and Loonie sit in the middle of the pack. However, these rankings are almost certain to shift as the week unfolds.

In Asia, at the time of writing, Hong Kong HSI is up 1.80%. China Shanghai SSE is down -0.10%. Singapore Strait Times is up 0.46%. Japan is on holiday.

Fed’s Collins signals hesitation on December rate cut

Boston Fed President Susan Collins signaled a clear preference for caution ahead of the December 9–10 FOMC meeting, saying she sees “reasons to be hesitant” about lowering borrowing costs again. After the 50bps of easing delivered in September and October, Collins argued on Saturday that policy is now “mildly restrictive” and appropriately calibrated to current conditions.

Collins stressed that the Fed faces a difficult balance: inflation remains above target while the job market shows visible signs of softening. She said risks exist “on both sides of the mandate,” and emphasized that more persistent weakness in employment could change her stance. “If I saw more evidence of softening and weakness, I would take that seriously,” she noted.

She also highlighted the unusually wide set of views emerging inside the Committee. “We’re in a complex period” for setting policy, Collins said, adding that a range of perspectives is healthy at a time when the economic outlook is highly uncertain.

SNB’s Schlegel says negative rates possible but bar remains high

SNB Chairman Martin Schlegel signaled over the weekend that the central bank remains willing to reintroduce negative interest rates if mid-term price stability were threatened. However, he emphasized that “the bar is high”.

Schlegel also addressed the recent deal to cut U.S. tariffs on Swiss goods to 15% from 39%, describing it as helpful but far from being a “game changer”. The duties only affected roughly 4% of Swiss exports.

He said U.S. trade policy remains the biggest source of uncertainty for Swiss companies, noting that exporters will likely pause U.S.-bound shipments until the lower tariff rate is fully implemented.

RBNZ to cut 25bps, yet surprise can’t be dismissed; US data catch-up continues

RBNZ is widely expected to lower OCR by another 25bps to 2.25%, extending the easing cycle to cushion the deteriorating domestic economy. But the picture is more complicated than the market-implied consensus suggests, with policymakers confronting a deeper slowdown, a long gap until the next meeting, and a looming change in leadership.

The key question is whether taking OCR to 2.25% is sufficient to stabilize activity. Even if the Committee believes this level provides adequate support, it is highly unlikely for RBNZ to shut the door on further easing given how fragile the outlook remains.

A deeper challenge is whether the Board believes another forceful step is justified. The next policy meeting is not until February—nearly three months away. That creates an unusually long gap and raises the prospect that the Bank may consider front-loading, leaving open the possibility—however slim—of a larger 50bps cut to avoid being behind the curve.

Meanwhile, this will be the final meeting overseen by acting Governor Christian Hawkesby before Anna Breman formally takes the helm on December 1. Some argue Hawkesby may prefer to “finish the job” by delivering a decisive step, clearing the decks for Breman. Others see value in holding fire and leaving major decisions to the incoming Governor.

Even if the base case remains a 25bps cut for the RBNZ, markets should brace for surprise potential.

This week’s central-bank calendar is not limited to RBNZ. ECB meeting accounts should reaffirm officials’ repeated message that inflation and policy rates are essentially in the right place, with little urgency to adjust stance again soon. Fed’s Beige Book will be scrutinised for clues on how tariffs are feeding through to pricing behavior and regional labour markets—particularly important given data release delays during the government shutdown.

On the data front, the U.S. will release a heavy slate of catch-up indicators including retail sales, PCE inflation and durable goods orders. Globally, markets will sift through Germany’s Ifo business climate, Canada and Switzerland GDP, Japan Tokyo CPI, and Australia’s monthly CPI.

Here are some highlights for the week:

- Monday: Germany Ifo business climate.

- Tuesday: Germany GDP final; US retail sales, PPI, house price index, pending home sales, consumer confidence.

- Wednesday: Japan corporate service prices; Australia monthly CPI; RBNZ rate decision; US jobless claims, durable goods orders, Chicago PMI, personal income and spending, PCE inflation, Fed’s Beige Book.

- Thursday: New Zealand retail sales, ANZ business confidence; Germany Gfk consumer sentiment; Eurozone M3; ECB meeting accounts.

- Friday: Japan Tokyo CPI, industrial production, retail sales; Germany retail sales, CPI flash, unemployment; Swiss GDP, KOF economic barometer, Canada GDP.

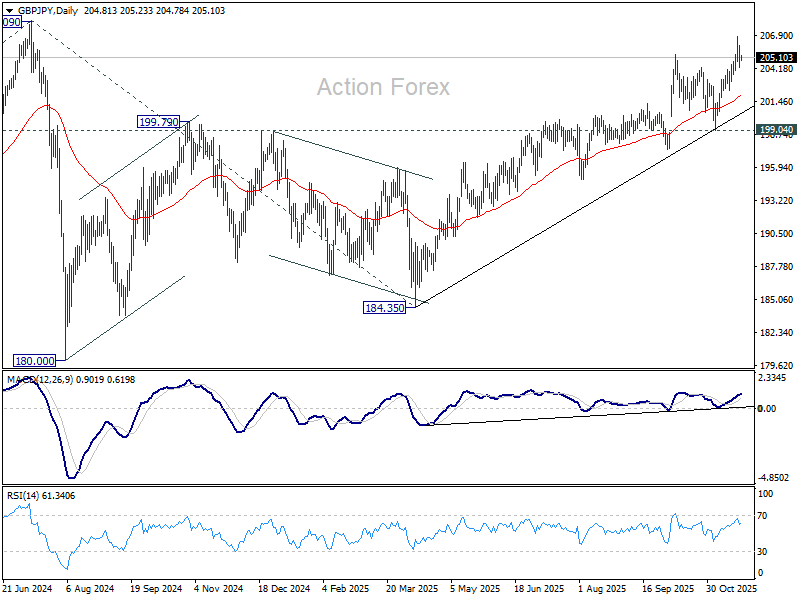

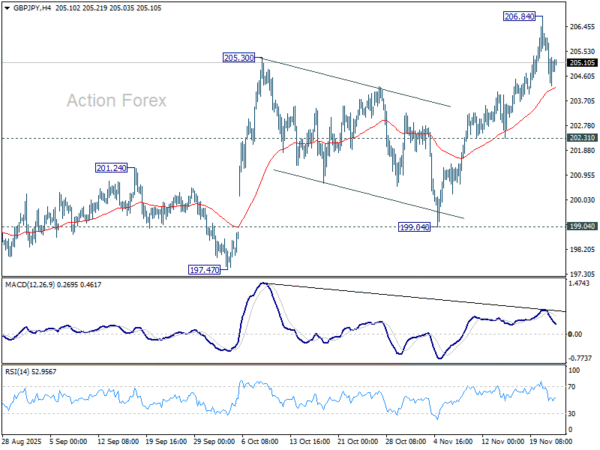

GBP/JPY Daily Outlook

Daily Pivots: (S1) 204.11; (P) 205.09; (R1) 205.88; More…

GBP/JPY recovered mildly ahead of 55 4H EMA and outlook is unchanged. Intraday bias remains neutral, and consolidations could continue below 206.84. Deeper retreat might be seen but downside be contained by 202.31 support to bring another rise. Break of 206..84 will target 208.09 high. Decisive break there will confirm long term up trend resumption.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a corrective pattern which might have completed at 184.35. Firm break of 208.09 high will resume the up trend from 123.94 (2020 low). Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. However, decisive break of 199.04 support will dampen this view and extend the corrective pattern with another fall.