Dollar Softens Further on Dovish Repricing; Bessent Signals Fed Chair Decision Near – Action Forex

Dollar weakened notably against Euro and Yen in early U.S. session, tracking another leg lower in Treasury yields as markets absorbed softer-than-expected September retail sales. While the report was backward-looking, it reinforced the direction of travel for consumption and added incremental weight to the view that demand is steadily cooling. PPI, meanwhile, was nor alarming.

The easing narrative continues to strengthen. Fed funds futures now imply nearly an 85% probability of a 25bps cut in December, with investors leaning heavily on the growing chorus of key Fed officials highlighting labor-market risks over inflation concerns. Dollar’s dip reflects that shift, though reactions across asset classes are uneven. Equity futures were broadly steady in pre-market trade.

Meanwhile, U.S. Treasury Secretary Scott Bessent told CNBC that President Donald Trump is likely to announce his choice for the next Fed Chair before Christmas. He emphasized that the timeline ultimately rests with the president but described the selection process as “moving along very well.”

The shortlist remains broad. Candidates believed to be under consideration include NEC Director Kevin Hassett, former Fed Governor Kevin Warsh, BlackRock’s Rick Rieder, and current Fed Governors Christopher Waller and Michelle Bowman. Bessent also hinted at a philosophical shift in how the administration views the Fed’s role. He suggested the central bank should “move back into the background” and play a less dominant role over the economy and markets than it has since the financial crisis.

In daily performance terms, Yen leads the majors, followed by Sterling and Euro. Kiwi is the weakest performer, trailed by Swiss Franc and Aussie, while Euro and Loonie sit in the middle of the pack.

In Europe, at the time of writing, FTSE is up 0.44%. DAX is up 0.71%. CAC is up 0.66%. UK 10-year yield is down -0.037 at 4.507. Germany 10-year yield is down -0.014 at 2.680. Earlier in Asia, Nikkei rose 0.07%. Hong Kong HSI rose 0.69%. China Shanghai SSE rose 0.87%. Singapore Strait Times fell -0.24%. Japan 10-year JGB yield rose 0.016 to 1.804.

US retail sales miss at 0.2% mom growth in September

US retail sales rose 0.2% mom to USD 733.3B in September, falling short of the 0.4% forecast. Ex-auto sales performed slightly better at 0.3% mom, in line with expectations. Ex-gasoline sales were flat.

On a longer view, sales for the July–September period were still up 4.5% yoy, indicating that overall demand remains broadly supported.

US PPI rises 0.3% mom in September, core pressure eases

US PPI rose 0.3% mom and 2.7% yoy in September, matching expectations. The entire monthly advance came from goods, where prices jumped 0.9%, while services were flat.

PPI final demand less food, energy, and trade—edged up just 0.1% mom after a firmer 0.3% mom reading in August. On a 12-month basis, core rose 2.9%.

UK retail sentiment hits 17-year low ahead of Autumn Budget

UK retail sentiment deteriorated sharply in November, with the CBI’s quarterly Distributive Trades Survey showing confidence plunging to its worst level in 17 years. Firms expect their business situation to worsen over the coming quarter, with the index sliding to -35% from -10% in August.

Sales volumes also contracted at a faster pace, with the year-to-November balance dropping to -32% from -27% in October. Retailers expect the decline to moderate slightly next month, but the outlook remains bleak, pointing to another weak patch heading into the key holiday period. Even modest stabilization would leave activity at depressed levels by historical standards.

CBI Deputy Chief Economist Alpesh Paleja said retailers are still grappling with “a long spell of weak demand”. He added that uncertainty surrounding the forthcoming Autumn Budget is causing businesses to delay investment and hiring decisions.

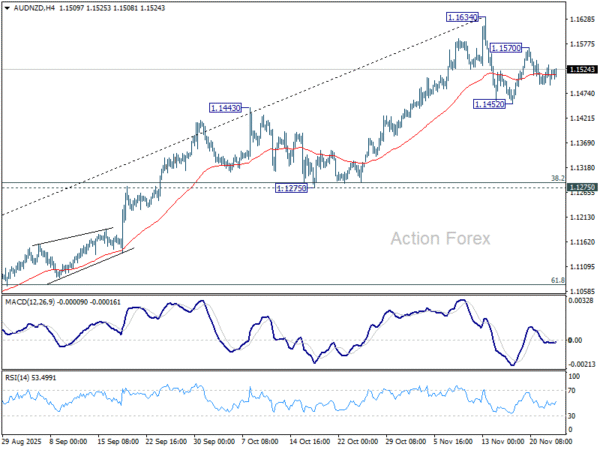

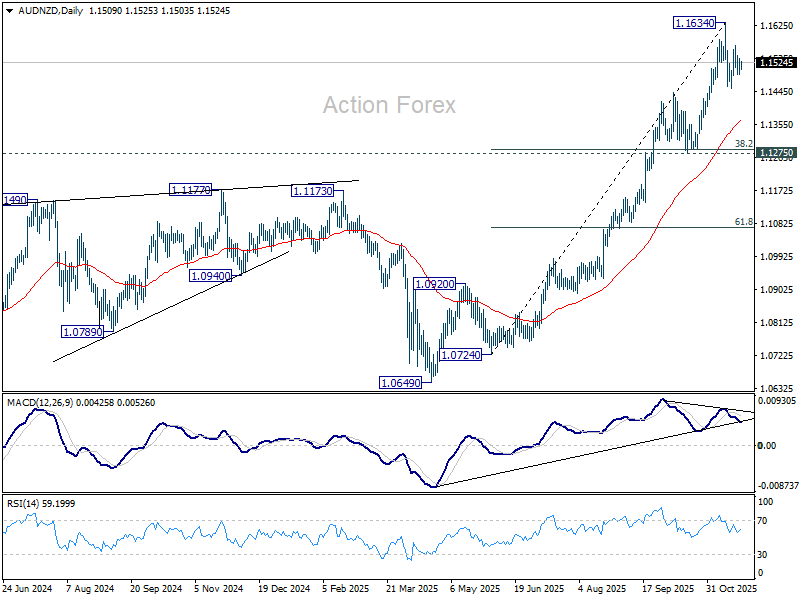

Two-way risks for AUD/NZD as RBNZ cut meets rising Australia CPI

AUD/NZD is shaping up for an active week, with two major catalysts—RBNZ’s rate announcement and Australia’s monthly CPI—set to hit on Wednesday.

RBNZ is widely expected to cut the OCR by 25bps to 2.25%. The NZIER Monetary Policy Shadow Board also endorsed a quarter-point reduction, arguing that although the economy is beginning to recover from a low base, excess capacity remains and a small additional cut is justified. Some members, however, warned against pushing stimulus too far, citing the risk of reigniting inflation—highlighting a cautious undercurrent within the broader policy debate.

On the medium-term path, the Shadow Board’s views clustered around an OCR of 2.25%–2.50% in a year, implying broad consensus that only limited easing will be required beyond November. While a minority still consider the risk of a larger, front-loaded cut—particularly given the long three-month gap until the next meeting—the Board’s recommendations may help stabilize expectations at a standard 25bps move.

In Australia, CPI is expected to rise again, from 3.5% to 3.6% for October, the fourth consecutive acceleration from June’s trough of 1.9%. A trend like this keeps the RBA firmly on hold for the remainder of the year, with any upside surprise diminishing the likelihood of a February rate cut. Sticky inflation would strengthen AUD by reinforcing Australia’s higher-for-longer stance relative to New Zealand’s easing cycle.

Technically, AUD/NZD carved out a short-term top at 1.1634 earlier this month and has since turned sideway. For now, it’s seen as in a brief near term correction. Break of 1.1570 minor resistance will solidify this case and bring retest of 11634 high.

However, on the downside, break of 1.1452 support will indicate that deeper decline is underway, as fall from 1.1634 could be correcting whole rise from 1.0724. But even so, downside should be contained by 1.1275 cluster support (38.2% retracement of 1.0724 to 1.1634 at 1.1286) or even higher at 55 D EMA (now at 1.1362).

There should be one more up leg through 1.1634 before the whole five-wave up trend from 1.0649 (April low) completes.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1499; (P) 1.1524; (R1) 1.1547; More…

EUR/USD recovers further today but stays well below 1.1655 resistance. Intraday bias remains neutral and further decline is still in favor. On the downside, below 1.1490 and 1.1467 will resume the whole decline from 1.1917 high. Next targets are 1.1390, and then 38.2% retracement of 1.0176 to 1.1917 at 1.1252.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1328) holds, the up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.