Quiet Markets, Technical Outage, and a Dollar Still Stuck at Weekly Lows – Action Forex

Markets were broadly quiet today as holiday conditions dominated trading, with liquidity thinning further after a major technical issue at the Chicago Mercantile Exchange brought several platforms to a halt. The CME said trading had come to a standstill due to a cooling problem at one of its data centers. The outage affected Globex futures and options, EBS foreign-exchange trading and BMD markets, with the exchange warning that price adjustments may take time to filter through once systems fully recover.

In currencies, the Dollar attempted another modest rebound but once again struggled to build momentum. With little fresh data and most investors already looking ahead to next week’s U.S. releases—including ISM manufacturing and services—there was no catalyst to drive a meaningful shift. Many traders may simply prefer to wait even longer for the December 10 FOMC decision before committing to larger directional positions.

As a result, the weekly performance picture remains unchanged. Dollar is still the weakest performer of the week, followed by Yen and Swiss Franc. At the top end, Kiwi continues to lead, supported by a hawkish RBNZ stance, while Aussie and Sterling follow. Euro and Loonie sit squarely in the middle.

In Europe, at the time of writing, FTSE is up 0.27%. DAX is up 0.18%. CAC is up 0.25%. UK 10-year yield is down -0.02 at 4.436. Germany 10-year yield is flat at 2.685. Earlier in Asia, Nikkei rose 0.17%. Hong Kong HSI fell -0.34%. China Shanghai SSE rose 0.34%. Singapore Strait Times rose 0.32%. Japan 10-year JGB yield rose 0.005 to 1.807.

ECB survey shows slight rise in 12-month inflation expectations to 2.8%

The ECB Consumer Expectations Survey for October showed a small uptick in near-term inflation expectations, with the median 12-month outlook rising to 2.8% from 2.7% in September.

Longer-term expectations remained stable, with the three-year horizon unchanged at 2.5% and the five-year measure anchored at 2.2%. Inflation uncertainty was likewise steady, indicating consumers do not see a significant shift in the underlying trend.

On the economic front, consumers grew slightly more optimistic about growth. Expectations for GDP over the next 12 months improved to -1.1%, up from -1.2% previously. However, labor-market expectations worsened. Consumers now expect the unemployment rate to reach 11.0% in 12 months, up from 10.7% in September.

Swiss KOF barometer edges up to 101.7 on stronger demand

Switzerland’s KOF Economic Barometer ticked higher in November, rising from 101.5 to 101.7 and signaling modest improvement in the near-term economic outlook.

KOF noted that the improvement is concentrated on the demand side. Indicator bundles tied to foreign demand and private consumption strengthened, suggesting both external orders and household activity are on firmer footing.

On the production side, however, parts of the economy remain under pressure. Indicators for financial and insurance services, as well as construction, deteriorated, revealing a mixed underlying picture.

Swiss GDP contracts -0.5% in Q3, pharma and chemicals lead decline

Swiss GDP fell -0.5% qoq in Q3, marking a sharp reversal driven almost entirely by the chemical and pharmaceutical sector. After strong momentum earlier in the year, the industry saw output plunge -7.9%, erasing prior gains and dragging the broader economy into contraction.

Authorities noted that the downturn reflects recent volatility in foreign trade. Earlier quarters saw a surge in pharma exports, partly driven by front-loading ahead of U.S. trade-policy changes. Those temporary boosts have now unwound, resulting in a “compensatory decline” that weighed heavily on Q3 activity.

Tokyo core CPI holds at 2.8% in November, inflation pressures still firm

In Japan, Tokyo’s inflation profile showed little moderation in November, with both core CPI and core-core CPI staying at 2.8% yoy. The readings came in slightly firmer than expected, while headline CPI eased just one-tenth to 2.7%. The stability of these measures indicates that underlying inflation momentum remains intact.

Much of the price momentum came from food, where sharp gains continued. The cost of rice surged 38.5% yoy, coffee beans rose 63.4%, and chocolate jumped 32.5%, reflecting broad price pressures across essential and discretionary categories.

Meanwhile, goods inflation climbed 4.0% yoy. Services inflation eased only marginally to 1.5% from 1.6%.

Japan industrial production surges 1.4% mom in October on auto rebound, but fluctuation to continue

Japan’s industrial production rose 1.4% mom in October, sharply beating expectations of a -0.6% decline. The rebound was driven primarily by a 6.6% jump in motor vehicle output, a sector benefiting from the U.S. tariff rate on Japanese cars being reduced to 15% from 27.5% in mid-September. The improvement highlights how quickly Japanese automakers responded once tariff uncertainty eased.

However, the forward outlook remains soft. Based on its manufacturer survey, METI expects output to fall -1.2% in November and contract a further -2.0% in December. Despite October’s upside surprise, the ministry kept its overall assessment unchanged, saying industrial production “fluctuates indecisively” amid continued uncertainty at home and abroad.

Retail sales also surprised to the upside, rising 1.7% yoy versus expectations of 0.8%. The strength suggests domestic demand remains more resilient than many feared, even as the industrial sector continues to face uneven momentum.

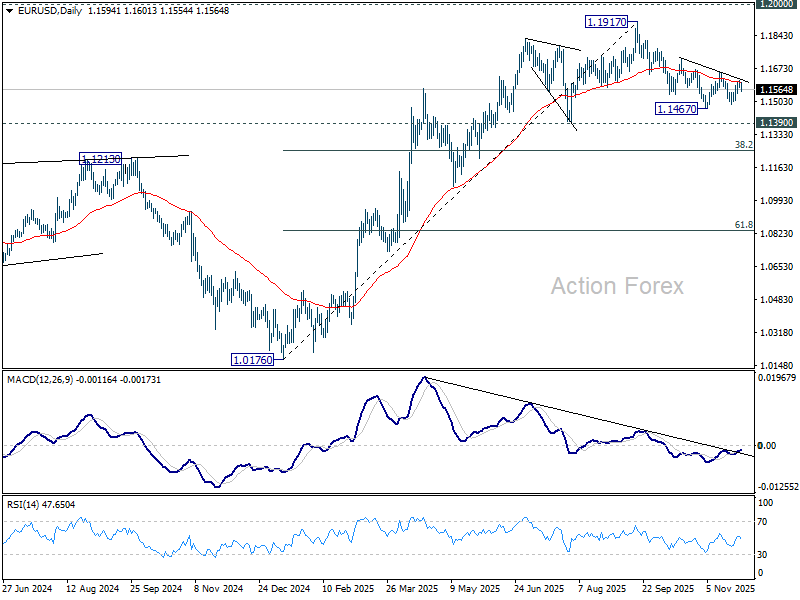

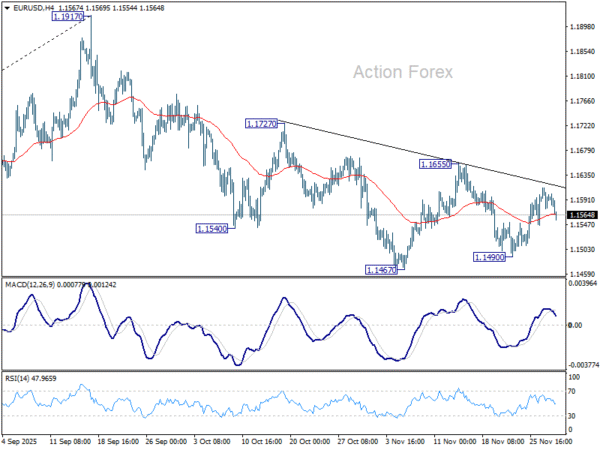

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1578; (P) 1.1596; (R1) 1.1615; More…

Intraday bias in EUR/USD remains neutral for the moment, as range trading continues. Further decline is expected with 1.1655 resistance intact. On the downside, below 1.1490 and 1.1467 will resume the whole decline from 1.1917 high. Next targets are 1.1390, and then 38.2% retracement of 1.0176 to 1.1917 at 1.1252. However, decisive break of 1.1655 will argue that fall from 1.1917 has completed, and turn bias back to the upside for 1.1727 resistance and above.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1328) holds, the up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.