BoJ Hike Back in Play After Ueda Comments; Yen Surge and 10Y JGB Yield Breakout – Action Forex

Risk aversion returned to Asia at the start of December, lifting Yen sharply across the board. The shift in sentiment coincided with a notable surge in Japanese government bond yields, with the 10-year jumping nearly 0.07 and breaking above 1.87%, its highest level in more than 15 years. .

A key catalyst was Governor Kazuo Ueda’s comments that the BoJ will weigh the “pros and cons” of raising interest rates at the December 18–19 meeting. While not definitive, the remark reintroduced the possibility of a near-term hike after weeks of speculation that political pressure might push the BoJ toward postponement.

Ueda’s position appears to have held firm following his meeting with Prime Minister Sanae Takaichi and senior economic officials last month, calming speculation that political considerations would force a delay. His tone today aligned with increasingly hawkish views emerging within the board, further reinforcing expectations that normalization remains a live discussion.

Even so, a December move is far from assured. The BoJ continues to emphasize wage trends, underlying inflation, and the durability of Japan’s recovery. But today’s developments likely nudge expectations toward either a December or, more plausibly, a January hike rather than a later timeline. Markets have quickly repriced that risk.

In currency markets, Yen is the clear outperformer today so far, followed by Dollar and then Euro. At the opposite end, Aussie is the weakest performer, with Swiss Franc and Kiwi also under some pressure. Sterling and Loonie are trading in the middle of the pack as cross-flows remain largely driven by Japan’s moves.

Whether these rankings hold through the session will depend on how long Japan-led risk aversion persists once Europe and the US open. Equity futures and broader risk assets will likely determine whether today’s defensive positioning extends into the next trading window or moderates as global liquidity increases.

Looking ahead, US data will dominate the week. A busy slate—ISM Manufacturing and Services, ADP employment, and personal income and spending with PCE inflation—will help refine expectations for early-2026 Fed policy. Additional releases, including Eurozone and Swiss CPI, Australia Q3 GDP, and Canada employment, round out the week.

In Asia, at the time of writing, Nikkei is down -1.96%. Hong Kong HSI is up 0.72%. China Shanghai SSE is up 0.50%. Singapore Strait Times is up 0.22%. Japan 10-year JGB yield is up 0.069 at 1.876.

Ueda signals December hike debate as BoJ reviews wage momentum

BoJ Governor Kazuo Ueda said the board will actively debate the “pros and cons” of raising interest rates at its December 18–19 meeting. He emphasized that the bank is now focused on whether firms’ “active wage-setting behavior” will persist, calling it a key determinant of the timing of the next hike.

Ueda noted that even with an increase, real interest rates would remain deeply negative, meaning policy would still be accommodative—more akin to “easing off the accelerator” than “applying the brakes.”

On the Yen, Ueda said Monday that further weakness is likely to push consumer inflation higher, a development that requires close monitoring when setting policy.

Japan’s PMI manufacturing finalized at 48.7, contraction eases and confidence hits year high

Japan’s Manufacturing PMI was finalized at 48.7 in November, slightly above October’s 48.2, but still pointing to contraction. S&P Global’s Annabel Fiddes noted that conditions remained challenging, with firms reporting “another solid decline” in new business as demand stayed weak across both domestic and external markets..

Despite the soft order flow, sentiment improved meaningfully. Business confidence rose to the strongest level since the start of the year, supported by expectations that market conditions will begin stabilizing in 2026. That optimism translated into a further rise in employment, with firms hiring in anticipation of a longer-term recovery in activity.

A key focus now shifts to the government’s newly announced stimulus package—the largest since the pandemic—which aims to accelerate investment in strategic sectors such as AI. Its success in lifting demand will be critical in determining whether the manufacturing sector can move out of contraction after a long period of subdued momentum.

China RatingDog PMI slips into contraction at 49.9 as production, demand stall

China’s RatingDog PMI Manufacturing fell back into contraction in November, dropping from 50.6 to 49.9 and missing expectations of 50.5. Founder Yao Yu said both production and demand slowed to levels near stagnation. While new export orders improved, the pickup was not enough to offset sluggish domestic demand, leaving overall new orders almost flat.

The loss of momentum weighed on hiring, purchasing activity, and inventory decisions. Manufacturers scaled back their workforce and procurement while adopting more cautious stock management. Inventories of raw materials and finished goods both declined, with the average inventory level hitting its lowest point in nearly three years. Also, raw material inventories fell for the first time in seven months. Pricing indicators also highlighted pressure on margins, with input prices rising while output prices continued to fall.

Official data released over the weekend offered mixed signals. NBS PMI Manufacturing edged up from 49.0 to 49.2, in line with expectations, hinting at modest stabilization. However, Non-Manufacturing PMI slipped from 50.1 to 49.5—the sector’s first contraction since December 2022—showing that weakness is now spreading beyond factories and reinforcing concerns about China’s softer near-term growth path.

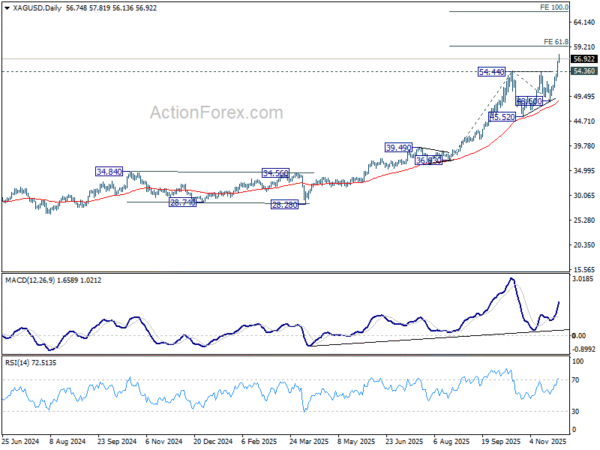

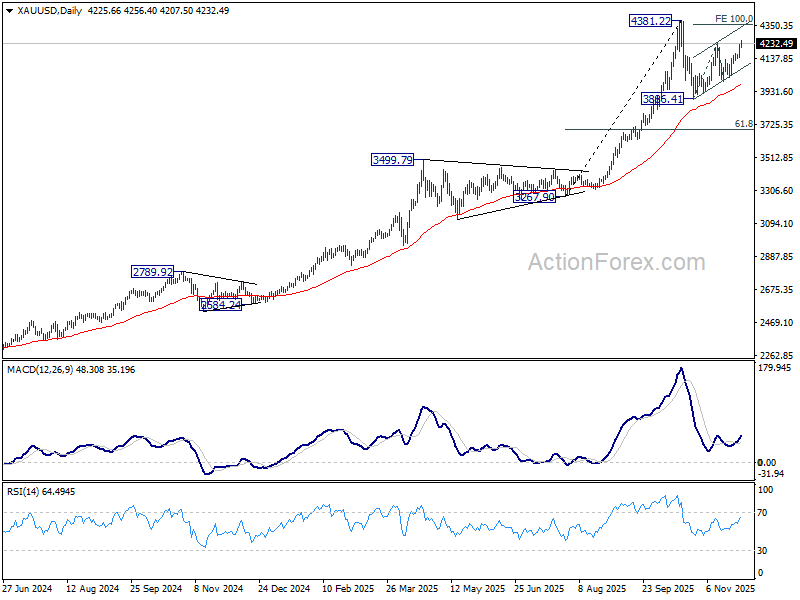

Silver extends record run and targets 60, leaving Gold lagging in range

Silver’s outperformance against Gold continued into December, with the metal surging to another record high late last week and extending gains in Asian trading today. The rally highlights a stark divergence within precious metals: while Silver pushes into uncharted territory, Gold remains trapped in its near-term range and capped well below its own record.

The strength in Silver reflects a powerful intersection of tight supply, firm physical demand, and intensifying industrial needs. Over the past year, the market’s underlying surplus has flipped into deficit, driven partly by the electrification of the vehicle fleet, rapid growth in artificial intelligence infrastructure, and continued expansion in photovoltaic applications. Together, these structural forces have pushed consumption higher while supply has struggled to keep pace.

Silver’s inherent material advantages—high thermal and electrical conductivity—make it difficult to substitute in EVs, advanced semiconductors, AI cooling systems, and solar technologies. With demand from these sectors accelerating and tariff-related distortions supporting domestic sourcing, investors have increasingly viewed Silver as a standout industrial-precious hybrid with strong forward momentum.

Technically, the breakout is equally convincing. Spot silver resumed its powerful uptrend by clearing the 54.44 resistance level and has now printed a fresh all-time high at 57.81. The next major upside zone sits at 61.8% projection of 36.93 to 54.44 from 48.60 at 59.4. The psychological 60 handle may cap the advance temporarily, but the broader trend remains decisively bullish as long as 54.36—now key support—holds. Sustained trading above 60 would open the door toward the 100% projection at 66.11.

Gold, by contrast, remains in consolidation. The rebound off 3,886.41 is developing as the second leg of the corrective pattern from 4,381.22 high. While further gains are possible near term, strong resistance is expected around the 100% projection of 3886.41 to 4344.86 from 3997.73 at 4356.18—close to the previous peak. Another pullback is still favored to complete the consolidation phase before the broader long-term uptrend reasserts itself.

US Data Deluge to Shape Fed’s Early-2026 Path

US data will set the tone this week, with markets preparing for a dense run of releases that could refine expectations for early-2026 policy. ISM Manufacturing and Services, ADP employment, and the latest personal income and spending numbers—including the Fed’s preferred PCE inflation gauge—form the core of the calendar. Together, these indicators will offer an updated read on demand momentum and how businesses are responding to a calmer tariff backdrop.

Despite the volume of data, none of the prints are likely to prevent the Fed from delivering another risk-management cut this month. Policymakers have signaled comfort in taking one more step to insure the economy against residual trade-related volatility and soft patches in hiring. The focus instead is shifting toward whether incoming numbers justify extending the easing cycle or pausing in Q1.

A rebound on the business side is increasingly plausible. With tariff risks easing after the extension of the US–China truce, firms appear better positioned to restore orders and investment decisions that were delayed earlier in the year. Any improvement in ISM new orders or employment components would support the argument that business confidence is stabilizing.

Consumer demand may also surprise on the upside. Two Fed rate cuts in September and October have already filtered into lower borrowing costs, providing marginal support to household spending. Strong personal consumption would suggest that the economy remains resilient even as labor-market gains moderate.

In Canada, the labor market takes center stage. At its October meeting, the BoC signaled that rates have now settled around the lower end of the neutral range, and further easing would require clear downside surprises in growth or inflation. A steady—or stronger-than-expected—jobs report would reinforce the BoC’s message that the bar for additional cuts is high.

Australia’s Q3 GDP is another important release, expected to show robust growth. Following last month’s upside inflation surprise, more strong data would underpin the case for the RBA to maintain its pause through Q1. Whether a full easing case still exists for 2026 is unclear, and policymakers are watching every incoming data point carefully.

Inflation figures from the Eurozone and Switzerland round out the global picture. But neither set of numbers is likely to shift the ECB or SNB from their current holding posture.

Here are some highlights for the week

- Monday: Japan PMI manufacturing final, capital spending; China RatingDog PMI manufacturing; Swiss retail sales, PMI manufacturing; Eurozone PMI manufacturing final; UK PMI manufacturing final; Canada PMI manufacturing; US ISM manufacturing.

- Tuesday: New Zealand terms of trade; Japan monetary base; Australian building approvals; Eurozone CPI flash, unemployment.

- Wednesday: Australia GDP; China RatingDog PMI services; Swiss CPI; Eurozone PMI services final, PPI; UK PMI services final; US ADP employment, industrial production, ISM PMI services.

- Thursday: Australia trade balance; Swiss unemployment rate; UK PMI construction; Eurozone retail sales; US jobless claims; Canada Ivey PMI.

- Friday: Japan household spending, leading indicators; Germany factory orders; Swiss foreign currency reserves; Eurozone GDP revision; Canada employment; US personal income and spending, PCE inflation, University of Michigan consumer sentiment.

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.91; (P) 156.25; (R1) 156.52; More…

USD/JPY dips low today as corrective pullback from 157.88 extends. While further fall cannot be ruled out, downside should be contained by near term channel support (now at 154.12) to bring rebound. Above 156.71 minor resistance will turn bias back to the upside. Further break of 157.88 will resume the whole rally from 139.87. Next target is 158.86 structural resistance, and then 161.94 high. However, firm break of the channel support will bring deeper correction to 55 D EMA (now at 152.86).

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 resistance turned support will dampen this bullish view and extend the corrective range pattern with another falling leg.