Dollar Slumps as Yen Surge Triggers Position Unwinds – ActionForex

Dollar fell broadly today, though the move lacked a clear single trigger. Fed expectations barely shifted, with December cut bets ticking up only marginally to 87%, not meaningfully different from last week. US yields were also steady to firmer, with 10-year Treasury yields recovering back above the 4% mark, offering no obvious impetus for a USD selloff. Yet sentiment remained shaky, with US equity futures dipping slightly as Japan-led risk aversion carried through Europe into the US session.

One plausible driver is position unwinding in USD/JPY. The Yen surged broadly after BoJ Governor Kazuo Ueda signaled that policymakers will “consider the pros and cons” of raising rates at the December meeting—his strongest hint yet that a hike could materialize this month. The comments triggered a recalibration of expectations, ending weeks of speculation that political pressure would push the BoJ toward delay.

Ueda added further fuel by saying the central bank would explain its future path once the policy rate reaches 0.75%. The message was clear: the debate now extends beyond one symbolic lift-off. Instead, the governor may be preparing the market for a meaningful, multi-step adjustment process.

Japan’s estimated neutral rate range—1.00% to 2.50%—remains broad, but it carries an important implication: the BoJ could deliver at least one or two more hikes without entering restrictive territory. With real rates still deeply negative, investors are reassessing the possibility that Japan’s tightening cycle may be more sustained than previously assumed.

That shift matters for USD/JPY, which has been heavily driven by rate differentials. The sudden unwind raises the question of whether the pullback could develop into a near-term bearish reversal. If that occurs, the Dollar’s weakness may broaden.

This comes at a sensitive moment for the greenback too. December is packed with high-impact US data: ISM Manufacturing and Services and PCE inflation this week, the FOMC meeting and expected rate cut next week, followed by NFP and CPI in the week after. With markets already leaning dovish, any additional softness in yields or US data could amplify USD pressure.

For now, Dollar is the worst performer today, followed by Loonie and then Aussie. Yen leads the board, trailed by Euro and Swiss Franc, while Sterling and Kiwi sit mid-pack. Whether this ranking holds depends heavily on whether USD/JPY selling stabilizes—or accelerates—into the US session.

In Europe, at the time of writing, FTSE is down -0.18%, DAX is down -1.38%. CAC is down -0.70%. UK 10-year yield is down -0.036 at 4.483. Germany 10-year yield is up 0.049 at 2.742. Earlier in Asia, Nikkei fell -1.89%. Hong Kong HSI rose 0.67%. China Shanghai SSE rose 0.65%. Singapore Strait Times rose 0.05%. Japan 10-year JGB yield rose 0.072 to 1.879.

UK PMI manufacturing finalized at 50.2, returns to growth for first time in 14 months

UK Manufacturing PMI was finalized at 50.2 in November, up from 49.7 and marking a 14-month high. S&P Global’s Rob Dobson said the month delivered further signs of recovery, with output rising for a second straight month and new orders stabilizing after more than a year of continuous decline. Business optimism also strengthened to a nine-month high.

What stands out is that this improvement came despite elevated business uncertainty ahead of the Autumn Budget, during which some firms maintained a cautious tone. With that political overhang now lifted, December could see a further boost in sentiment—though Dobson noted that the Chancellor’s “absence of significant growth-promoting measures” may limit the scale of any rebound in activity or investment.

Price indicators added a dovish twist. Rising competitive pressures and cooling cost inflation pushed factory gate prices lower for the first time in more than two years. This combination of a still-soft industrial recovery and easing price pressures reinforces the shift in BoE’s policy debate “away from inflation fears towards supporting economic growth”.

Eurozone PMI manufacturing finalized at 49.6, small economies improve, big ones falter

Country-level data showed a striking split. Six of the eight surveyed economies—led by Ireland at 52.8, Greece at 52.7, and the Netherlands at 51.8—remained in expansion. Italy and Austria also posted multi-year highs, pointing to broad stabilization beneath the surface. However, the aggregate picture remains weak because the region’s industrial heavyweights continue to contract. Germany fell to a nine-month low of 48.2, while France stayed at 47.8.

HCOB’s Cyrus de la Rubia emphasized that while most countries are improving, the downturn in the two largest economies overwhelms the progress elsewhere. France’s weakness reflects ongoing political uncertainty that has delayed investment decisions, whereas Germany is grappling with frustration over government direction and growing doubts about the country’s reform capacity.

Nevertheless, forward-looking sentiment improved across the bloc. Most firms expect production to rise over the next year, with Germany showing a gradual return of optimism and France shifting noticeably into positive territory. The improvement suggests that confidence may be stabilizing after a difficult year.

Ueda signals December hike debate as BoJ reviews wage momentum

BoJ Governor Kazuo Ueda said the board will actively debate the “pros and cons” of raising interest rates at its December 18–19 meeting. He emphasized that the bank is now focused on whether firms’ “active wage-setting behavior” will persist, calling it a key determinant of the timing of the next hike.

Ueda noted that even with an increase, real interest rates would remain deeply negative, meaning policy would still be accommodative—more akin to “easing off the accelerator” than “applying the brakes.”

On the Yen, Ueda said Monday that further weakness is likely to push consumer inflation higher, a development that requires close monitoring when setting policy.

Japan’s PMI manufacturing finalized at 48.7, contraction eases and confidence hits year high

Japan’s Manufacturing PMI was finalized at 48.7 in November, slightly above October’s 48.2, but still pointing to contraction. S&P Global’s Annabel Fiddes noted that conditions remained challenging, with firms reporting “another solid decline” in new business as demand stayed weak across both domestic and external markets..

Despite the soft order flow, sentiment improved meaningfully. Business confidence rose to the strongest level since the start of the year, supported by expectations that market conditions will begin stabilizing in 2026. That optimism translated into a further rise in employment, with firms hiring in anticipation of a longer-term recovery in activity.

A key focus now shifts to the government’s newly announced stimulus package—the largest since the pandemic—which aims to accelerate investment in strategic sectors such as AI. Its success in lifting demand will be critical in determining whether the manufacturing sector can move out of contraction after a long period of subdued momentum.

China RatingDog PMI slips into contraction at 49.9 as production, demand stall

China’s RatingDog PMI Manufacturing fell back into contraction in November, dropping from 50.6 to 49.9 and missing expectations of 50.5. Founder Yao Yu said both production and demand slowed to levels near stagnation. While new export orders improved, the pickup was not enough to offset sluggish domestic demand, leaving overall new orders almost flat.

The loss of momentum weighed on hiring, purchasing activity, and inventory decisions. Manufacturers scaled back their workforce and procurement while adopting more cautious stock management. Inventories of raw materials and finished goods both declined, with the average inventory level hitting its lowest point in nearly three years. Also, raw material inventories fell for the first time in seven months. Pricing indicators also highlighted pressure on margins, with input prices rising while output prices continued to fall.

Official data released over the weekend offered mixed signals. NBS PMI Manufacturing edged up from 49.0 to 49.2, in line with expectations, hinting at modest stabilization. However, Non-Manufacturing PMI slipped from 50.1 to 49.5—the sector’s first contraction since December 2022—showing that weakness is now spreading beyond factories and reinforcing concerns about China’s softer near-term growth path.

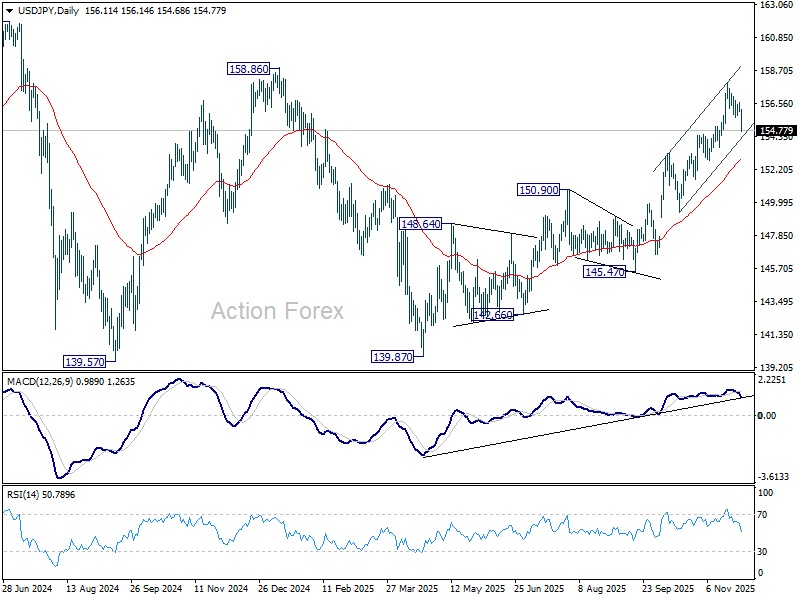

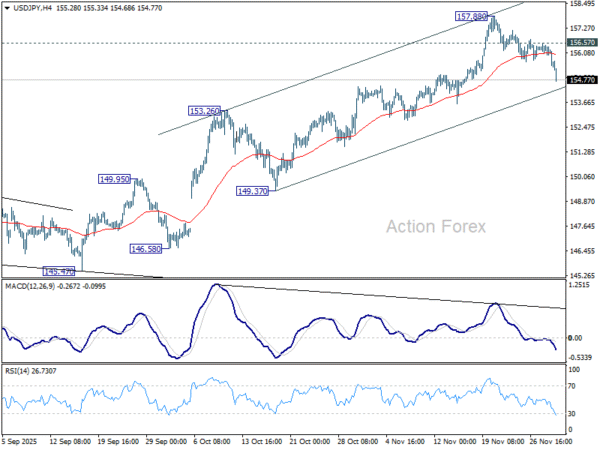

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.91; (P) 156.25; (R1) 156.52; More…

USD/JPY’s fall from 157.88 extends lower today and focus is now on near term rising channel support (now at 154.21). Strong support could be seen there to bring rebound. Above 156.57 minor resistance will bring retest of 157.88. Further break of 157.88 will resume the whole rally from 139.87. Next target is 158.86 structural resistance, and then 161.94 high. However, sustained break of the channel support will bring deeper correction to 55 D EMA (now at 152.86), and raise the chance of near term trend reversal.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 resistance turned support will dampen this bullish view and extend the corrective range pattern with another falling leg.