Markets Await US ADP and ISM Services as Dollar Drops Further – ActionForex

Risk sentiment was mixed in Asian trading today. The Nikkei outperformed thanks to a rebound in SoftBank and renewed enthusiasm for tech and AI names, but the index failed to break back above 50,000 psychological level—highlighting lingering hesitation among investors despite the intraday gains. Outside Japan, the tone was considerably weaker, particularly in Hong Kong, where declines in property and China-linked names weighed on the broader market. Regional divergence highlights an indecisive backdrop. Clarity may emerge later in the day as US markets react to the ADP employment report and ISM services data.

In the currency markets, Dollar is back under selling pressure through the session, extending a soft patch that some expect to persist into year-end. The gradual release of delayed US economic data is expected to show a softer underlying growth profile—especially in the job market—which could reinforce expectations for additional Fed easing next year. Additionally, a stable global risk environment only deepens headwinds for the greenback.

Fed rate-cut expectations continue to build as investors look for data confirming the slowdown in consumption and hiring. Combined with an improving risk backdrop globally, the Dollar is increasingly vulnerable to further downside, particularly if today’s ISM services numbers reinforce the softer tone seen in this week’s manufacturing data.

In the meantime, Aussie leads the days’ performance board, buoyed by hawkish comments from RBA Governor Michele Bullock that overshadowed the softer-than-expected Q3 GDP figures. Kiwi follows as the second-strongest, while Sterling also trades firmer on cross-flow demand. At the weaker end of the board, Dollar is the day’s worst performer so far, followed by Loonie and Swiss Franc. Euro and Yen sit mid-table.

In Asia, Nikkei closed up 1.14%. Hong Kong HSI is down -1.30%. China Shanghai SSE is down -0.54%. Singapore Strait Times is up 0.23%. Japan 10-year JGB yield rose 0.029 to 1.892, edging closer to 1.9 handle. Overnight, DOW rose 0.39%. S&P 500 rose 0.25%. NASDAQ rose 0.59%. 10-year yield fell -0.010 to 4.860.

RBA’s Bullock warns inflation persistence may require renewed tightening

RBA Governor Michele Bullock told the Senate Economics Legislation Committee that the bank remains on high alert for renewed inflation pressure and is prepared to act if price gains prove “more persistent” than expected. She noted that upcoming data in the next few months will be crucial in determining whether demand pressures are easing, adding that officials may still have to pivot back toward tightening if inflation shows signs of regaining strength.

Facing questions on past budget and inflation mis-projections, Bullock conceded the RBA “hasn’t done it yet” in bringing inflation sustainably back to target, and must continue working toward that objective. She stressed that the board must “keep working on this”.

With national debt set to exceed AUD 1 trillion and a deficit of AUD 42 billion projected, she noted that lower public and private savings—if paired with unchanged investment—could “put upward pressure on the neutral rate,” she said.”

But she added that that such an outcome is possible but contingent on both domestic and global forces. She emphasized that while the RBA can respond to domestic dynamics, but we don’t control global factors.”

Australia Q3 GDP misses forecast at 0.4%, per capita output stagnates

Australia’s economy expanded 0.4% qoq in Q3, below expectations for 0.7% and marking a softer outcome despite a 2.1% yoy rise from a year earlier. The headline result reflected steady domestic activity supported by private investment and household consumption. However, GDP per capita was flat, suggesting growth is tracking population gains rather than delivering broad-based improvement in living standards.

A key drag came from external accounts. Inventory rundown—used to support export volumes—subtracted meaningfully from growth, while net trade also weighed as imports rose faster than exports. The pattern highlights ongoing pressure on Australia’s trade balance even as domestic demand remains resilient.

Grace Kim, ABS head of National Accounts, described Q3 performance as “steady,” noting growth matched the post-pandemic quarterly average. Kim added that per capita GDP stagnation reflected population dynamics rather than outright weakness in activity, with the measure still 0.4% above its level a year earlier.

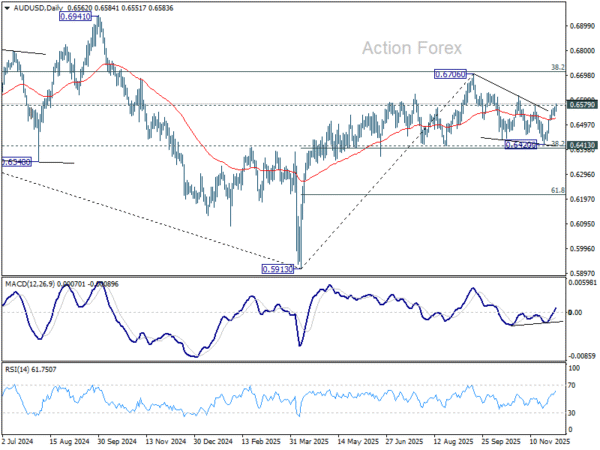

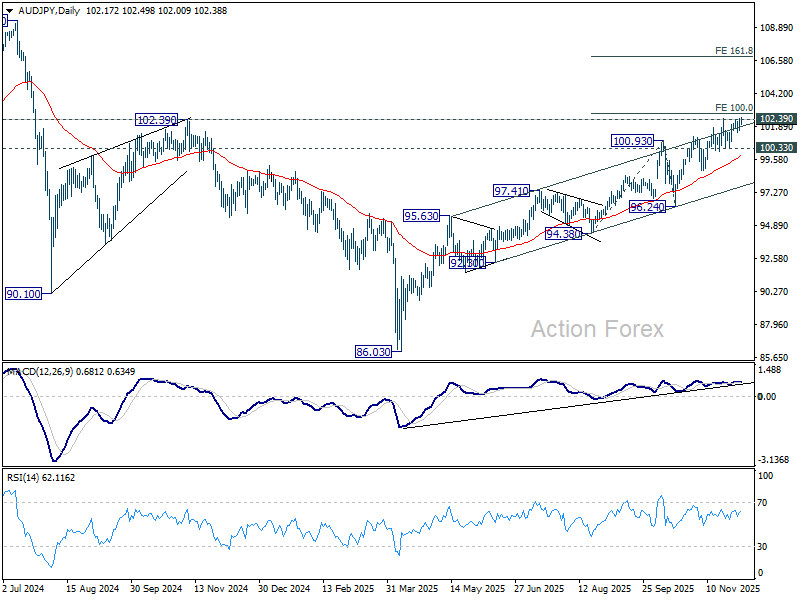

AUD/USD and AUD/JPY both eye breakouts after hawkish RBA remarks

Australian Dollar rallied sharply today after RBA Governor Michele Bullock signaled to Parliament that policymakers remain ready to tighten policy if inflation shows renewed persistence. Markets took her remarks as a clear indication that a rate hike in 2026 is possible—and that easing is firmly off the table for now. .

Soft Q3 GDP numbers briefly tempered expectations, but failed to stall Aussie’s advance. While quarterly growth undershot forecasts at 0.4% qoq, the 2.1% yoy expansion was still the strongest pace in two years, keeping concerns alive that domestic demand may be too resilient for inflation to retreat as quickly as hoped.

Markets now largely agree that rate cuts are off the table for an extended period, and a pre-emptive hike cannot be ruled out if upcoming data surprise on the upside.

Technically, AUD/USD’s break above 0.6579 reinforces that the correction from 0.6706 likely ended at 0.6420. The uptrend from the 2025 trough at 0.5913 may now be resuming, setting up a retest of 0.6706 peak. The key question is whether bullish momentum can build into that level or whether upside energy fades on approach.

AUD/JPY is also attempting a significant breakout as it challenges a dense cluster of resistance around 102. This zone includes the medium-term rising channel ceiling and the key 102.39 structural pivot. A clean break would represent an important bullish confirmation for longer-term AUD strength.

As long as 100.33 support holds, outlook for AUD/JPY stays bullish. Decisive break above 100% Projection of 94.38 to 100.93 from 96.24 at 102.79 should trigger upside acceleration towards 161.8% projection at 106.83.

Japan PMI services holds strong at 53.2, optimism hits year high

Japan’s Services PMI was finalized at 53.2 in November, edging up from 53.1 in October. Composite PMI also improved, rising to 52.0 from 51.5. S&P Global’s Annabel Fiddes noted “a number of positive developments,” with the sector consistently driving overall activity since mid-year.

Forward-looking indicators strengthened notably. Business optimism and hiring intentions both climbed to their highest levels since early 2025. New orders also accelerated modestly, the first pickup in three months, signaling a gradual improvement in underlying demand even if the pace remains mild. However, the positive momentum was accompanied by firmer inflation pressures. Input costs rose at the fastest rate since May, prompting another solid increase in selling prices as firms sought to protect margins.

With Japan’s new stimulus package now approved—aimed at supporting growth and offsetting rising costs—markets will be watching closely to see whether demand and output continue to improve in the coming months.

China’s RatingDog PMI services falls to 52.1, expansion loses pace, employment and margins under pressure

China’s RatingDog Services PMI eased in November, slipping from 52.6 to 52.1, while Composite PMI fell from 51.8 to 51.2. Both measures remained in expansionary territory, but the decline signaled moderation in growth momentum heading into year-end.

Yao Yu, Founder of RatingDog, said the services sector remained “relatively stable,” though November’s reading marked the weakest level since Q2. External demand showed mild improvement and offered “marginal support,” but domestic conditions were less encouraging.

Employment contracted again, profit margins came under pressure, and business expectations weakened—factors Yao described as the “main constraints” on the sector.

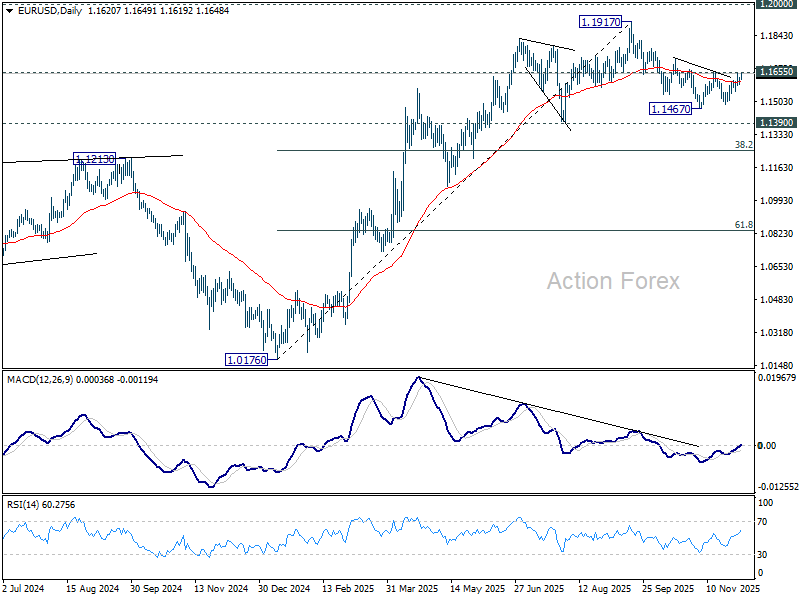

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1602; (P) 1.1615; (R1) 1.1638; More….

EIUR/USD rises slightly today but stays below 1.1655 resistance. Intraday bias remains neutral. On the upside, decisive break of 1.1655 will complete a head and should bottom pattern (ls: 1.1540, h: 1.1467, rs: 1.1490). That would argue that whole fall from 1.1917 has completed as a correction. Further rise should then be seen to 1.1727 resistance first. On the downside, though, below 1.1554 will turn bias to the downside for 1.1490 support first.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1345) holds, the up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.