Dollar Extends Losses on Deepening Labor Weakness, Euro Leads Weekly Gains – ActionForex

Dollar selling intensified again in early US session after another weak ADP employment report, marking the fourth decline in private payrolls over the past six months. The series of negative prints is now being viewed as a clear sign of deterioration in the labor market, prompting markets to extend their bearish repricing of the greenback ahead of next week’s FOMC meeting.

The latest ADP miss pushed the probability of a 25bps Fed rate cut this month to nearly 90%, with investors now treating a December move as all but baked in. Whether the Fed continues easing in Q1 remains less certain. Officials will have to weigh the ADP weakness against the upcoming official nonfarm payrolls report in two weeks—data that will arrive after the December policy decision and may heavily influence early-2026 expectations.

Adding to the uncertainty is speculation surrounding the Fed leadership transition. While not formally confirmed, markets widely expect US President Donald Trump to nominate his top economic adviser Kevin Hassett to replace Jerome Powell. Trump has suggested a formal announcement will come early next year, but traders are already gaming out the implications for forward guidance and institutional independence.

One emerging theme is the notion that Hassett could act as a “shadow Fed Chair” for several months before formally taking over, with markets potentially reacting as strongly to his comments as to those of Powell. If so, communication risks may rise into mid-2026 as investors adjust to a new center of gravity in policy messaging.

In FX, the Dollar sits firmly at the bottom of the weekly performance table for now, followed by Loonie and Kiwi. Euro leads, with Aussie and Sterling also posting gains. Yen and Swiss Franc are trading mid-range.

In Europe, at the time of writing, FTSE is down -0.14%. DAX is up 0.13%. CAC is flat. UK 10-year yield is down -0.025 at 4.448. Germany 10-year yield is down -0.015 at 2.740. Earlier in Asia, Nikkei rose 1.14%. Hong Kong HSI fell -1.28%. China Shanghai SSE fell -0.51%. Singapore Strait Times rose 0.36%.

US ADP jobs shock with -32k drop as small businesses cut deeply

US ADP private employment fell –32k in November, a sharp downside surprise versus expectations for 19k gain and marking one of the weakest readings of the year. Hiring declined in both major sectors, with goods-producing industries shedding -19k jobs and services losing -13k, highlighting broad cooling in labor demand.

The breakdown by firm size underscored the strain on smaller companies. Small businesses cut -120k jobs, overwhelmingly driving the headline decline, while medium-sized firms added 51k and large employers added 39k.

Wage growth also eased: pay for job-stayers slowed to 4.4% yoy from 4.5%, while job-changers saw pay growth fall to 6.3% yoy from 6.7%, continuing the trend of decelerating compensation pressures.

ADP’s Dr. Nela Richardson said the hiring backdrop has become increasingly uneven, citing “cautious consumers and an uncertain macroeconomic environment.” She emphasized that while the slowdown was widespread, the contraction was driven primarily by small businesses—often the most sensitive to shifts in demand and credit conditions.

Eurozone PMI composite finalized at 30-month high, mild Q4 acceleration expected

Eurozone Services PMI final rose to 53.6 in November from 53.0, marking a 30-month high and reinforcing the sector’s position as the main driver of regional growth. Composite PMI also improved to 52.8 from 52.5—another 30-month high—indicating that services strength more than compensated for continued manufacturing softness.

Country-level PMI Composite showed broad participation: Ireland led with a 42-month high at 55.8, while Italy also hit a 31-month high at 53.8. Germany (52.34) and Spain (55.1) softened slightly, and France returned to expansion at 50.4.

Hamburg Commercial Bank Chief Economist Cyrus de la Rubia said the data show “clear signs of recovery” across the services sector. The improvement was strong enough to lift overall Eurozone output, supporting expectations of a “slight acceleration” in Q4 growth. Though the headline index remains “far from a boom,” De la Rubia described the overall performance as “relatively robust,” underpinned by encouraging geographical breadth.

Price indicators delivered mixed but generally favorable signals for policymakers. Services selling-price inflation—which the ECB monitors closely—“weakened significantly” again, while wage growth c is gradually easing. Taken together, the data are likely to strengthen the ECB’s conviction in keeping interest rates on hold at the upcoming meeting.

UK PMI services finalized at to 51.3; Client caution and margin pressures build

UK Services PMI was finalized at 51.3 in November down from October’s 52.3. Composite PMI eased to 51.2 from 52.2, marking a clear loss of momentum after several months of improvement. S&P Global’s Tim Moore said the data show an “abrupt end” to the gradual recovery in order books seen since summer, with demand weakening in both domestic and export markets.

Lower workloads fed through to a slowdown in business activity growth, pushing expansion well below the post-pandemic trend. Firms also cut staffing levels at the fastest pace since February, pointing to an increasingly cautious operating environment. Survey respondents cited fragile client confidence, rising risk aversion and elevated policy uncertainty in the run-up to the Autumn Budget, with many delaying major spending decisions.

Competitive pressures intensified as firms struggled with weak sales pipelines. While input cost inflation accelerated—largely due to higher wages—selling price inflation rose at the slowest pace in nearly five years, signaling a squeeze on margins.

Swiss CPI back at 0.0% as broad price declines in November

Swiss inflation softened in November, with headline CPI falling -0.2% mom, in line with expectations, while annual inflation slowed from 0.1% yoy to 0.0%, undershooting forecasts of 0.1%. Core CPI also dipped, falling -0.1% yoy, with the annual rate easing from 0.5% yoy to 0.4%. The data highlight Switzerland’s continued weak inflation, keeping price growth far below levels seen elsewhere in Europe.

Both domestic and imported prices contributed to the decline. Domestic products fell -0.2% mom, while imported goods dropped a sharper -0.4% mom. On a yearly basis, domestic inflation cooled from 0.5% yoy to 0.4%, and imported prices remained deeply negative at -1.3% yoy. The persistent weakness in imported goods continues to anchor Swiss inflation near zero.

RBA’s Bullock warns inflation persistence may require renewed tightening

RBA Governor Michele Bullock told the Senate Economics Legislation Committee that the bank remains on high alert for renewed inflation pressure and is prepared to act if price gains prove “more persistent” than expected. She noted that upcoming data in the next few months will be crucial in determining whether demand pressures are easing, adding that officials may still have to pivot back toward tightening if inflation shows signs of regaining strength.

Facing questions on past budget and inflation mis-projections, Bullock conceded the RBA “hasn’t done it yet” in bringing inflation sustainably back to target, and must continue working toward that objective. She stressed that the board must “keep working on this”.

With national debt set to exceed AUD 1 trillion and a deficit of AUD 42 billion projected, she noted that lower public and private savings—if paired with unchanged investment—could “put upward pressure on the neutral rate,” she said.”

But she added that that such an outcome is possible but contingent on both domestic and global forces. She emphasized that while the RBA can respond to domestic dynamics, but we don’t control global factors.”

Australia Q3 GDP misses forecast at 0.4%, per capita output stagnates

Australia’s economy expanded 0.4% qoq in Q3, below expectations for 0.7% and marking a softer outcome despite a 2.1% yoy rise from a year earlier. The headline result reflected steady domestic activity supported by private investment and household consumption. However, GDP per capita was flat, suggesting growth is tracking population gains rather than delivering broad-based improvement in living standards.

A key drag came from external accounts. Inventory rundown—used to support export volumes—subtracted meaningfully from growth, while net trade also weighed as imports rose faster than exports. The pattern highlights ongoing pressure on Australia’s trade balance even as domestic demand remains resilient.

Grace Kim, ABS head of National Accounts, described Q3 performance as “steady,” noting growth matched the post-pandemic quarterly average. Kim added that per capita GDP stagnation reflected population dynamics rather than outright weakness in activity, with the measure still 0.4% above its level a year earlier.

Japan PMI services holds strong at 53.2, optimism hits year high

Japan’s Services PMI was finalized at 53.2 in November, edging up from 53.1 in October. Composite PMI also improved, rising to 52.0 from 51.5. S&P Global’s Annabel Fiddes noted “a number of positive developments,” with the sector consistently driving overall activity since mid-year.

Forward-looking indicators strengthened notably. Business optimism and hiring intentions both climbed to their highest levels since early 2025. New orders also accelerated modestly, the first pickup in three months, signaling a gradual improvement in underlying demand even if the pace remains mild. However, the positive momentum was accompanied by firmer inflation pressures. Input costs rose at the fastest rate since May, prompting another solid increase in selling prices as firms sought to protect margins.

With Japan’s new stimulus package now approved—aimed at supporting growth and offsetting rising costs—markets will be watching closely to see whether demand and output continue to improve in the coming months.

China’s RatingDog PMI services falls to 52.1, expansion loses pace, employment and margins under pressure

China’s RatingDog Services PMI eased in November, slipping from 52.6 to 52.1, while Composite PMI fell from 51.8 to 51.2. Both measures remained in expansionary territory, but the decline signaled moderation in growth momentum heading into year-end.

Yao Yu, Founder of RatingDog, said the services sector remained “relatively stable,” though November’s reading marked the weakest level since Q2. External demand showed mild improvement and offered “marginal support,” but domestic conditions were less encouraging.

Employment contracted again, profit margins came under pressure, and business expectations weakened—factors Yao described as the “main constraints” on the sector.

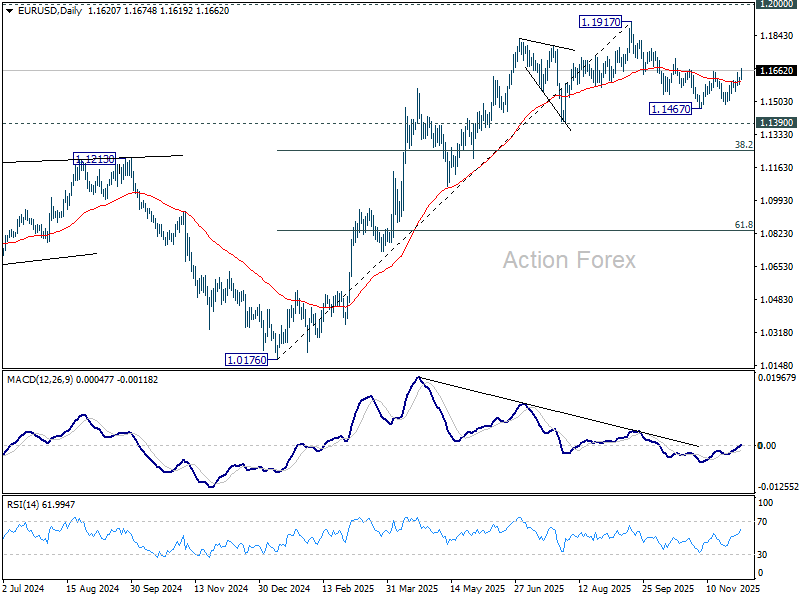

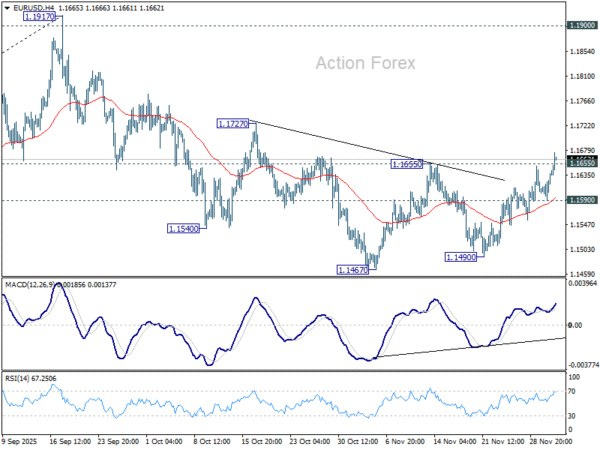

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1602; (P) 1.1615; (R1) 1.1638; More….

EUR/USD’s break of 1.1655 resistance argues that fall from 1.1917 has completed at 1.1467 as a correction. This is supported by the head and shoulder bottom pattern (ls: 1.1540, h: 1.1467, rs: 1.1490). Intraday bias is back on the upside for 1.1727 resistance. Firm break there will bring retest of 1.1917 high. Nevertheless, below 1.1590 minor support will mix up the outlook and turn bias neutral again.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1345) holds, the up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.