Muted Reaction to Strong US Claims; Japan’s Bond Markets Flash Caution – ActionForex

Global markets have steadied heading into US session, with equity futures pointing to a flat open after yesterday’s strong rally. Early optimism from Japan and Europe faded through the day, leaving investors cautious but not materially risk-off. The backdrop is one of consolidation rather than clear direction.

US jobless claims delivered a notable surprise, falling to their lowest level in more than three years. Yet market reactions were muted, reflecting scepticism that a single data point signals a genuine improvement in labor market momentum. With Fed funds futures still assigning nearly 90% probability to another 25bp “risk-management” cut next week, the report has not shifted the policy narrative.

Still, the data serve as a reminder that US labor conditions may stabilize as trade uncertainty eases. The extension of the US–China tariff truce in November for another year helps reduce one of the key macro headwinds that has weighed on business sentiment. If conditions continue to firm, both President Donald Trump and his expected Fed Chair pick, Kevin Hassett, may find it harder to justify aggressive, politically driven easing unless the data cooperate.

A separate but increasingly important development sits in Japan, where the 10-year JGB yield surged to 1.941%, its highest close since 2007. Rising yields translate into sharply higher government borrowing costs at a time when Prime Minister Sanae Takaichi is rolling out a massive stimulus package to offset cost-of-living pressures and support growth. Fiscal strains are likely to intensify if yields continue rising.

For the BoJ, the situation complicates an already delicate policy transition. Move too quickly, and the Bank risks pushing yields even higher, deepening fiscal stress. Move too slowly, and inflation pressures may re-accelerate. The policy dilemma is tightening, with global markets increasingly sensitive to how Governor Kazuo Ueda balances these conflicting risks.

Another concern is the narrowing Japan–US yield gap, which reduces the appeal of Yen-funded carry trades. A sudden reversal in Yen weakness could force a broader risk unwind, particularly among leveraged positions that have benefited from ultra-low JPY funding costs. The JGB move is therefore more than a local story—it is a potential global risk event.

Across the currency markets this week, Dollar remains anchored at the bottom of the performance ladder, with no signs of recovery. Loonie and Swiss Franc follow as the next weakest. On the stronger side, Yen leads with help from bond-market repricing, followed by Aussie and Sterling, while Euro and Kiwi sit in the middle of the pack.

In Europe, at the time of writing, FTSE is up 0.21%. DAX is up 0.90%. CAC is up 0.53%. UK 10-year yield is down -0.011 at 4.440. Germany 10-year yield is up 0.023 at 2.773. Earlier in Asia, Nikkei rose 2.33%. Hong Kong HSI rose 0.68%. China Shanghai SSE fell -0.06%. Singapore Strait Times fell -0.43%. Japan 10-year JGB yield rose 0.046 to 1.941.

US jobless claims fall sharply to 191k, lowest since 2022

US initial jobless claims fell sharply by -27k to 191k in the week ending November 29, far below expectations of 220k, and marking the lowest level since September 2022. The four-week moving average also by -9k eased to 215k.

Continuing claims slipped modestly by -4k to 1.939 million in the week ending November 22. Their four-week average edging down by -6k to 1.945 million, indicating some stabilization after earlier signs of softening.

The data stand in contrast to the recent deterioration seen in other labor indicators, including the weak ADP report, and highlight ongoing tightness in the job market despite clear signs of cooling elsewhere.

Eurozone retail sales stall in October as non-food demand softens

Eurozone retail sales were unchanged on the month in October, matching expectations and highlighting a subdued consumer environment heading into year-end. Category-level data showed mixed trends: spending on food, drinks and tobacco rose 0.3% mom, while non-food products (excluding fuel) fell -0.2% mom. Automotive fuel sales increased 0.3% mom, helping offset weakness elsewhere but not enough to lift the overall index.

Retail activity across the wider EU was also flat on the month, reinforcing the picture of stagnation in household consumption. The divergence among member states remained notable. Luxembourg posted the strongest monthly gain at 3.6% mom, followed by Estonia (1.7%) and Croatia (1.4). In contrast, Belgium saw a sharp -1.3% drop, with Austria (-0.6%), Ireland (-0.4%) and Sweden (-0.4%) also reporting declines.

BoJ’s Ueda: Neutral rate uncertainty keeps BoJ guessing how far to tighten

BoJ Governor Kazuo Ueda told lawmakers today that Japan’s neutral interest rate remains highly uncertain, describing it as a concept that can only be estimated within a “quite wide range.” He noted that the central bank is attempting to narrow that range and may disclose updated estimates once confidence improves.

Ueda added that the lack of clarity around the neutral rate means the BoJ must operate without a firm sense of how much tightening is ultimately appropriate. This ambiguity, he said, leaves uncertainty around “how far we should raise interest rates,” even as policymakers consider more conventional policy settings after years of ultra-accommodation. Current BoJ estimates place the nominal neutral rate between 1% and 2.5%.

His comments come days after signaling that the BoJ will weigh the “pros and cons” of a rate hike at the upcoming December meeting, a remark markets interpreted as the strongest indication yet that a move to 0.75% is under consideration.

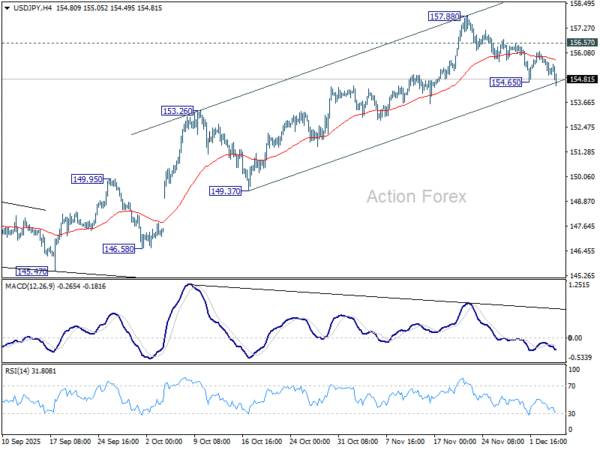

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 154.85; (P) 155.39; (R1) 155.77; More…

Intraday bias in USD/JPY remains neutral at this point. With near term rising channel floor intact, further rally is expected. Above 156.57 minor resistance will bring retest of 157.88. Further break there will resume the whole rally from 139.87. Next target is 158.86 structural resistance, and then 161.94 high. However, sustained break of the channel support will bring deeper correction to 55 D EMA (now at 153.13), and raise the chance of near term trend reversal.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 resistance turned support will dampen this bullish view and extend the corrective range pattern with another falling leg.