Dollar Softens Ahead of High-Stakes Central Bank Week; EU–China Trade Tensions Simmer – ActionForex

Dollar weakened mildly in Asian trading as the new week began, but the move lacked conviction, with most major pairs still confined to familiar ranges. With a light data calendar on tap today and little in the way of market-moving headlines, early-session flows were cautious. Eurozone Sentix Investor Confidence is the only notable release in Europe, while the U.S. calendar is completely empty.

That calm will not last. Market activity is almost certain to pick up sharply as the week progresses, with four major central bank meetings on deck. The headline event is Wednesday’s FOMC decision, where markets are fully priced for another 25bps “risk-management” cut. But RBA, BoC and SNB decisions also carry potential for surprise—even if none are expected to move rates this week.

This cluster of central bank risk suggests the FX market could see unusually choppy conditions, especially as investors reposition around forward guidance rather than the policy moves themselves. With Fed communication still unclear regarding the 2026 path and RBA pricing now tilting toward the possibility of a hike next year, volatility clusters may emerge across USD-majors and AUD-crosses.

Away from central banks, traders will also keep a close eye on geopolitics—particularly the brewing tensions between the EU and China. French President Emmanuel Macron used his state visit to Beijing earlier this month to issue an unusually blunt warning: unless China takes steps to narrow its rapidly growing trade surplus with Europe, the EU may resort to U.S.-style tariffs.

Macron described the current trade imbalance as “unsustainable,” arguing that China is “killing its own customers” by dramatically reducing imports from Europe. He stressed that European industry is trapped between Trump’s protectionism and China’s competitive pressure in industrial goods, calling it a “life or death” moment for the region’s manufacturing base.

In early Monday trading, Euro and Swiss Franc sit on the firmer side, followed by Yen, reflecting a mild preference for defensives. On the weaker side are Loonie and Dollar, followed by Sterling, while Aussie and Kiwi hold the middle ground. These early rankings are unlikely to hold for long, with the central bank bonanza almost certain to reorder the field.

In Asia, Nikkei rose 0.18%. Hong Kong HSI is down -1.02%. China Shanghai SSE is up 0.55%. Singapore Strait Times is down -0.41%. Japan 10-year JGB yield is up 0.002 at 1.955.

Japan’s wage picture improves but real incomes growth stays negative at -0.7%

Japan’s economic data delivered a familiar combination of improving nominal pay but still-depressed real incomes. Real wages fell -0.7% yoy in October, the 10th consecutive decline, though the rate of contraction moderated for the second month. Officials highlighted that fewer part-time roles and a higher share of full-time employees—who earn more—helped support headline income levels. Yet inflation of 3.4% yoy, driven mainly by food prices, continued to outpace wage gains.

Nominal earnings were considerably stronger, rising 2.6% yoy and beating forecasts for 2.2%. That marks a three-month high and extends the run of increases to 46 straight months, giving policymakers some evidence that wage momentum is holding up. Regular pay also expanded a robust 2.6% yoy, while bonus-driven special payments surged 6.7% yoy, providing a further boost. strain, limiting the lift to consumption.

The bigger disappointment came from growth data. Japan’s Q3 GDP was revised down to -2.3% annualized, from the initial -1.8%, making it the weakest quarter since 2023.

China’s exports rebound sharply by 5.9% yoy, US shipments remain deep in double-digit decline

China’s November trade data delivered a stronger-than-expected rebound, with exports surging 5.9% yoy to USD 330.35B, sharply reversing October’s -1.1% decline. The improvement marks the strongest performance since early 2024.

However, the headline strength masks continued weakness in China–U.S. trade, where shipments plunged -28.6% yoy, extending a run of eight straight months of double-digit declines. Despite the one-year tariff truce, effective levies remain elevated—averaging 47.5% on Chinese goods entering the U.S. and around 32% on American goods entering China—keeping bilateral flows under heavy pressure.

A clear divergence across regions stood out. Exports to ASEAN partners climbed more than 8% yoy, while shipments to the EU jumped nearly 15% y/y, underlining a rotation in China’s export momentum toward other major markets.

Imports, however, rose a softer-than-expected 1.9% yoy, pointing to still-cautious domestic demand despite policy easing efforts. With exports outpacing imports, China’s trade surplus widened to USD 111.68B in November.

Fed cut locked in, but guidance uncertain; RBA, BoC and SNB to hold the line

The week ahead brings one of the heaviest central bank line-ups, with the Fed, RBA, BoC and SNB all on deck. Yet only one of them—the Federal Reserve—is expected to move. Markets are firmly positioned for a 25bps risk-management cut, taking Fed funds to 3.50–3.75%, while the other three major central banks are widely expected to hold steady. Even so, the messaging from all four will matter for shaping early-2026 expectations.

For the Fed, Wednesday’s FOMC meeting is unquestionably the anchor event. The cut itself is not up for debate; market pricing still hovers near 90% change. What matters is what comes with it. One area to watch is the voting split, where attention will fall on whether ultra-dove Governor Stephen Miran again pushes for a 50bps move, and how many officials favor staying on hold. Any widening of dissent would reveal how fragmented the Committee has become.

The second focal point is the new economic projections. Back in September, the median dot implied only one more 25bps cut in 2026. With substantial macro uncertainty and incomplete data due to the government shutdown earlier this quarter, there may be caveats around precision. Still, the Fed’s broad views on growth, employment and inflation will deliver valuable clues on how policymakers interpret the recent slowing in activity.

Markets will also look to Chair Jerome Powell’s press conference, though expectations are modest. Powell is unlikely to lift the fog surrounding 2026. Internally, there is neither clarity nor consensus on how far or how fast cuts might proceed next year, especially as political noise grows louder ahead of leadership transition. His message may therefore lean heavily on data dependence.

In Australia, the RBA is expected to keep the cash rate unchanged at 3.60% on Tuesday. But the tone will be anything but neutral. October CPI surprised sharply to the upside at 3.8%, while trimmed-mean inflation ticked up to 3.3%. Combined with still-firm labor-market conditions, the inflation-control narrative has reclaimed center stage. Rate-cut expectations have evaporated in just two weeks.

Australia’s Big Four banks all expect the RBA to stay on hold, with three of them declaring the cutting cycle over. Reuters’ latest poll shows fewer than one-third of economists still expect one more cut by mid-2026—down from above 60% in November. Meanwhile, futures markets now price over a 70% chance of a rate hike by end-2026, marking a dramatic shift in sentiment.

Markets therefore expect a more hawkish-tilted message at the RBA’s final meeting of the year. While the base case remains “steady through 2026,” the balance of risk has clearly pivoted toward the upside. Acknowledging stronger demand momentum and sticky inflation may be enough to reinforce the idea that the next move could be up, not down.

The BoC follows on Wednesday, also expected to stay put at 2.25%. After signaling in October that the easing cycle had effectively ended, recent data—especially a string of strong labor-market reports—has given policymakers no reason to reopen the door to cuts. A Reuters poll taken even before the latest jobs surge showed 18 of 29 economists expecting no rate changes until at least 2027. That conviction has only strengthened.

Rounding out the week, the SNB meets Thursday and is widely expected to hold at 0.00%. Chair Martin Schlegel has repeatedly stressed that the threshold for returning to negative rates is very high. While Switzerland’s November CPI dipped back to 0.0% yoy, concerns about deflation are partially offset by recent Swiss Franc weakness and the US–Swiss trade deal, which slashes tariffs on Swiss exports from 39% to 15%. SNB will almost certainly stick to its current stance: ready to act if needed, but seeing no justification to move now.

Here are some highlights for the week:

- Monday: Japan labor cash earnings, current account, Q3 GDP final; China trade balance; Swiss SECO consumer climate; Eurozone Sentix investor confidence.

- Tuesday: Australia NAB business confidence, RBA rate decision; Germany trade balance.

- Wednesday: Japan PPI, China CPI, PPI; US employment cost index; BoC rate decision; FOMC rate decision.

- Thursday: New Zealand manufacturing sales; Japan BSI manufacturing;Australia employment; SNB rate decision; ; Canada trade balance; US trade balance, jobless claims.

- Friday: New Zealand BNZ manufacturing; UK GDP, trade balance.

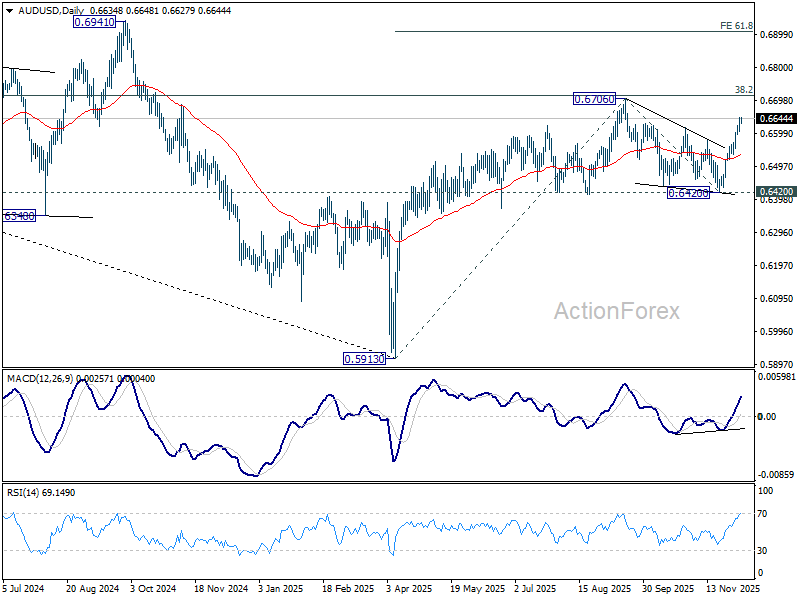

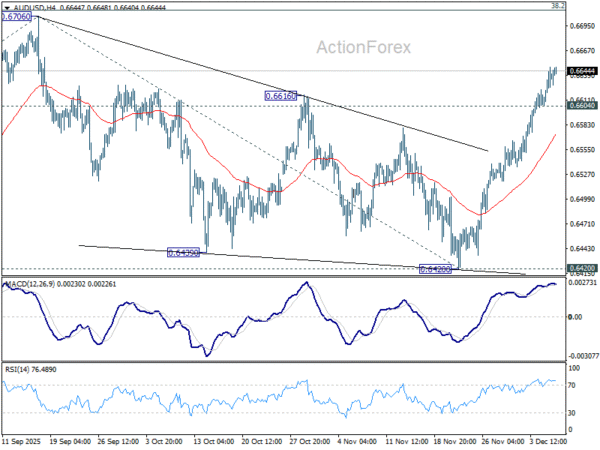

AUD/USD Daily Report

Daily Pivots: (S1) 0.6614; (P) 0.6632; (R1) 0.6658; More...

Intraday bias in AUD/USD remains the upside for retesting 0.6706 high. As noted before, rise from 0.5913 might be ready to resume. Decisive break of 0.6706 will confirm and target 61.8% projection of 0.5913 to 0.6706 from 0.6420 at 0.6910. On the downside, below 0.6604 minor support will turn intraday bias neutral and bring consolidations, before staging another rise.

In the bigger picture, the break of multi-year falling trend line resistance suggests that rise from 0.5913 is possibly reversing whole down trend from 08006 (2021 high). Decisive break of 38.2% retracement of 0.8006 to 0.5913 at 0.6713 will solidify this case, and bring further rally to 61.8% retracement at 0.7206. On the downside, however, firm break of 0.6420 support will suggest rejection by 0.6713 and retain medium term bearishness.