Markets Drift, Loonie Firms, Swiss Franc Slips, Aussie Awaits RBA – ActionForex

European markets are treading water today, and the same pattern is visible in US futures as investors hold their positions ahead of Wednesday’s FOMC decision. With volatility expected to rise sharply mid-week, traders appear content to let the market consolidate and avoid premature positioning.

Even in this holding pattern, pockets of activity stand out—most notably in the Canadian Dollar. Loonie’s strength extends the momentum from last week’s impressive jobs report, which reinforced expectations that the BoC will keep its policy rate unchanged at 2.25% later this week. The tone from policymakers is expected to confirm that the easing cycle is finished and that the central bank is now in a prolonged pause.

Another tailwind in the background is political. US President Donald Trump signaled openness to restarting trade discussions with Canada after what he described as a “very productive” conversation with Prime Minister Mark Carney during a World Cup draw event. Carney’s office later described the talks as “constructive,” offering a glimmer of optimism.

On the other side of the spectrum, Swiss Franc is under broad pressure today. SNB is widely expected to keep rates unchanged at 0.00% and reiterate that the threshold for returning to negative rates remains high. Yet speculation has emerged that policymakers could tilt toward a more dovish tone, possibly even hinting at negative rates sometime next year.

Some traders appear to be positioning for that scenario, helping drive CHF lower against most major peers. Still, it is far too early to draw definitive conclusions about the policy path for 2026. Any refusal by SNB to entertain dovish speculation this week could spark a swift reversal in the Franc’s performance.

Attention is also turning toward tomorrow’s RBA decision. A steady hold at 3.60% is effectively a foregone conclusion, but the focus is on Governor Michele Bullock’s messaging. Markets want to know whether she will explicitly shift the emphasis away from supporting growth and toward the still-unfinished battle against inflation.

While rate cuts are clearly off the table, expectations for a return to tightening in 2026 have grown louder. That said, some analysts caution that such speculation may be premature. Trimmed-mean inflation is only slightly above 3%, job ads have plateaued, and private-sector momentum remains uneven. Public-sector spending is also set to ease, creating additional downside risks.

Bullock’s communication will therefore be scrutinized line by line, particularly for any hint that the RBA is considering a policy pivot next year. For now, markets seem unsure whether she will validate or push back against emerging expectations for future hikes.

As of the latest positioning, Kiwi leads the performance board, followed by Loonie and then Euro. Swiss Franc is the weakest today, trailed by Yen and Sterling. Dollar and Aussie sit in the middle.

In Europe, at the time of writing, FTSE is down -0.02%. DAX is up 0.31%. CAC is down -0.12%. UK 10-year yield is up 0.014 at 4.495. Germany 10-year yield is up 0.042 at 2.844. Earlier in Asia, Nikkei rose 0.18%. Hong Kong HSI fell -1.23%. China Shanghai SSE rose 0.54%. Singapore Strait Times fell -0.54%. Japan 10-year JGB yield rose 0.02 to 1.972.

ECB’s Schnabel signals rates to stay put but next move likely a hike

ECB Executive Board member Isabel Schnabel struck a subtly hawkish tone in a Bloomberg interview, saying she is “rather comfortable” with market expectations that the ECB’s next move will be a rate hike. Still, she stressed that such expectations remain uncertain and that policymakers are “not currently” focused on when the next move might occur.

Schnabel reiterated that interest rates are “in a good place” and likely to remain there absent a major shock. What has changed, however, is the balance of inflation risks—which she said has “shifted to the upside”—a shift that naturally tilts the bias toward future tightening rather than easing.

Also, Schnabel flagged the possibility that the Eurozone’s natural rate of interest may be rising. Structural forces such as AI-driven investment and stepped-up public spending could lift the equilibrium rate over time, meaning the current stance may become increasingly accommodative if not adjusted. If policy drifts into a zone that is “too accommodative,” she said, that would be the moment to consider a further rate move.

Eurozone Sentix confidence edges higher to -6.2 but recovery still elusive

Eurozone Sentix Investor Confidence improved slightly in December, rising from -7.4 to -6.2, a touch better than expectations of -6.3. Both components strengthened, with Current Situation Index climbing from -17.5 to -16.5 and Expectations rising from 3.3 to 4.8. The figures reinforce a theme that has persisted through the past quarter: sentiment is no longer deteriorating, but neither is it showing convincing signs of a rebound.

Sentix noted that the Eurozone economy is “at best” stabilizing, even as global momentum improves across most other major regions. That divergence reflects the bloc’s inability to translate external tailwinds into domestic gains, with survey participants continuing to flag sluggish internal dynamics and weak demand conditions.

Germany remains the key drag heading into year-end. According to Sentix, recessionary forces in the Eurozone’s largest economy are still “having an impact,” and those pressures are filtering through to the wider region. Until German activity finds a firmer footing, the broader recovery narrative will remain tentative at best.

Japan’s wage picture improves but real incomes growth stays negative at -0.7%

Japan’s economic data delivered a familiar combination of improving nominal pay but still-depressed real incomes. Real wages fell -0.7% yoy in October, the 10th consecutive decline, though the rate of contraction moderated for the second month. Officials highlighted that fewer part-time roles and a higher share of full-time employees—who earn more—helped support headline income levels. Yet inflation of 3.4% yoy, driven mainly by food prices, continued to outpace wage gains.

Nominal earnings were considerably stronger, rising 2.6% yoy and beating forecasts for 2.2%. That marks a three-month high and extends the run of increases to 46 straight months, giving policymakers some evidence that wage momentum is holding up. Regular pay also expanded a robust 2.6% yoy, while bonus-driven special payments surged 6.7% yoy, providing a further boost. strain, limiting the lift to consumption.

The bigger disappointment came from growth data. Japan’s Q3 GDP was revised down to -2.3% annualized, from the initial -1.8%, making it the weakest quarter since 2023.

China’s exports rebound sharply by 5.9% yoy, US shipments remain deep in double-digit decline

China’s November trade data delivered a stronger-than-expected rebound, with exports surging 5.9% yoy to USD 330.35B, sharply reversing October’s -1.1% decline. The improvement marks the strongest performance since early 2024.

However, the headline strength masks continued weakness in China–U.S. trade, where shipments plunged -28.6% yoy, extending a run of eight straight months of double-digit declines. Despite the one-year tariff truce, effective levies remain elevated—averaging 47.5% on Chinese goods entering the U.S. and around 32% on American goods entering China—keeping bilateral flows under heavy pressure.

A clear divergence across regions stood out. Exports to ASEAN partners climbed more than 8% yoy, while shipments to the EU jumped nearly 15% y/y, underlining a rotation in China’s export momentum toward other major markets.

Imports, however, rose a softer-than-expected 1.9% yoy, pointing to still-cautious domestic demand despite policy easing efforts. With exports outpacing imports, China’s trade surplus widened to USD 111.68B in November.

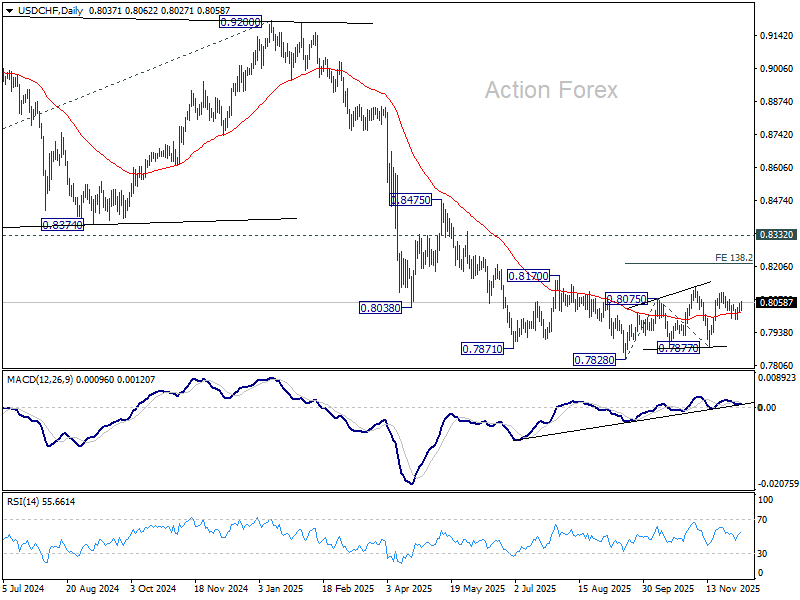

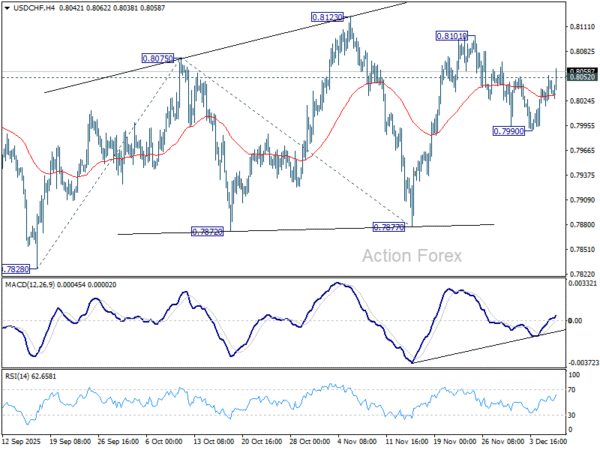

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8014; (P) 0.8034; (R1) 0.8067; More…

USD/CHF’s break of 0.8052 resistance suggests that pullback from 0.8101 has completed at 0.7990. Intraday bias is back on the upside for 0.8101 and then 0.8123. As noted before, price actions from 0.7828 are developing into a corrective pattern. Firm break of 0.8123 will target 138.2% projection of 0.7828 to 0.8075 from 0.7877 at 0.7812. For now, risk will stay on the upside as long as 0.7990 support holds, in case of retreat.

In the bigger picture, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low). Long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.