Yen Weakens, Yields and Stocks Surge, Focus Turns to NFP

Following strong rally in US stocks and treasury yield overnight, Yen is trading broadly lower today, together with Swiss Franc. Yen is also the worst performing one for the week, followed by Euro. On the other hand, Canadian Dollar is the winner for the week, followed by Aussie. Focus will turn to US job data today. Upside surprise there could prompt further rally in treasury yield and thus, pressure Yen further. But the reaction in other currencies would depend on the reactions in overall stock market movements.

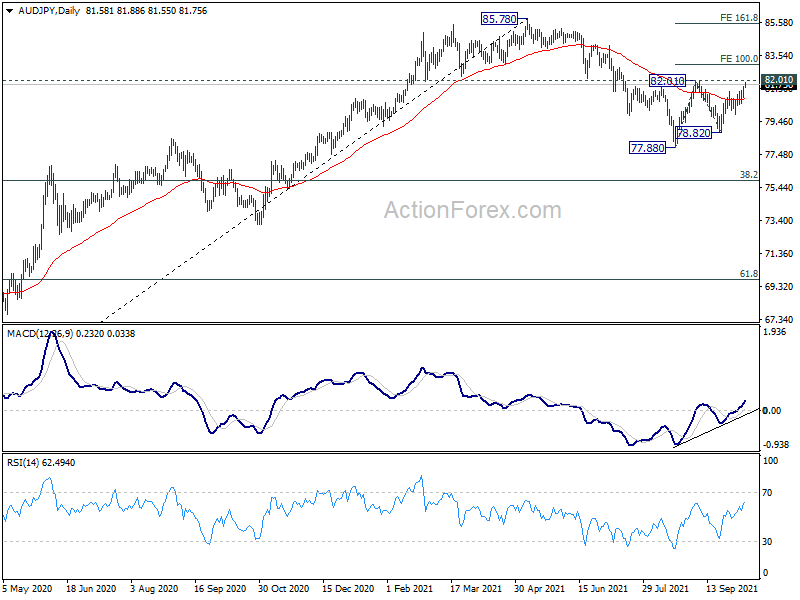

Technically, AUD/JPY is now eyeing 82.01 resistance with this week’s rally. Firm break there will firstly resume the rebound from 77.88. Secondly, it will affirm the case that correction from 85.78 has completed. Further rise would be seen to 100% projection of 77.88 to 82.01 from 78.82 at 82.95. Decisive break of 82.95 would probably bring upside acceleration towards 161.8% projection at 85.50, which is close to 85.78 high. Such development could happen if both stocks and yields surge after NFP today.

{kind=link}

In Asia, at the time of writing, Nikkei is up 1.69%. Hong Kong HSI is down -0.26%. China Shanghai SSE is up 0.33%. Singapore Strait Times is up 0.11%. Japan 10-year JGB yield is up 0.0043 at 0.082. Overnight, DOW rose 0.98%. S&P 500 rose 0.83%. NASDAQ rose 1.05%. 10-year yield rose 0.0047 to 1.571.

Fed Mester sees employment mandate met by end of next year

Cleveland Fed Bank President Loretta Mester said in a panel discussion yesterday that inflation in the US is “pandemic related” only. “Fundamentally, if it’s supply-side driven, that’s not something monetary policy should be responding to,” Mester added.

On monetary policy, she said, “our new strategy says, look, we’re not going to be moving until we have average inflation being 2% and we’re now going to be making up for past misses. I think we’ve basically met that part of the mandate.”

“My forecast is that we’ll meet that [employment] mandate by the end of next year, if things play out as I expect,” Mester said.

“My baseline is we’ll see inflation rates move back down as pent-up demand eases and supply-side challenges ease. But, as you know, that is taking longer than people thought and, in some cases supply chain issues are getting worse,” Mester said.

BoC Macklem: Goods reasons to believe inflation is temporary

BoC Governor Tiff Macklem said yesterday that there’s “a bit more persistence” in inflation than policy makers previously thought. But he added, ” I think there are good reasons to believe that they are temporary,”

“Our job as a central bank is to make sure that one-off increase in prices doesn’t become ongoing inflation… What we’re really looking for is to see any signs of spreading,” he added, noting that medium- to longer-term measures of expected inflation had not risen.

He also pointed to the “frictions” in the labor market, which took longer to work through. “We’ve never reopened an economy before. And I think what we’re seeing is reopening an economy is a lot more complicated than closing one,” he said.

ECB Lane: Eurozone far distance from inflation red zone

ECB Chief Economist Philip Lane said, “the red zone for everyone is if inflation became persistent at a number that’s immoderately above the inflation target. That’s a very far distance from where the euro area is.” He added, “we have to be the counterweight, honestly, in this debate.”

On inflation, he also said, “there’s solid reasons to believe that a lot of this is to do with the reopening of the economy and there’s very solid reasons to believe there’s a significant transitory component.”

China Caixin PMI services rose to 53.4, PMI composite rose to 51.4

China Caixin PMI Services rose to 53.4 in September, up from August’s 46.7, above expectation of 49.3. PMI Composite rose to 51.4, up from 47.2 in August.

Wang Zhe, Senior Economist at Caixin Insight Group said: “Both market supply and demand recovered, and improvement in the services sector was stronger than in the manufacturing sector. Impacted by the pandemic, overseas demand was weak. Employment was stable overall. Prices gauges remained high, indicating strong inflationary pressure.”

10-year yield rises as focus turns to NFP

US non-farm payrolls report is the major focus for today. Markets are expecting 500k job growth in September. Unemployment rate is expected to tick down from 5.2% to 5.1%. Average hourly earnings are expected to have risen 0.4% mom.

Looking at related job data, ADP report showed 568k growth in private sector jobs in the month. ISM manufacturing employment ticked up from 49.0 to 50.2. ISM services employment dipped slightly from 53.6 to 53.0. Four-week moving average of initial jobless claims dropped from 355k to 344k. Overall, the data support solid, but not spectacular, job growth in September.

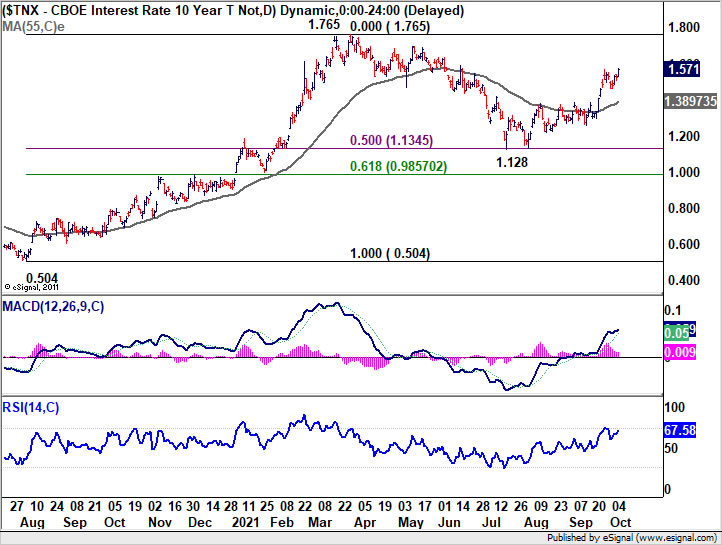

Bond market reactions to NFP today would be worth a watch. 10-year yield closed up 0.047 at 1.571 overnight, close to day high at 1.573. The development also indicates resumption of whole rise from 1.128. Positive reaction in yield to NFP would extend the rally, probably with upside acceleration, towards 1.1765 high. Such development could also lift USD/JPY through 112.07 near term resistance.

{kind=link}

Elsewhere

Japan labor cash earnings rose 0.7% yoy in August, versus expectation of 0.3% yoy. Household spending dropped -3.0% yoy, versus expectation of -1.5% yoy. Current account surplus narrowed to JPY 1.04T.

Eurozone will release trade balance in European session. While US non-farm payroll report, Canada job data is also a focus.

USD/JPY Daily Outlook

Daily Pivots: (S1) 111.36; (P) 111.51; (R1) 111.78; More…

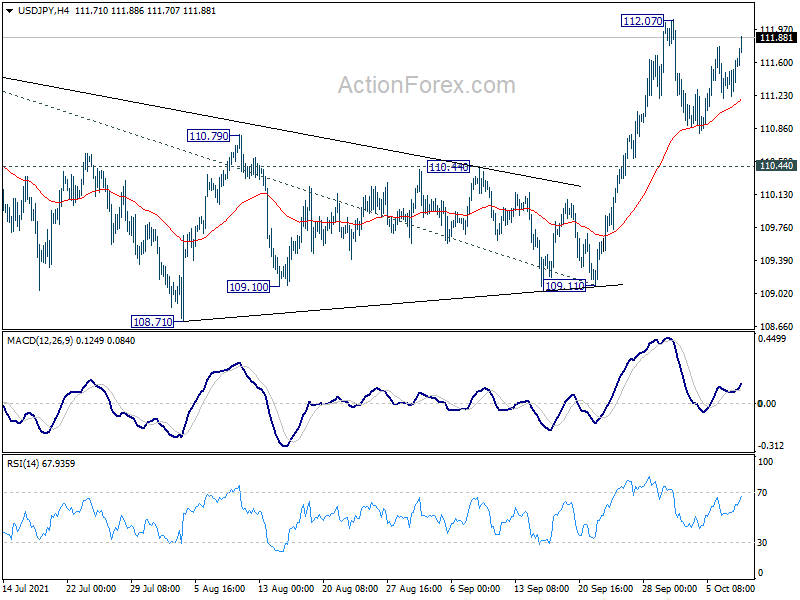

USD/JPY rebounds strongly but stays below 112.07 resistance. Intraday bias remains neutral first. Consolidation form 112.07 could still extend. But in case of another retreat, downside should be contained by 110.44 support. On the upside, above 112.07 will extend larger rise to 61.8% projection of 102.58 to 111.65 from 109.11 at 114.71 next. However, break of 110.44 will dampen the bullish case and turn focus back to 109.11 support.

{kind=link}

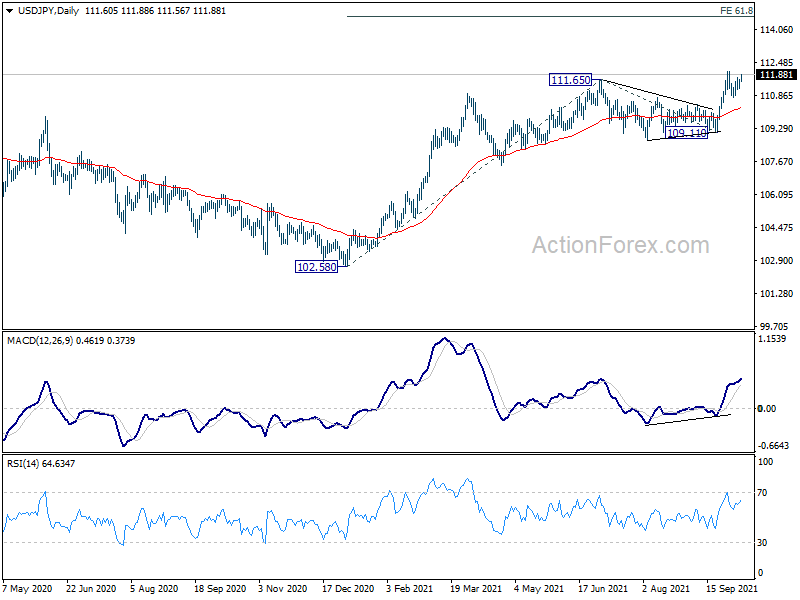

In the bigger picture, break of 111.71 resistance suggests that the whole corrective decline from 118.65 (2016 high) has completed at 101.18 (2020 low) already. Medium term bullishness is also affirmed as USD/JPY stays well above 55 week EMA (now at 108.60). Sustained trading above 111.71 will affirm this bullish case. Rise from 101.18 could then be resuming whole rally from 98.97 (2016 low) through 118.65. This will now be the preferred case as long as 108.71 support holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Aug | 0.70% | 0.30% | 0.60% | |

| 23:30 | JPY | Overall Household Spending Y/Y Aug | -3.00% | -1.50% | 0.70% | |

| 23:50 | JPY | Current Account (JPY) Aug | 1.04T | 1.15T | 1.41T | |

| 1:45 | CNY | Caixin Services PMI Sep | 53.4 | 49.3 | 46.7 | |

| 5:00 | JPY | Eco Watchers Survey: Current Sep | 43.4 | 34.7 | ||

| 6:00 | EUR | Germany Trade Balance (EUR) Aug | 15.7B | 17.9B | ||

| 11:00 | GBP | BoE Quarterly Bulletin | ||||

| 12:30 | USD | Nonfarm Payrolls Sep | 500K | 235K | ||

| 12:30 | USD | Unemployment Rate Sep | 5.10% | 5.20% | ||

| 12:30 | USD | Average Hourly Earnings M/M Sep | 0.40% | 0.60% | ||

| 12:30 | CAD | Net Change in Employment Sep | 61.2K | 90.2K | ||

| 12:30 | CAD | Unemployment Rate Sep | 6.90% | 7.10% | ||

| 14:00 | USD | Wholesale Inventories Aug F | 1.20% | 1.20% |