Dollar and Yen Down again as DOW Sets to Extend Record Run

Risk-on sentiment is pressuring Yen and Dollar today, while Euro and Swiss Franc are not too far away. On the other hand Sterling is the strongest, while Aussie leads other commodity currencies. US futures are trading higher suggesting that DOW and S&P 500 are on track to extend record ones. The question is whether buying would finally pick up some momentum. In other markets, Gold and Silver continue to trade in tight range while oil is firm at around 84.

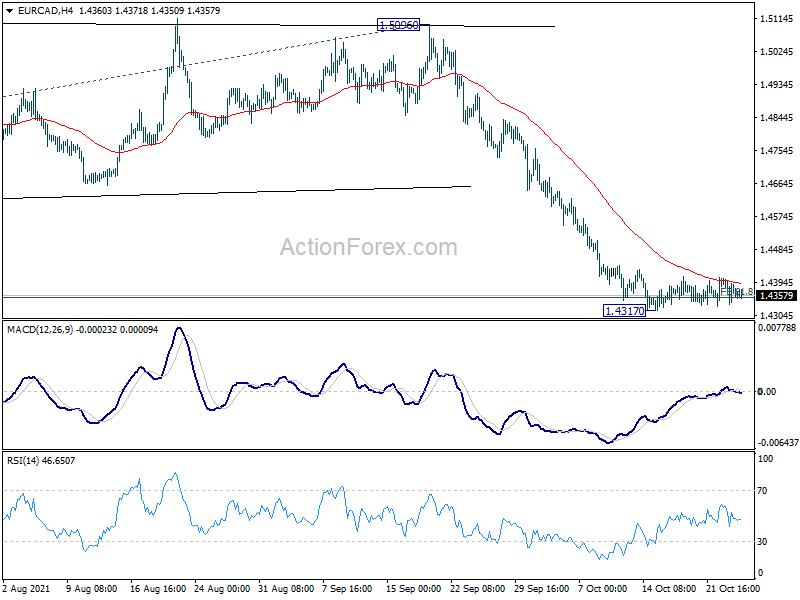

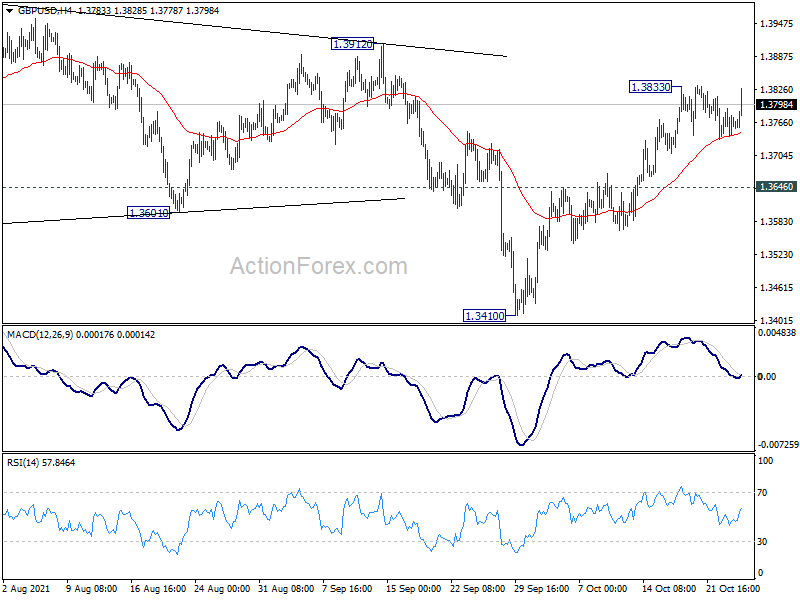

Technically, following EUR/AUD’s down trend breakout, EUR/GBP also resumed near term decline today. We’d now look at when EUR/CAD would break through 1.4317 temporary low and when EUR/CHF would break 1.0656. Also, we’d see when GBP/USD will break through 1.3833 temporary top, and if selling in Dollar would follow elsewhere.

{kind=link}

In Europe, at the time of writing, FTSE is up 0.59%. DAX is up 0.95%. CAC is up 0.70%. Germany 10-year yield is down -0.0104 at -0.123. Earlier in Asia, Nikkei rose 1.77%. Hong Kong HSI dropped -0.36%. China Shanghai SSE dropped -0.34%. Japan 10-year JGB yield rose 0.0036 to 0.104.

UK CBI retail sales performance jumped, but stock shortages bite

UK CBI said retail sales grew in the year to October at the faster pace than last month, balance up from 11% to 30%. Growth is expected to accelerate further next month to 35%. Orders growth accelerated from 20% to 48% but is expected to ease slightly back to 41% next month.

Ben Jones, CBI Principal Economist, said: “The UK’s economic recovery has been pretty bumpy lately and the same seems true of the retail sector. Sales performance has jumped around in recent months, while stock shortages continue to bite. Disruption to supply chains, combined with staff shortages and uncertain public health conditions mean retailers are finding it difficult to plan for the winter ahead.”

German Ifo: Supply problems now impacts manufacturing export

Germany’s Ifo export expectations dropped sharply from 20.5 to 13.0 in October, hitting the lowest level since February. Ifo said, “supply problems in intermediate products are now having an impact on manufacturing export”.

President of Ifo Clemens Fuest said: “In the electrical and electronics sector, export expectations have softened but remain at a high level, with companies continuing to expect good international business. However, the mood is bleaker in the chemical industry, where growth rates will be significantly slower. The situation is similar for the automotive industry. In the food and furniture industries, exports are expected to remain constant. The textile and leather industries are now preparing for declining international sales.”

US Yellen frankly raised issues of concern to China

US Treasury Secretary Janet Yellen held a virtual meeting with Chinese Vice Premier Liu He yesterday. In a statement, the US side said they “discussed macroeconomic and financial developments”, and “frankly raised issues of concern”.

On the Chinese side, it described in a statement that the meeting as “pragmatic, candid and constructive”. China expressed concerns on US tariffs, sanctions and urged fair treatment of Chinese companies.

Both sides agreed to further communications.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3743; (P) 1.3767; (R1) 1.3793; More…

GBP/USD rebounds after drawing support from 4 hour MACD, but stays below 1.3838 temporary top. Intraday bias remains neutral first. Further rise is expected with 1.3646 support intact. On the upside, above 1.3833 will target 1.3912 key structural resistance. Firm break there will indicate that the correction from 1.4248 is complete with three waves down to 1.3410. Further rally would then be seen to retest 1.4248 high. However, break of 1.3646 will turn bias to the downside for retesting 1.3410 low.

{kind=link}

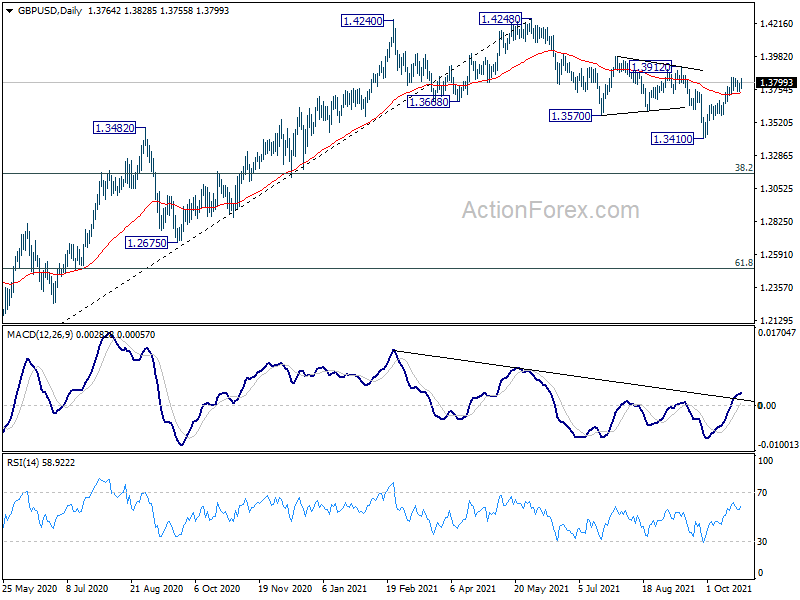

In the bigger picture, the structure of the fall from 1.4248 suggests that it’s a correction to the up trend from 1.1409 (2020 low) only. While deeper fall cannot be ruled out yet, downside should be contained by 38.2% retracement of 1.1409 to 1.4248 at 1.3164, at least on first attempt, to bring rebound. On the upside, firm break of 1.4376 key resistance (2018 high) will add to the case of long term bullish reversal. However, sustained trading below 1.3164 will revive some medium term bearishness and target 61.8% retracement at 1.2493.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Sep | 0.90% | 1.00% | 1.00% | |

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Aug | 20.00% | 19.90% | ||

| 13:00 | USD | Housing Price Index M/M Aug | 1.30% | 1.40% | ||

| 14:00 | USD | Consumer Confidence Oct | 108.4 | 109.3 | ||

| 14:00 | USD | New Home Sales Sep | 763K | 740K |