Stocks Surged, Dollar Mixed after Fed Tapering, BoE Next

US stocks surged to new records overnight despite Fed’s tapering announcement. Positive sentiments also continued in general in Asia. Dollar remains mixed for now and traders are probably awaiting tomorrow’s non-farm payroll report before taking a commitment. Focus will now turn to BoE rate decision, as Sterling is trading with an undertone.

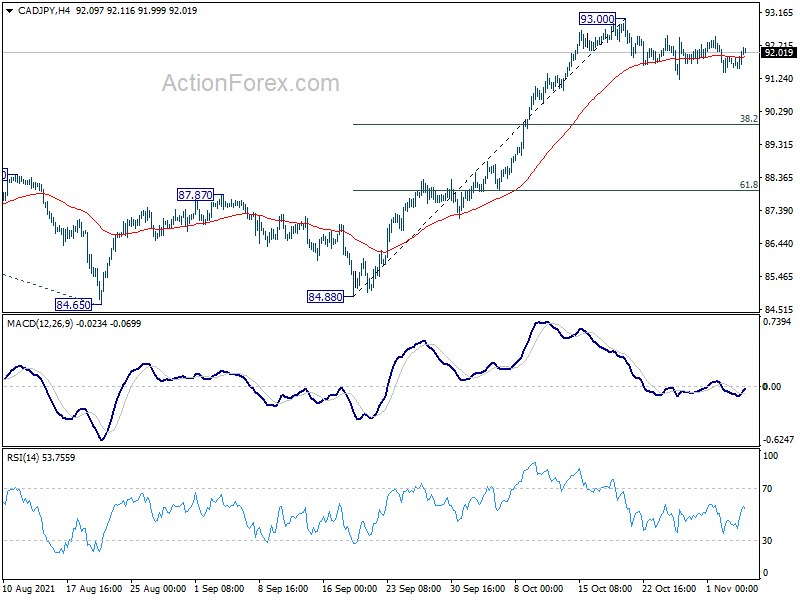

Technically, The general pull back in major global benchmark yield is capping Yen crosses’s rally attempts. But judging from the structure of the price actions, the crosses are clearly in consolations and upside breakouts are in favor, just when. We’d pay close attention to 133.44 resistance in EUR/JPY, 158.19 resistance in GBP/JPY and 93.00 resistance in CADP/JPY to gauge the timing of the breakouts.

{kind=link}

In Asia, at the time of writing, Nikkei is up 0.75%. Hong Kong HSI is up 0.27%. China Shanghai SSE is up 0.59%. Japan 10-year JGB yield is down -0.009 at 0.075. Overnight, DOW rose 0.29%. S&P 500 rose 0.65%. NASDAQ rose 1.04%. 10-year yield rose 0.030 to 1.579.

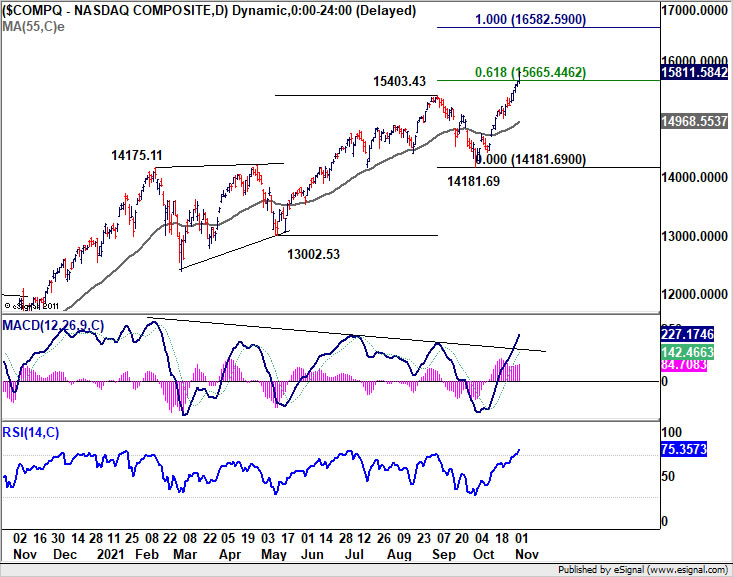

US stocks surged after Fed tapering, NASDAQ broke projection level

As widely anticipated, the Fed announced to taper its QE program. The Fed funds rate was kept unchanged at 0-0.25%. Fed continued to view inflation as “transitory” and did not appear to think that a rate hike was imminent.

Suggested readings on FOMC:

US stocks surged to new record highs overnight despite Fed’s tapering announcement. NASDAQ’s break of 61.8% projection of 13002.52 to 15403.43 from 14181.69 at 15665.44 is a sign that it’s in another acceleration phase. For now near term outlook will stay bullish as long as this week’s low at 15470.74 holds. Next target will be 100% projection at 16582.59.

{kind=link}

Australia retail sales rose 1.3% mom in Sep, down a record -4.4% qoq in Q3

Australia retail sales rose 1.3% mom, 1.7% yoy in September. For the quarter, sales dropped a record -4.4% qoq.

Ben James, Director of Quarterly Economy Wide Statistics said: “The Delta outbreak from late June led to protracted lockdowns in many mainland jurisdictions, with the restrictions causing many retailers to close their physical stores throughout the September quarter. This resulted in the largest quarterly fall in national sales volumes ever recorded.”

Also released, goods and services exports dropped -6% mom to AUD 44.97B in September. Goods and services imports dropped -2% mom to AUD 32.73B. Trade surplus came in at AUD 12.24B, versus expectation of AUD 12.22B.

BoJ Kuroda: YCC to continue even after the pandemic

BoJ Governor Haruhiko Kuroda said his met with new Japanese Prime Minister Fumio Kishida today, and discussed Japan, global economies and financial markets.

Kuroda said he explained BoJ’s monetary policy to Kishida, and reiterated the aim to achieve 2% inflation target. When asked about Fed’s tapering, he explained that BoJ is in different situation from western central banks.

Also, Kuroda said that yield curve control will continue even after the pandemic is contained.

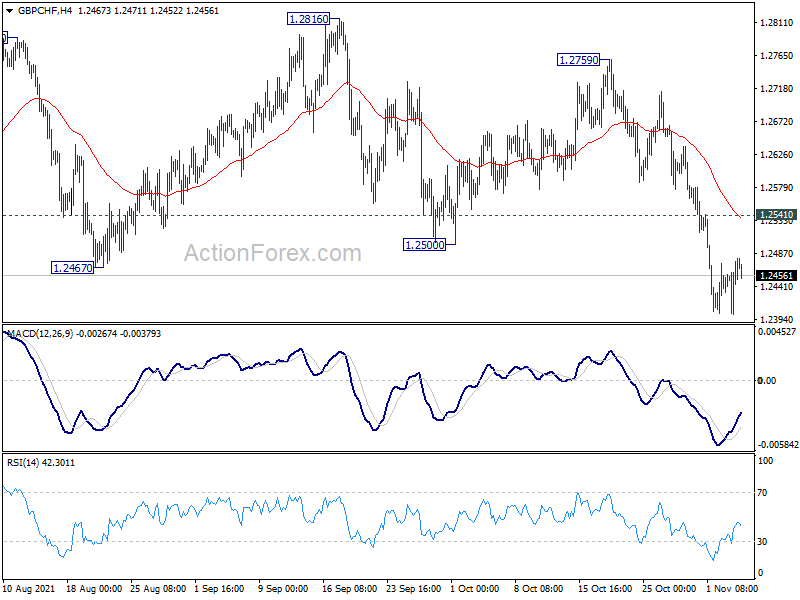

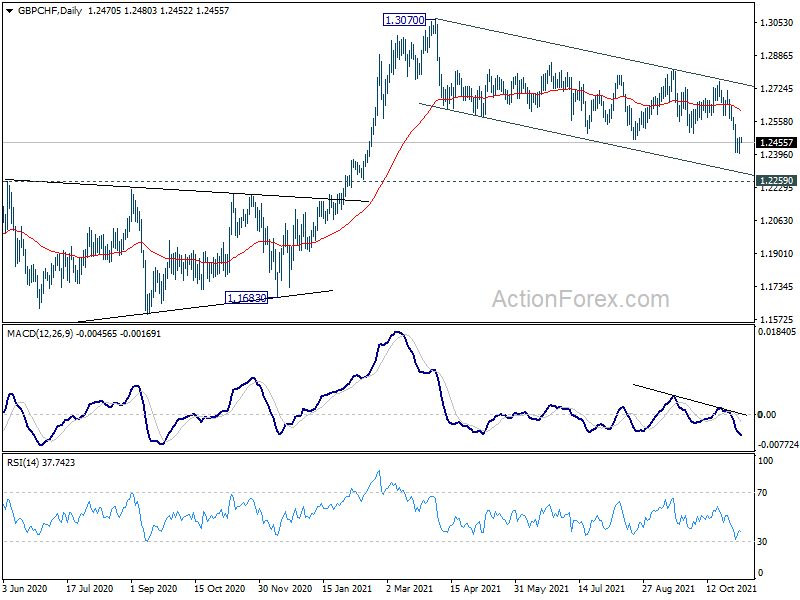

GBP/CHF extending near term fall as BoE awaited

Today’s BoE meeting is, as new BoE Chief Economist Huw Pill described, “live” and “finely balanced”. There is a thin majority of economists expecting no change. But market pricing suggests that a hike is not really a surprise. But in either case, the new economic projections, as well as voting would more likely be the things that move markets.

Here are some previews:

Sterling is generally soft ahead of BoE’ rate decision. GBP/CHF broke through 1.2467 support this week and resumed the whole decline from 1.3070. For now the structure of the fall suggests that it’s corrective in nature. Hence, even in case of deeper decline, we’d expect strong support from 1.2259 to contain downside and bring rebound.

Nevertheless, while break of 1.2541 minor resistance will bring recovery, break of 1.2759 resistance is needed to signal a near term bullish reversal. Otherwise, outlook will be neutral at best.

{kind=link}

{kind=link}

Elsewhere

Germany factor orders, Eurozone PMI services final and PPI, Swiss SECO consumer climate and UK PMI construction will be released in European session. Later in the day, Canada will release trade balance. US will release jobless claims, trade balance and non-farm productivity.

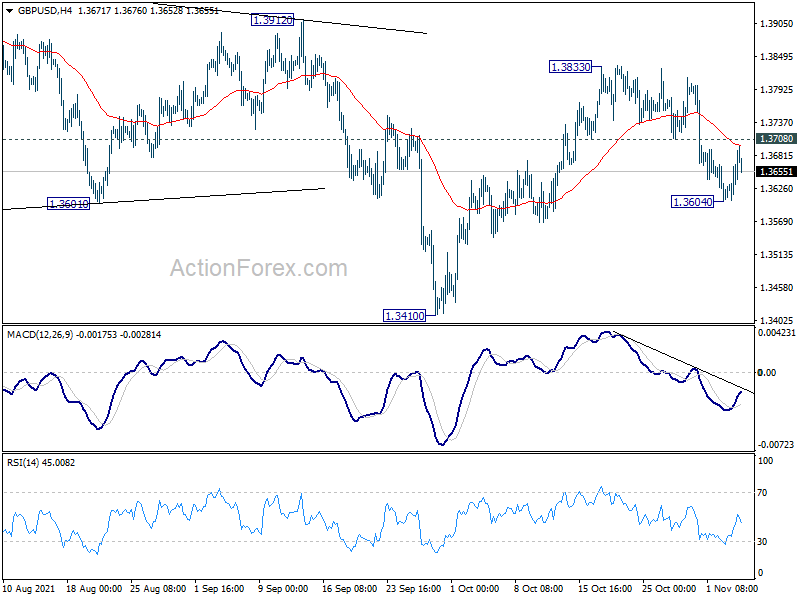

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3632; (P) 1.3662; (R1) 1.3717; More…

Intraday bias in GBP/USD is turned neutral with current recovery, but further decline is in favor with 1.3708 minor resistance intact. Below 1.3604 will target a test on 1.3410 low. Break there will resume larger decline from 1.4280. On the upside, though, break of 1.3708 minor resistance will turn bias back to the upside for 1.3833 resistance again. Decisive break of 1.3833 will re-affirm the case that corrective fall from 1.4248 has completed at 1.3410 already.

{kind=link}

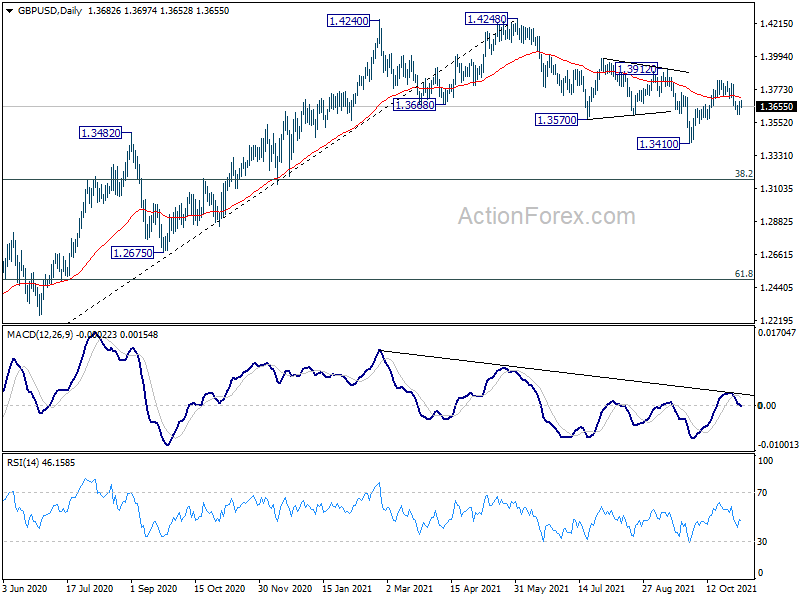

In the bigger picture, the structure of the fall from 1.4248 suggests that it’s a correction to the up trend from 1.1409 (2020 low) only. While deeper fall cannot be ruled out yet, downside should be contained by 38.2% retracement of 1.1409 to 1.4248 at 1.3164, at least on first attempt, to bring rebound. On the upside, firm break of 1.4376 key resistance (2018 high) will add to the case of long term bullish reversal. However, sustained trading below 1.3164 will revive some medium term bearishness and target 61.8% retracement at 1.2493.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:00 | NZD | ANZ Commodity Price Oct | 2.10% | 1.00% | 1.50% | |

| 00:30 | AUD | Trade Balance (AUD) Sep | 12.24B | 12.22B | 15.08B | 14.74B |

| 07:00 | EUR | Germany Factory Orders M/M Sep | 2.00% | -7.70% | ||

| 08:00 | CHF | SECO Consumer Climate Q4 | 5 | 8 | ||

| 08:45 | EUR | Italy Services PMI Oct | 54.5 | 55.5 | ||

| 08:50 | EUR | France Services PMI Oct F | 56.6 | 56.6 | ||

| 08:55 | EUR | Germany Services PMI Oct F | 52.4 | 52.4 | ||

| 09:00 | EUR | Eurozone Services PMI Oct F | 54.7 | 54.7 | ||

| 09:30 | GBP | Construction PMI Oct F | 54 | 52.6 | ||

| 10:00 | EUR | Eurozone PPI M/M Sep | 1.90% | 1.10% | ||

| 10:00 | EUR | Eurozone PPI Y/Y Sep | 15.20% | 13.40% | ||

| 11:30 | USD | Challenger Job Cuts Y/Y Oct | -84.90% | |||

| 12:00 | GBP | BoE Rate Decision | 0.10% | 0.10% | ||

| 12:00 | GBP | BoE Asset Purchase Facility | 875B | 875B | ||

| 12:00 | GBP | MPC Official Bank Rate Votes | 0–0–9 | 0–0–9 | ||

| 12:00 | GBP | MPC Asset Purchase Facility Votes | 0–2–7 | 0–2–7 | ||

| 12:30 | CAD | Trade Balance (CAD) Sep | 2.3B | 1.9B | ||

| 12:30 | USD | Initial Jobless Claims (Oct 29) | 277K | 281K | ||

| 12:30 | USD | Trade Balance (USD) Sep | -74.5B | -73.3B | ||

| 12:30 | USD | Nonfarm Productivity Q3 P | -1.50% | 2.10% | ||

| 12:30 | USD | Unit Labor Costs Q3 P | 5.20% | 1.30% | ||

| 14:30 | USD | Natural Gas Storage | 1.5B | 87B |