USD/JPY Rises Strong as Yield Rebounds, CAD Firm ahead of BoC

Strong rally in USD/JPY is the main focus in Asian session today, following the strong rebound in benchmark US treasury yields. Yen is also staying as the weakest one. But for now, Canadian Dollar and Australian Dollar are both stronger than the greenback. The Loonie’s rally slowed some what as WTI crude oil was rejected by 120 handle. But there is still upside prospect as hawkish BoC rate hike is awaited.

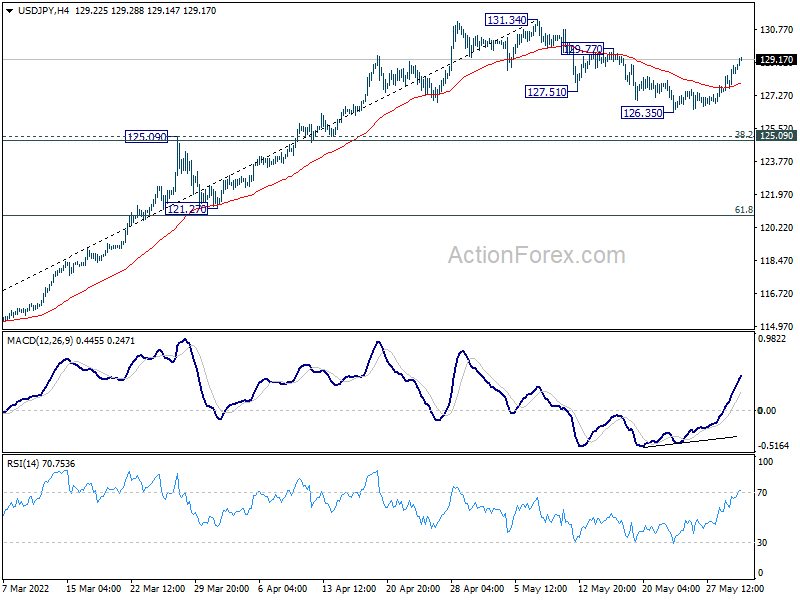

Technically, EUR/JPY’s break of 138.33 resistance and GBP/JPY’s break of 161.83 resistance both indicate more upside for retesting recent highs at 139.99 and 168.40 respectively. A focus will also be on 129.77 resistance in USD/JPY. Firm break there will affirm the case of broad based up trend resumptions in Yen pairs.

{kind=link}

In Asia, Nikkei closed up 0.65%. Hong Kong HSI is down -0.83%. China Shanghai SSE is down -0.35%. Singapore Strait Times is up 0.38%. Japan 10-year JGB yield is down -0.0042 at 0.236. Overnight, DOW dropped -0.67%. S&P 500 dropped -0.63%. NASDAQ dropped -0.41%. 10-year yield rose 0.101 to 2.743.

Fed Bostic: There could be significant reduction in inflation this year

Atlanta Fed President Raphael Bostic said yesterday that a pause in tightening in September might be a good idea, because market responses had been “far stronger than what we’ve historically seen.” “I want to make sure I truly understand the pace of change that’s associated with our policy response,” Bostic said.

By September, some of the uncertainty over the economy could be resolved. Bostic expected that could lead to a “pretty significant reduction in inflation.”

Yet, he’s “fully comfortable” to raise interest rates above neutral if inflation doesn’t come down. “The goal is to get inflation down. We’ve got to really tackle it in an intentional, persistent way,” he said. “I want to be open to both possibilities.”

BoJ Wakatabe: Necessary to persistently continue with monetary easing

BoJ Deputy Governor Masazumi Wakatabe said in a speech, “since rises in energy and food prices are mainly caused by cost-push factors from abroad, it is desirable to respond to them through measures other than monetary policy.”

“Possible options include fiscal policy and energy policy to reduce Japan’s dependence on petroleum and natural gas,” he added.

For monetary policy, “it is necessary to persistently continue with monetary easing and thereby continue to steadily support the virtuous cycle in the economy and maintain an environment in which wages rise,” he said.

“In addition, if downside risks to the economy materialize, the Bank should not rule out taking the necessary additional easing measures without hesitation.”

Released from Japan, PMI manufacturing was finalized at 53.3 in May, down from April’2 53.5. S&P Global noted softer expansions in production and incoming new business. Supply chain disruption encouraged firms to bolster safety stocks. Input prices rose at fourth-fastest pace in survey history.

Capital spending rose 3.0% in Q1, below expectation of 3.7%.

China Caixin PMI manufacturing rose to 48.1, still in contraction

China Caixin PMI Manufacturing rose from 46.0 to 48.1 in May, below expectation of 49.4. Caixin said output and new orders both declined at slower rates. Suppliers’ delivery times continued to lengthen markedly. Output charges fell, despite further rise in costs.

Wang Zhe, Senior Economist at Caixin Insight Group said: “The negative effects from the latest wave of domestic outbreaks may surpass those of 2020. It’s necessary for policymakers to pay attention to employment and logistics. Removing obstacles in supply and industrial chains and promoting resumption of work and production will help to stabilize market entities and protect the labor market. Also, the government should not only offer support to the supply side, but also put subsidies for people whose income has been affected by the epidemic on the agenda.”

Australia GDP grew 0.8% qoq in Q1, price deflator highest since 1988

Australia GDP grew 0.8% qoq in Q1, above expectation of 0.6% qoq. GDP also grew 3.3% through the year. Nominal GDP rose 3.7%. The GDP implicit price deflator increased 2.9%, the fastest rate since March quarter 1988.

The terms of trade rose 5.9%, with export (+9.6%) and import prices (+3.5%) both up strongly. Strong demand for Australia’s mining and agricultural commodities amidst supply constraints in other producing nations contributed to the rise in export prices.

The domestic final demand implicit price deflator rose 1.4%. This was the strongest growth since the introduction of the Goods and Services Tax, reflecting high levels of demand and increased input costs.

Also from Australia, AiG performance of manufacturing index dropped sharply from 58.5 to 52.4 in may.

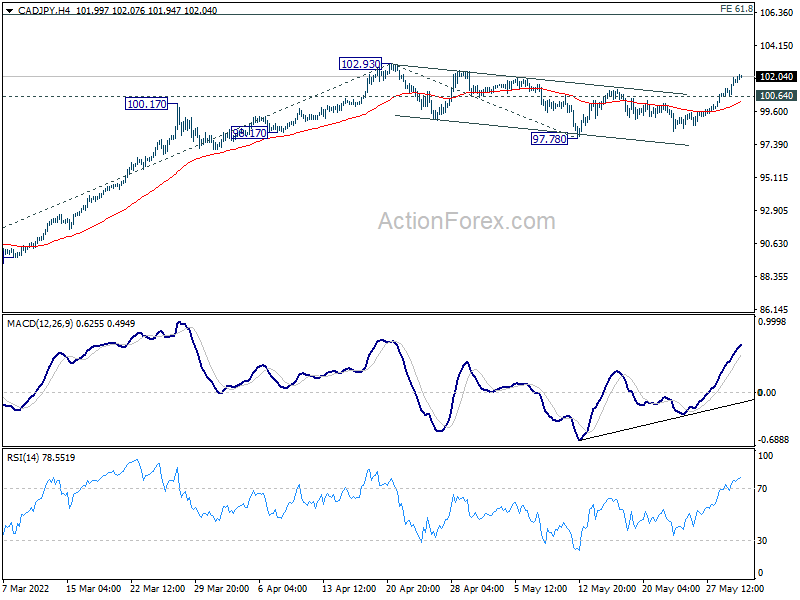

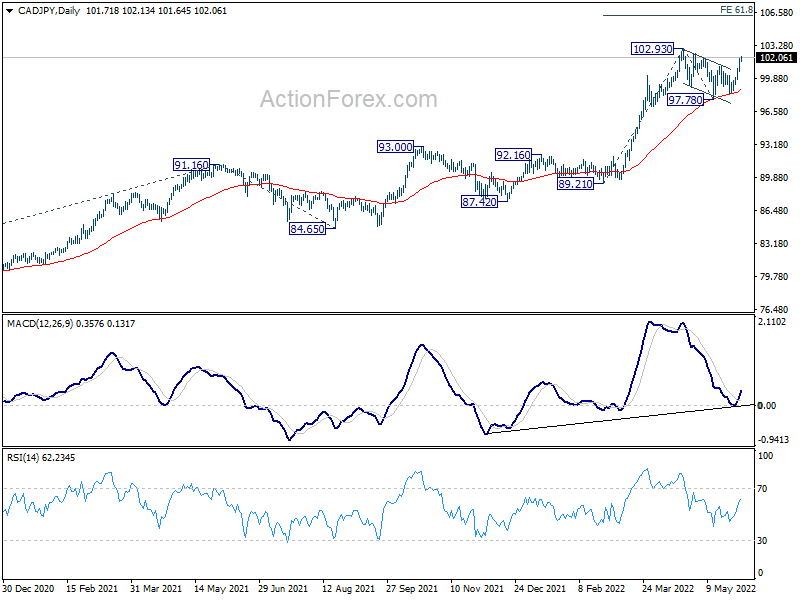

CAD/JPY ready for up trend resumption as BoC hike awaited

BoC is widely expected to raise the Overnight Rate by another 50bps to 1.50% today. Governor Tiff Macklem had recently noted that interest rates may need to go above the neutral range, estimated to be between 2% and 3%. Thus BoC should indicate that more tightening is still on the way. But Macklem would probably wait at least until July’s monetary policy report before talking about how high rates would top.

Some previews on BoC:

CAD/JPY’s strong rally this week suggests that correction from 102.93 has completed at 97.78 already, after drawing support from 55 day EMA. Further rise is now expected as long as 100.64 minor support holds. Firm break of 102.93 will resume larger up trend and target 61.8% projection of 89.21 to 102.93 from 97.78 at 106.25.

{kind=link}

{kind=link}

Looking ahead

Swiss PMI, Eurozone PMI manufacturing final and unemployment rate, UK PMI manufacturing final will be released in European session.

Later in the day, BoC rate hike is the main focus. US will release ISM manufacturing and Fed’s Beige Book report.

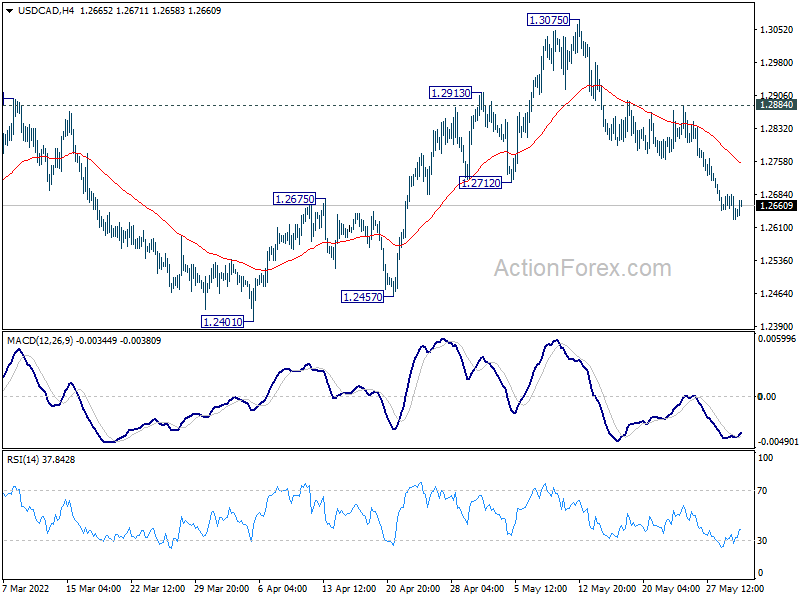

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2624; (P) 1.2656; (R1) 1.2682; More…

USD/CAD’s fall from 1.3075 is still in progress and intraday bias stays on the downside for 1.2401 support. Firm break there will argue that whole rebound from 1.2005 has completed. Deeper fall would then be seen to retest this low. On the upside, though, above 1.2884 minor resistance will revive near term bullishness and turn bias back to the upside for 1.3075 high.

{kind=link}

In the bigger picture, focus stays on 38.2% retracement of 1.4667 (2020 high) to 1.2005 (2021 low) at 1.3022. Sustained break there should confirm that the down trend from 1.4667 has completed after defending 1.2061 long term cluster support. Further rise would then be seen towards 61.8% retracement at 1.3650. However, rejection by 1.3022 will maintain medium term bearishness. Break of 1.2005 will resume the down trend from 1.4667 and that carries larger bearish implications too.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Mfg Index May | 52.4 | 58.5 | ||

| 23:01 | GBP | BRC Shop Price Index Y/Y Apr | 2.80% | 2.70% | ||

| 23:50 | JPY | Capital Spending Q1 | 3.00% | 3.70% | 4.30% | |

| 00:30 | JPY | Manufacturing PMI May F | 53.3 | 53.2 | 53.2 | |

| 01:30 | AUD | GDP Q/Q Q1 | 0.80% | 0.60% | 3.40% | |

| 01:45 | CNY | Caixin Manufacturing PMI May | 48.1 | 49.4 | 46 | |

| 06:00 | EUR | Germany Retail Sales M/M Apr | -5.40% | -0.50% | -0.10% | |

| 07:30 | CHF | SVME PMI May | 61.5 | 62.5 | ||

| 07:45 | EUR | Italy Manufacturing PMI May | 53.6 | 54.5 | ||

| 07:50 | EUR | France Manufacturing PMI May F | 54.5 | 54.5 | ||

| 07:55 | EUR | Germany Manufacturing PMI May F | 54.7 | 54.7 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI May F | 54.4 | 54.4 | ||

| 08:30 | GBP | Manufacturing PMI May F | 54.6 | 54.6 | ||

| 09:00 | EUR | Eurozone Unemployment Rate Apr | 6.70% | 6.80% | ||

| 13:30 | CAD | Manufacturing PMI May | 56.2 | |||

| 13:45 | USD | Manufacturing PMI May F | 57.5 | |||

| 14:00 | CAD | BoC Interest Rate Decision | 1.50% | 1.00% | ||

| 14:00 | USD | ISM Manufacturing PMI May | 54.5 | 55.4 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid May | 80.1 | 84.6 | ||

| 14:00 | USD | ISM Manufacturing Employment Index May | 50.9 | |||

| 14:00 | USD | Construction Spending M/M Apr | 0.50% | 0.10% | ||

| 18:00 | USD | Fed’s Beige Book |