Risk Sentiment Turns Sour ahead of US CPI

Euro’s post ECB rally was very short-lived, while market turned into risk-off mode later in US session. Negative sentiment continues in Asia today as US consumer inflation data is awaited. So far, Sterling is the strongest one for the week followed by Dollar, and then Canadian. Yen is the overwhelming loser, extending recent down trend of extended rally in global benchmark yields. Swiss Franc is second weakest even though it rebounds against Euro.

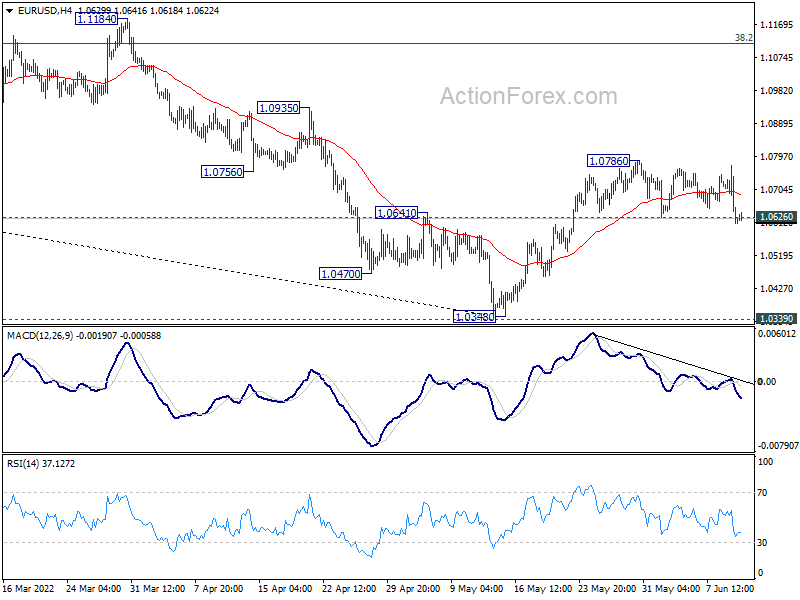

Technically, EUR/USD’s breach of 1.0626 minor support is a bearish sign. Sustained trading below this level will likely bring retest of 1.0348 low. USD/CAD’s breach of 1.2685 minor resistance also suggest that Dollar is on the way up for the near term. To confirm this development, attention will be on 1.2429 minor support in GBP/USD, and 0.7034 minor support in AUD/USD.

In Asia, Nikkei closed down -1.43%. Hong Kong HSI is up 0.01%. China Shanghai SSE is up 1.11% Singapore Strait Times is down -0.84%. Japan 10-year JGB yield is up 0.0026 at 0.253. Overnight, DOW dropped -1.94%. S&P 500 dropped -2.38%. NASDAQ dropped -2.75%. 10-year yield rose 0.015 to 3.044

China PPI slowed to 14-mth low, CPI unchanged

China PPI slowed notably from 8.0% yoy to 6.4% yoy in May, below expectation of 6.5% yoy. That’s also the lowest level in 14 months since March 2021. CPI was unchanged at 2.1% yoy, below expectation of 2.5% yoy. Core CPI, excluding food and energy, was unchanged at 0.9% yoy.

“In May, the pandemic control continued to improve, with overall sufficient supplies in the consumer market, CPI has decreased compared to last month, and the year-on-year increase remained stable,” said senior NBS statistician Dong Lijuan. “As a great amount of fresh vegetables entered the market and logistics gradually smooth, prices of fresh vegetables fell by 15 per cent”.

DOW lost -638pts as markets await US CPI

US stocks tumbled sharp in late trading overnight, as traders turned into defense mode ahead of today’s consumer inflation report. Headline CPI is expected to tick down from 8.3% yoy to 8.2% yoy in May. Core CPI is also expected to slow from 6.2% to 5.9% yoy.

Headline CPI appeared to have peaked at 8.5% yoy and core CPI at 6.5% yoy in March. Markets will look for validation that these levels were the peak. But the more important question is whether inflation is plateauing, or reversing. That is important for Fed officials to decide whether a pause in tightening is needed in September.

Technically, DOW’s picture is not looking good with the sharp -638pts decline, which suggests rejection by the falling 55 day EMA. If there is no come back to push for a strong rebound in DOW in the next few days, it will likely extend the correction from 36952.65 through 30635.76 low before finally finding a bottom.

{kind=link}

Elsewhere

New Zealand manufacturing sales rose 1.2% in Q1. Japan PPI slowed from 9.8% yoy to 9.1% yoy in May, below expectation of 9.8% yoy. Looking ahead, Italy industrial production is a feature in European session. Canada will release job data later in the day, together with US CPI and U of Michigan consumer sentiment.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0561; (P) 1.0668 (R1) 1.0724; More…

EUR/USD’s breach of 1.0626 minor support argues that rebound from 1.0348 has completed at 1.0786 already, after multiple rejection by 55 day EMA. Intraday bias is back on the downside for retesting 1.0348 low, and more importantly 1.0339 long term support. On the upside, though, break of 1.0786 will resume the rebound from 1.0348 to 1.1112 fibonacci resistance.

{kind=link}

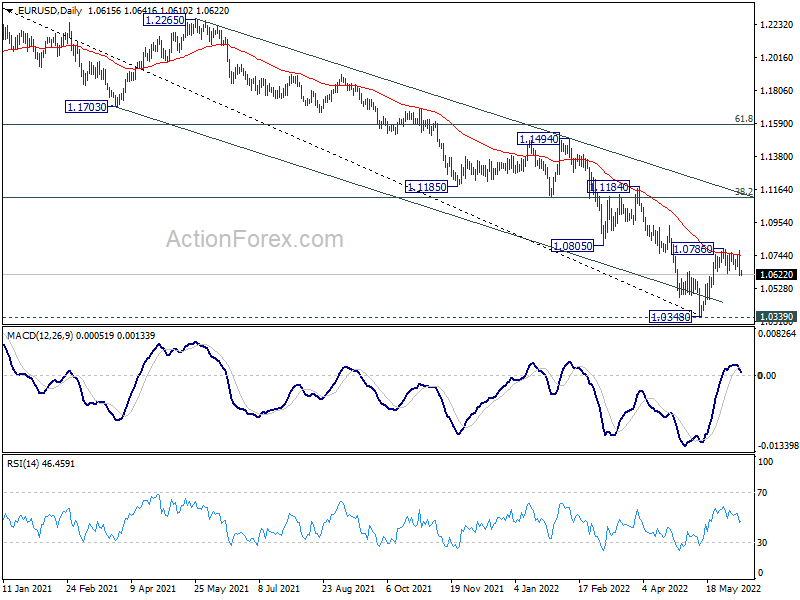

In the bigger picture, focus stays on 1.0339 long term support (2017 low). Decisive break there will resume whole down trend from 1.6039 (2008 high). Next target is 61.8% projection of 1.3993 to 1.0339 from 1.2348 at 1.0090. However, firm break of 1.0805 support turned resistance will delay this bearish case. Rise from 1.0348 is at least a correction to the down trend from 1.2348. Stronger rebound would be seen to 38.2% retracement of 1.2348 to 1.0348 at 1.1112.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Manufacturing Sales Q1 | 1.20% | 8.20% | 11.90% | |

| 23:50 | JPY | PPI Y/Y May | 9.10% | 9.80% | 10.00% | 9.80% |

| 01:30 | CNY | CPI Y/Y May | 2.10% | 2.50% | 2.10% | |

| 01:30 | CNY | PPI Y/Y May | 6.40% | 6.50% | 8.00% | |

| 08:00 | EUR | Italy Industrial Output M/M Apr | -1.60% | 0.00% | ||

| 12:30 | CAD | Net Change in Employment May | 28.5K | 15.3K | ||

| 12:30 | CAD | Unemployment Rate May | 5.20% | 5.20% | ||

| 12:30 | USD | CPI M/M May | 0.70% | 0.30% | ||

| 12:30 | USD | CPI Y/Y May | 8.20% | 8.30% | ||

| 12:30 | USD | CPI Core M/M May | 0.50% | 0.60% | ||

| 12:30 | USD | CPI Core Y/Y May | 5.90% | 6.20% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Jun P | 56.9 | 58.4 |