Bitcoin Breaks 20k, Sterling Awaits UK Data

Overall markets are rather steady in Asian session today. Even the free falling crytocurrencies are stabilizing slightly. Major Asian indexes, except Nikkei, are treading water. Dollar and Yen are softening slightly with Sterling. Aussie and Euro and mildly higher. But most major pairs and crosses are just stuck inside Friday’s range. Sterling would be a focus this week with a string of economic data featured, including CPI, retail sales, and PMIs.

Technically, Bitcoin broke through 20k handle over the weekend and stays below. It could now be heading back to pre pandemic high at 13855. In any case, firm break above 25083 resistance turned support is needed to be the first sign of bottoming. But even so, upside potential should be limited below 32368 resistance.

{kind=link}

{kind=link}

In Asia, at the time of writing, Nikkei is down -1.11%. Hong Kong HSI is down -0.30%. China Shanghai SSE is down -0.20%. Singapore Strait Times is up 0.08%. 10-year JGB yield is down -0.0263 at 0.206.

Fed Waller: Fed is all in on re-establishing price stability

Fed Governor Christopher Waller said in a speech over the weekend that “if the data comes in as I expect, I will support a similar-sized move at our July meeting,” referring to the 75bps hike at the June meeting. He added, “the Fed is ‘all in’ on re-establishing price stability.”

“It should not have been a surprise that the policy rate would rise fast in 2022. Rate hikes would need to be larger and more frequent, relative to the 2015-2018 tightening pace, to get back to neutral.”

“Looking back, should the Committee have signaled a steeper rate path once the liftoff criteria had been met? Perhaps another lesson is that giving forward guidance about liftoff should also include forward guidance about the possible path of the policy rate after liftoff.”

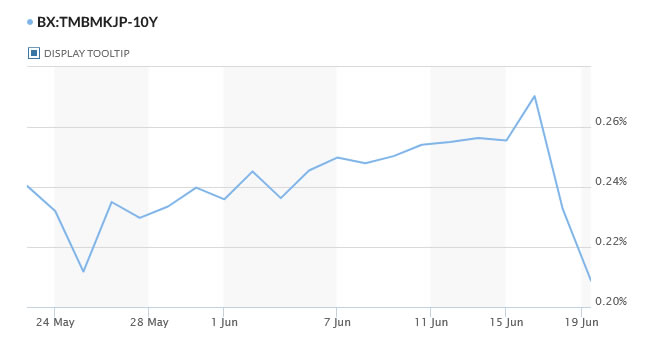

10-yr JGB yield back below 0.21% after massive BoJ purchases

BoJ offered to purchase unlimited amounts of 5- and 10-year JGBs today. That’s part of the central bank’s move to cap 10-year yield at 0.25%, after doubling down on maintaining this position and the overall ultra loose policy stance last Friday. Just last week, BoJ bought JPY 10.9T yen of government bonds, the most on record according to data compiled by Bloomberg.

BoJ’s move seems to be working well finally with 10-year JGB yield now down below 0.21% handle, after breaking above 0.27% last week.

{kind=link}

New Zealand BusinessNZ services rose to 55.2, back above average

New Zealand BusinessNZ Performance of Services Index rose from 52.2 to 55.2 in May. Activity/sales rose sharply from 53.3 to 59.6. But employment dropped from 51.0 to 48.5. New orders/business rose from 55.2 to 62.0. Stocks/inventories ticked down from 55.0 to 54.6. Supplier deliveries rose from 40.5 to 45.0.

BNZ Senior Economist Doug Steel said that “while the improvement was far from universal across components, reflecting many ongoing challenges across segments of the service sector, the overall outcome was the first above average result since the outbreak of Delta in August last year.”

UK CPI, retail sales, consumer confidence and PMIs highlights the week

UK data this week carry some weight, including CPI, consumer confidence and retail sales. For now, recession risks look higher than other major economies. The key lies in the dynamics between inflation and consumption. That’s the key to how far BoE’s tightening could continue. On the business side, PMIs will also be watched.

Other data to be watched include Eurozone PMIs, Germany Ifo, Canada CPI and retail sales; Australia PMIs; Japan PMIs and CPI, New Zealand consumer sentiment.

On central banks front, Fed Chair Jerome Powell will deliver his semi-annual testimony to Congress. No change in tune is expected, not that soon after last week’s FOMC press conference. RBA and BoJ will release meeting minutes while ECB will publish monthly economic bulletin.

Here are some highlights for the week:

- Monday: New Zealand BusinessNZ services index; Germany PPI.

- Tuesday: New Zealand Westpac consumer sentiment; RBA minutes; Swiss Trade balance; Eurozone current account; Canada retail sales, new housing price index; US existing home sales.

- Wednesday: New Zealand trade balance; BoJ minutes; UK CPI, PPI; Canada CPI; Eurozone consumer confidence.

- Thursday: Australia PMIs; Japan PMI manufacturing; Eurozone PMIs, ECB monthly bulletin; UK PMIs; US jobless claims, PMIs.

- Friday: Japan CPI, SPPI; UK Gfk consumer confidence, retail sales; Germany Ifo; US new home sales.

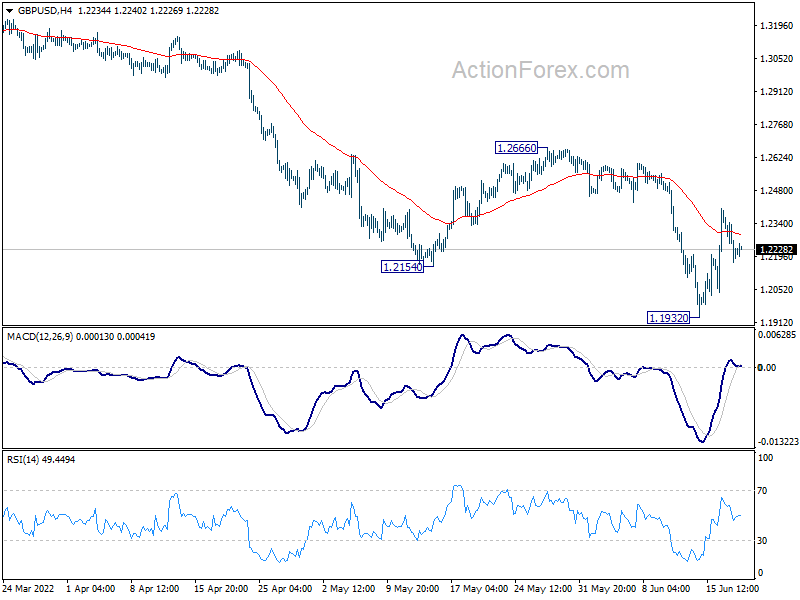

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2141; (P) 1.2254; (R1) 1.2335; More…

Intraday bias in GBP/USD stays neutral as consolidations continues. But outlook stays bearish as long as 1.2666 resistance holds. On the downside, break of 1.1932 will resume larger down trend from 1.4248. However, firm break of 1.2666 will suggest medium term bottoming and bring stronger rebound back towards 1.3158 support turned resistance.

{kind=link}

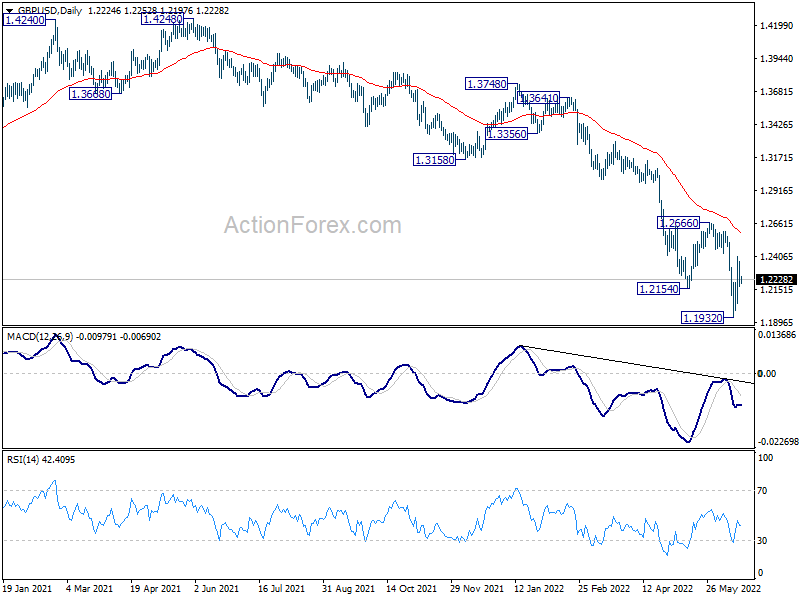

In the bigger picture, fall from 1.4248 (2018 high) could be a leg inside the pattern from 1.1409 (2020 low), or resuming the longer term down trend. Deeper decline is expected as long as 1.2666 resistance holds. Next target is 1.1409 low. However, firm break of 1.2666 will bring stronger rise back to 55 week EMA (now at 1.3175).

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PSI May | 55.2 | 51.4 | 52.2 | |

| 06:00 | EUR | Germany PPI M/M May | 1.50% | 2.80% | ||

| 06:00 | EUR | Germany PPI Y/Y May | 33.50% | 33.50% |