NZD Dips after Poor Consumer Confidence, Markets Staying in Consolidations

The markets are rather mixed in Asian session today, engaging in mostly consolidative moves. New Zealand Dollar trades broadly lower following record low consumer confidence data. But Canadian and Australian Dollars are firmer on steady risk sentiment. Dollar is also weak together with Yen while European majors are mixed.

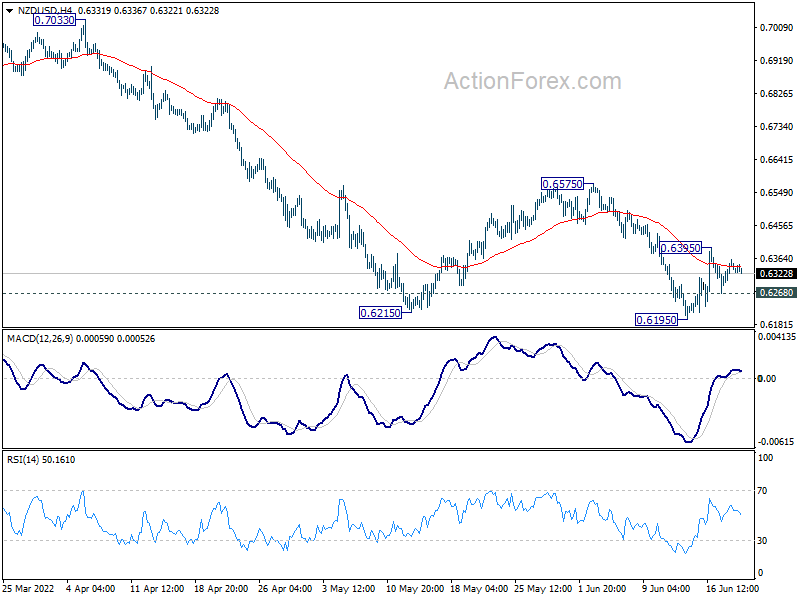

Technically, NZD/USD dips slightly after failing to stand above 4 hour 55 EMA again today. Overall development suggests that recovery from 0.6195 is merely a corrective move and outlook stays bearish. Break of 0.6286 minor support will likely resume larger down trend through 0.6195 low. Though, bring of 0.6395 will bring stronger rise back to 0.6575 structural resistance.

{kind=link}

In Asia, at the time of writing, Nikkei is up 2.37%. Hong Kong HSI is up 1.59%. China Shanghai SSE is down -0.12%. Singapore Strait Times is up 0.88%. 10-year JGB yield is down -0.0003 at 0.233.

ECB Lane: Initial policy normalization steps clear and robust

ECB Chief Economist Philip Lane said yesterday, “we have very high inflation rates now, and clearly we could be in a world where inflation psychology is taking hold.”

In a presentation, he said that Eurozone is facing three inflation shocks: pandemic cycle, energy shock and Russia-Ukraine war. Risks to inflation outlook include catch-up adjustment in wages, re-set of long term inflation expectations, inflation psychology, downward revision in potential output, and rise in real interest rate.

He added that monetary policy normalization is “appropriate” with “clear and robust” initial steps. That is, ECB will be stopping asset purchases, raise interest rate by 25bps in July, and again in September. Though, the size of the September hike is undecided. As for further steps, they will be state-contingent (gradualism, optionality, flexibility, data-dependency).

RBA Lowe: Going to be some years before inflation back in target range

RBA Governor Philip Lowe said the larger than expected 50bps hike at last meeting was driven by “additional information suggesting a further upward revision to an already high inflation forecast”.

He also emphasized, “as we chart our way back to 2 per cent to 3 per cent inflation, Australians should be prepared for more interest rate increases.”

“In the next month or so, we’ll be doing a full forecast update, but it’s going to be some years, I think, before inflation is back in the 2-3 per cent range, he added.

“I don’t see a recession on the horizon,” Lowe said. “If the last two years has taught us anything, it’s that you can’t rule anything out. But our fundamentals are strong, the position of the household sector is strong, and firms are wanting to hire people at record rates. It doesn’t feel like a precursor to a recession,” he said.

New Zealand Westpac consumer confidence dropped to 78.7 in Q2, record low

New Zealand Westpac consumer confidence dropped sharply from 92.1 to 78.7 in Q2. That’s the lowest level on record, and well below long-term average at 110.2.

Westpac said: “The pressure on household finances and sharp fall in confidence reinforces our expectations for a downturn in household spending – and economic growth more generally – over the coming months”.

“The RBNZ’s own projections show the cash rate rising to 3.9%, while financial markets have started to price in the chance that it could go as high as 4.5%…

“If there is a more abrupt slowdown in spending than the RBNZ anticipates, then it’s likely that increases in the cash rate will be more measured.”

Japan PM Kishida and opposition Tamaki agree BoJ to keep loose monetary policy

Japan Prime Minister Fumio Kishida asked opposition DDP’s Yuichiro Tamaki on monetary policy. Tamaki said the BOJ must keep current ultra-low interest rates, arguing that tightening monetary policy was “unthinkable”. Kishida said afterwards, “I agree with you on the point that Japan shouldn’t alter monetary policy,”

Kishida also said, “monetary policy affects not just currency rates, but the economy and smaller firms’ businesses. Such factors must be taken into account comprehensively.”

Separately, Finance Minister Shunichi Suzuki said, “I’m concerned about the rapid yen weakening seen recently.” He added that the government will “closely liaise” with BoJ on watching the exchange markets with “even greater sense of urgency”.

“We will respond appropriately if necessary while keeping close communication with currency authorities from other countries,” Suzuki said.

Looking ahead

Swiss trade balance and Eurozone current account will be release in European session. Later in the day, Canada retail sales will take center stage. US will release existing home sales.

USD/JPY Daily Outlook

Daily Pivots: (S1) 134.62; (P) 135.03; (R1) 135.52; More…

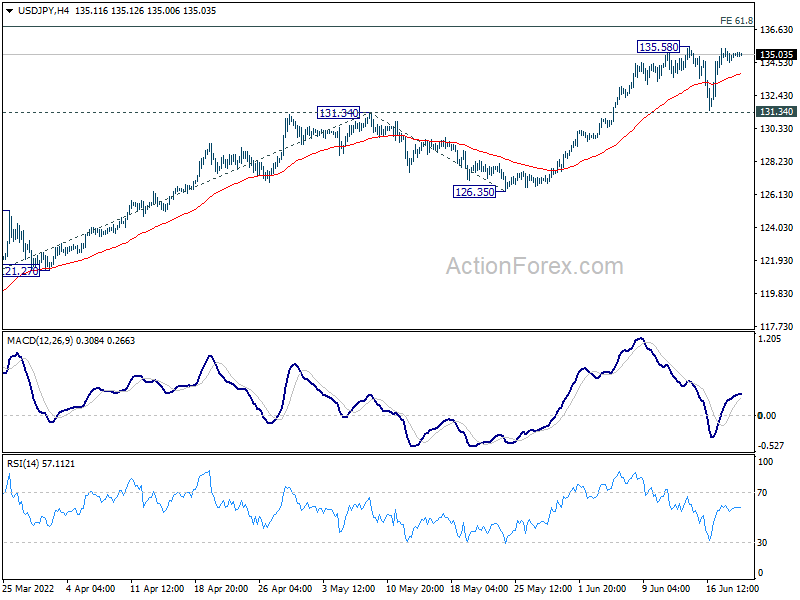

USD/JPY is still bounded in range below 135.58 and intraday bias remains neutral first. More consolidations could be seen but further rally is expected as long as 131.34 support holds. On the upside, break of 135.58 will resume larger up trend to 61.8% projection of 114.40 to 131.34 from 126.35 at 136.81. Firm break there will target 100% projection at 143.29.

{kind=link}

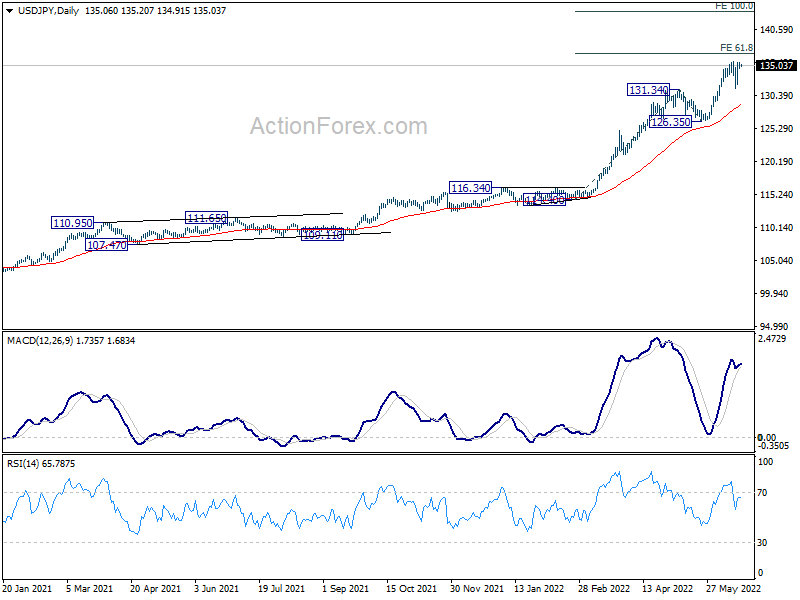

In the bigger picture, current rally is seen as part of the long term up trend from 75.56 (2011 low). Next target is 100% projection of 75.56 (2011 low) to 125.85 (2015 high) from 98.97 at 149.26, which is close to 147.68 (1998 high). This will remain the favored case as long as 126.35 support holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:00 | NZD | Westpac Consumer Survey Q2 | 78.7 | 92.1 | ||

| 01:30 | AUD | RBA Meeting Minutes | ||||

| 06:00 | CHF | Trade Balance (CHF) May | 3.78B | 4.13B | ||

| 08:00 | EUR | Eurozone Current Account Apr | -3.2B | -1.6B | ||

| 12:30 | CAD | New Housing Price Index M/M May | 0.40% | 0.30% | ||

| 12:30 | CAD | Retail Sales M/M Apr | 0.80% | 0.00% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M Apr | 0.50% | 2.40% | ||

| 14:00 | USD | Existing Home Sales May | 5.41M | 5.61M |