Slow Start to a Week with RBA Hike, Fed and ECB Minutes, NFP

It’s a rather slow start to the week, with major pairs and crosses stuck inside Friday’s range. Trading could remain subdued for the day with the US on holiday. But there are lots of events to look forward to, starting from RBA’s rate hike tomorrow. Minutes of Fed and ECB meeting might not reveal anything new. Instead, important data like ISM services and non-farm payroll would provide more guidance to the markets.

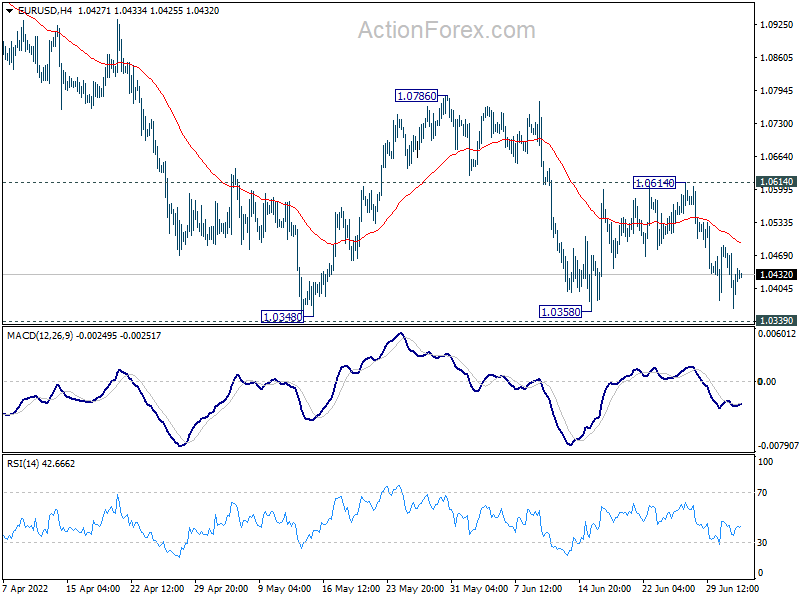

Technically, Dollar is in upper hand against both Euro and Sterling. Yet, both EUR/USD and GBP/USD are still held above recent lows at 1.0358 and 1.1932 respectively. These two levels will be the main focuses for the week as the US publishes important economic data.

In Asia, at the time of writing, Nikkei is up 0.68%. Hong Kong HSI is flat. China Shanghai SSE is up 0.35%. Singapore Strait Times is up 0.74%. Japan 10-year JGB yield is flat at 0.221.

Australia expects resource and energy export earnings to make successive records this year and next

Australia’s Department of Industry, Science and Resources said in a new quarterly report that resources and energy exports earnings are expected deliver two successive record years in 2021-2022 and 2022-2023, before falling slightly in 2023-24 to a third highest ever figure.

Resources and energy export earnings are estimated to be at AUD 405B in 2021-22, AUD 419B in 2022-23, and then notably lower at AUD 338B in 2023-24. The growth was mainly driven by higher prices as volume would remain below 2019-20 high throughout the forecast period.

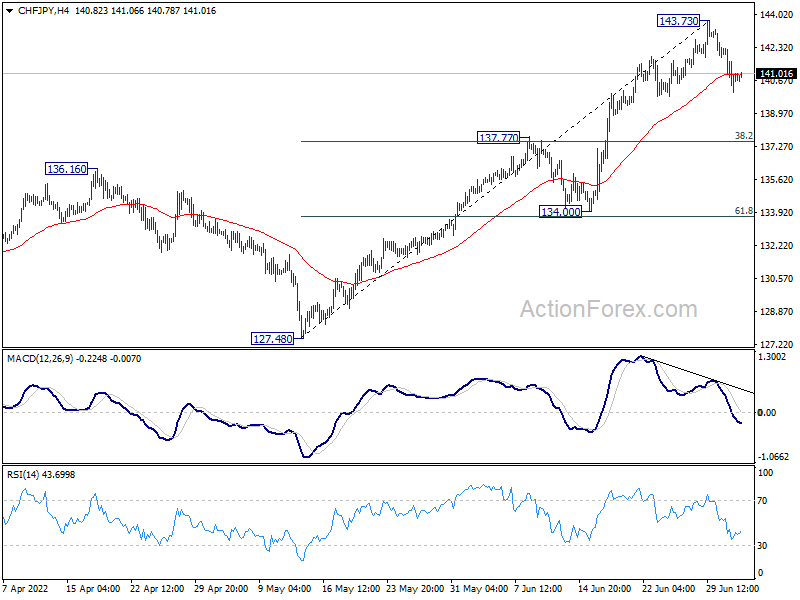

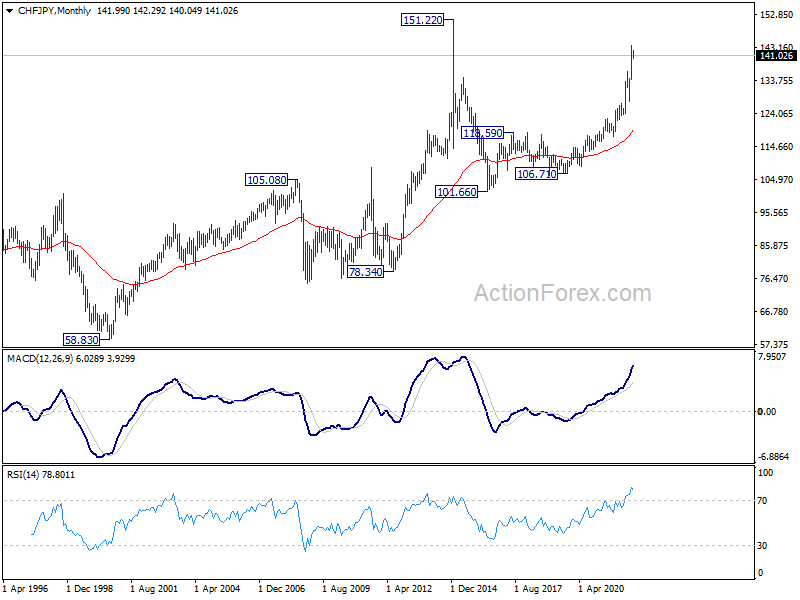

CHF/JPY topped in short term, but up trend intact

CHF/JPY’s up trend should have passed its climax for the near term. It has been lifted by buying in Swiss Franc on SNB’s hawkish rate hike in June, while BoJ is still standing firm by its ultra loose monetary policy. But recent pull back in benchmark treasury yields is giving Yen a lift. Meanwhile, as for the Franc, the pull back could be deeper if EUR/CHF manages to rebound firmly from 0.9970 long term support.

Technically, a short term top should be in place at 143.74, on bearish divergence condition in 4 hour MACD. Deeper correction cannot be ruled out for now. But downside should be contained by 137.77 cluster support (38.2% retracement of 127.48 to 143.73 at 137.52) to bring rebound. The overall long term up trend in CHF/JPY is still in healthy shape to retest 151.22 high (2014 high, the spike after SNB removed the EUR/CHF floor).

{kind=link}

{kind=link}

RBA to hike 50bps, Fed and ECB to publish minutes, NFP featured too

RBA is widely expected to raise interest rate by 50bps to 1.35% this week. A 75 bps was ruled out by Governor Philip Lowe, as he said only the 25bps and 50bps options were on the table. The central bank should also maintain tightening bias, setting the stage for more rate hikes down the road. Lowe has indicated in an interview that it’s reasonably to get the cash rate to 2.50% at some point. Nevertheless, the path would be data dependent. Fed and ECB will publish meeting minutes too.

The economic data calendar is also very busy. US ISM services and non-farm payroll report are the main focuses. But attention will also be on Eurozone Sentix, China PMI services, Swiss CPI, and Canada employment.

Here are some highlights for the week:

- Monday: Japan monetary base; Australia MI inflation gauge, building approvals; Germany trade balance; Swiss CPI; Eurozone Sentix investor confidence, PPI; Canada PMI manufacturing, BoC business outlook survey.

- Tuesday: Australia AiG construction, retail sales, RBA rate decision; China Caixin PMI services; France industrial production, Eurozone PMI services final; UK PMI services final; Canada building permits; US factory orders.

- Wednesday: Germany factory orders; UK PMI construction; Eurozone retail sales; US ISM services, FOMC minutes.

- Thursday: Australia AiG services, trade balance; Japan leading indicators; Swiss unemployment rate, foreign currency reserves; Germany industrial production; ECB meeting accounts; US ADP employment, jobless claims, trade balance; Canada trade balance, Ivey PMI.

- Friday: Japan household spending, current account; France trade balance; Italy industrial production; Canada employment; US non-farm payrolls.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0366; (P) 1.0428 (R1) 1.0489; More…

EUR/USD is still holding in range above 1.0339/58 support zone and intraday bias remains neutral first. Further decline is expected as long as 1.0614 resistance holds. On the downside, sustained break of 1.0339/48 will resume larger down trend. Next target is long term projection level at 1.0090. On the upside, above 1.0614 will turn bias back to the upside for 1.0786 resistance instead.

{kind=link}

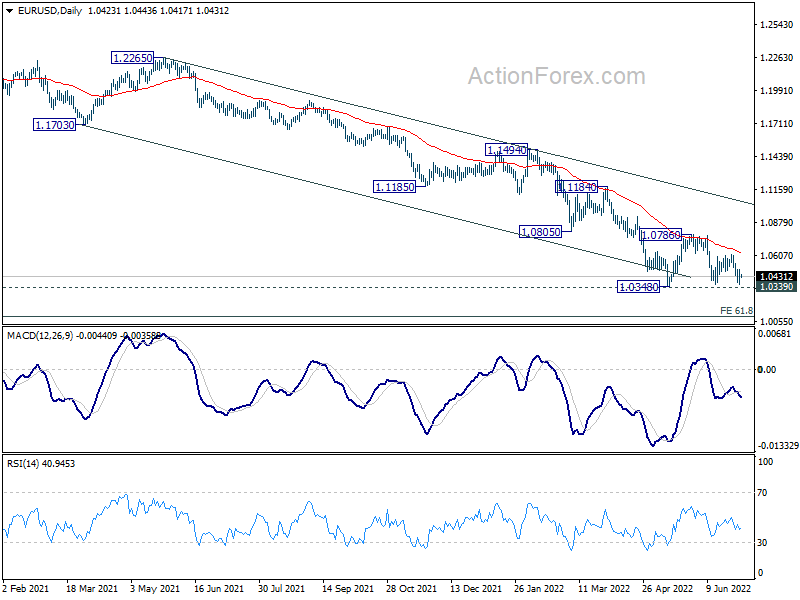

In the bigger picture, focus stays on 1.0339 long term support (2017 low). Decisive break there will resume whole down trend from 1.6039 (2008 high). Next target is 61.8% projection of 1.3993 to 1.0339 from 1.2348 at 1.0090. However, firm break of 1.0805 support turned resistance will delay this bearish case, and bring stronger rebound first.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Monetary Base Y/Y Jun | 3.90% | 4.90% | 4.60% | |

| 01:00 | AUD | TD Securities Inflation M/M Jun | 0.30% | 1.10% | ||

| 01:30 | AUD | Building Permits M/M May | 9.90% | -1.80% | -2.40% | -3.90% |

| 06:00 | EUR | Germany Trade Balance (EUR) May | 4.2B | 3.5B | ||

| 06:30 | CHF | CPI M/M Jun | 0.30% | 0.70% | ||

| 06:30 | CHF | CPI Y/Y Jun | 3.20% | 2.90% | ||

| 08:30 | EUR | Eurozone Sentix Investor Confidence Jul | -20 | -15.8 | ||

| 09:00 | EUR | PPI M/M May | 1.00% | 1.20% | ||

| 09:00 | EUR | PPI Y/Y May | 36.70% | 37.20% | ||

| 13:30 | CAD | Manufacturing PMI Jun | 56.8 | |||

| 14:30 | CAD | BoC Business Outlook Survey |