Yen Extending Rebound on Intervention Threat, Dollar Turned Mixed

Yen is shrugging off rally in US and European benchmark yields today, and rebound on threat of intervention in Japan. European majors are also finding some foots while Dollar turned mixed. Still commodity currencies are under broad based selling pressure. While US futures might point to a flat open, selling could come back later in the session. Overall, for the week, Dollar is so far the strongest, followed by Swiss Franc and Yen, and Kiwi is worst followed by Aussie and then Loonie.

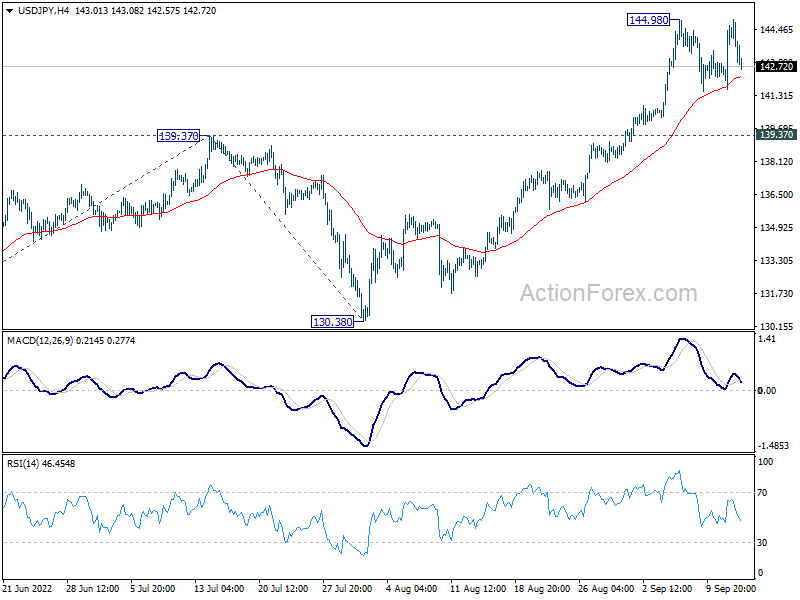

Technically, a focus now is on how far Yen’s rebound could go. As long as 139.37 resistance turned support in USD/JPY holds, it’s too early to call for bearish reversal. The pair is still more likely to resume recent up trend then not. Such development would also provide a floor to the selloff in other Yen crosses.

{kind=link}

In Europe, at the time of writing, FTSE is down -1.29%. DAX is down -1.1%. CAC is down -0.58%. Germany 10-year yield is up 0.012 at 1.744. Earlier in Asia, Nikkei dropped -2.78%. Hong Kong HSI dropped -2.48%. China Shanghai SSE dropped -0.37%. Singapore Strait Times dropped -0.97%. Japan 10-year JGB yield rose 0.0128 to 0.258.

US PPI down -0.1% mom, up 8.9% yoy in Aug

US PPI for final demand dropped -0.1% mom in August, matched expectations. The decreased is attributable to a -1.2% mom decline in prices for goods, while prices for services rose 0.4% mom. For the 12 months ended in August, PPI slowed from 9.8% yoy to 8.7% yoy, below expectation of 8.9% yoy. PPI for final demand less foods, energy and trade services rose 0.2% mom, 5.6% yoy.

From Canada, manufacturing sales dropped -0.9% mom in July, versus expectation of -1.0% yoy.

Eurozone industrial production dropped -2.3% mom in Jul, EU down -1.6% mom

Eurozone industrial production dropped -2.3% mom in July, much worse than expectation of -0.8% mom. Production of capital goods fell by -4.2%, durable consumer goods by -1.6% and intermediate goods by -0.8%, while production of energy rose by 0.4% and non-durable consumer goods by 1.2%.

EU industrial production declined -1.6% mom. Among Member States for which data are available, the largest monthly decreases were registered in Ireland (-18.9%), Estonia (-7.4%) and Austria (-3.2%). The highest increases were observed in Lithuania (+6.5%), Sweden (+5.8%) and Malta (+4.2%).

UK CPI slowed to 9.9% yoy in Aug, core CPI ticked up to 6.3% yoy

UK CPI slowed from 10.1% yoy to 9.9% yoy in August, below expectation of 10.2% yoy. CPI core rose from 6.2% yoy to 6.3% yoy, matched expectations. The largest contributions to the annual rate in August are from housing and household services, transport, and food and non-alcoholic beverages. July’s figure was the highest since 1982 based on indicative model.

On monthly basis, CPI rose 0.5% mom, slowed from prior 0.6% mom. Food and non-alcoholic beverages made the largest upward contribution to the monthly rates, while falling prices for motor fuels resulted in a large offsetting downward contribution.

Also released, RPI came in at 0.6% mom, 12.3% yoy, below expectation of 0.7% mom, 12.4% yoy. PPI input was at -1.2% mom, 20.5% yoy, versus expectation of 1.2% mom, 21.0% yoy. PPI output was at -0.1% mom, 116.1% yoy, versus expectation of 1.6% mom, 17.8% yoy. PPI core output was at 0.3% mom, 13.7% yoy, versus expectation of 1.5% yoy.

Japan officials toughen up talks on Yen

Top Japanese officials toughened up the talks on Yen, as it tumbled notably again overnight following US CPI data. Finance Minister Shunichi Suzuki said Japan wouldn’t rule out any response if current trends in the foreign exchange market continued, with intervention as an option.

The comment was echoed by top current diplomat Masato Kanda, who reiterated, “we are monitoring yen moves with a sense of urgency. We will respond appropriately to currency moves without ruling out any options.”

Chief Cabinet Secretary Hirokazu Matsuno also said at a briefing that the government would take necessary action should excessive yen moves continue. He added that rapid currency moves were undesirable.

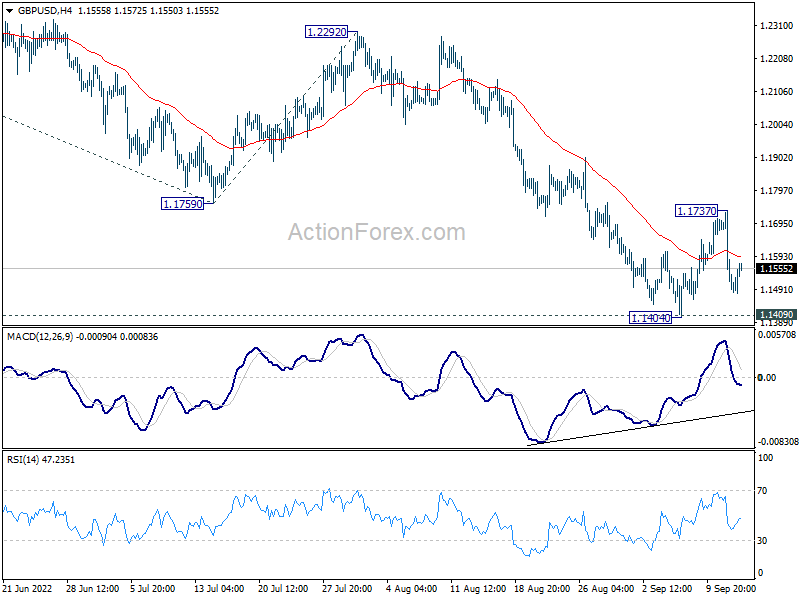

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1411; (P) 1.1574; (R1) 1.1657; More…

GBP/USD recovered well ahead of 1.1404/9 support zone and intraday bias is turned neutral first. On the downside, decisive break of 1.1404/9 will resume larger down trend. Next target is 61.8% projection of 1.3748 to 1.1759 from 1.2292 at 1.1063. On the upside, above 1.1737 minor resistance will resume the rebound from 1.1404 to 55 day EMA (now at 1.1917).

{kind=link}

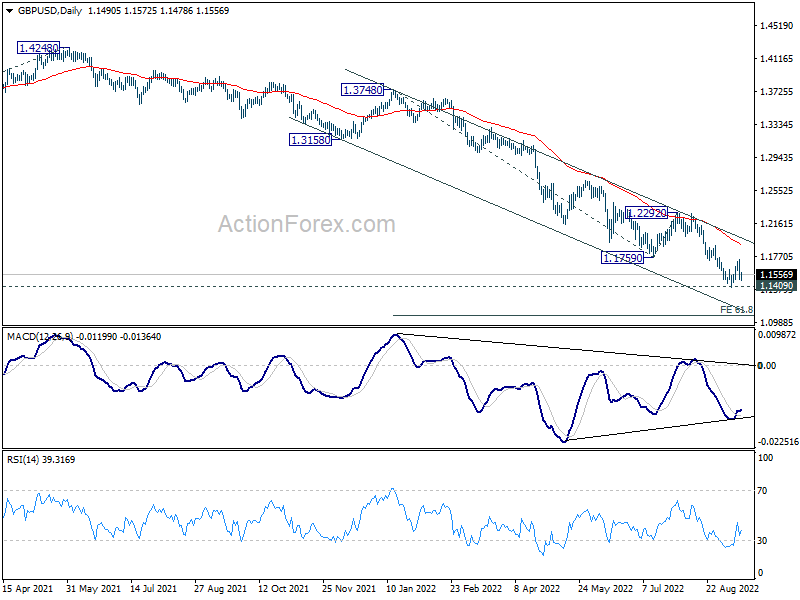

In the bigger picture, based on current momentum, fall from 1.4248 (2018 high) is probably resuming long term down trend from 2.1161 (2007 high). Sustained break of 1.1409 will target 61.8% projection of 1.7190 (2014 high) to 1.1409 (2020 low) from 1.4248 (2021 high) at 1.0675. This will remain the favored case for now as long as 1.2292 resistance holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Current Account (NZD) Q2 | -5.22B | -4.70B | -6.14B | -6.50B |

| 23:50 | JPY | Machinery Orders M/M Jul | 5.30% | -0.60% | 0.90% | |

| 04:30 | JPY | Industrial Production M/M Jul F | 0.80% | 1.00% | 1.00% | |

| 06:00 | GBP | CPI M/M Aug | 0.50% | 0.60% | 0.60% | |

| 06:00 | GBP | CPI Y/Y Aug | 9.90% | 10.20% | 10.10% | |

| 06:00 | GBP | Core CPI Y/Y Aug | 6.30% | 6.30% | 6.20% | |

| 06:00 | GBP | RPI M/M Aug | 0.60% | 0.70% | 0.90% | |

| 06:00 | GBP | RPI Y/Y Aug | 12.30% | 12.40% | 12.30% | |

| 06:00 | GBP | PPI Input M/M Aug | -1.20% | 1.20% | 0.10% | 0.00% |

| 06:00 | GBP | PPI Input Y/Y Aug | 20.50% | 21.00% | 22.60% | |

| 06:00 | GBP | PPI Output M/M Aug | -0.10% | 1.60% | 1.60% | 1.60% |

| 06:00 | GBP | PPI Output Y/Y Aug | 16.10% | 17.80% | 17.10% | |

| 06:00 | GBP | PPI Core Output M/M Aug | 0.30% | 1.50% | 1.00% | 0.80% |

| 06:00 | GBP | PPI Core Output Y/Y Aug | 13.70% | 13.90% | 14.60% | 14.40% |

| 09:00 | EUR | Eurozone Industrial Production M/M Jul | -2.30% | -0.80% | 0.70% | 1.10% |

| 12:30 | USD | PPI M/M Aug | -0.10% | -0.10% | -0.50% | -0.40% |

| 12:30 | USD | PPI Y/Y Aug | 8.70% | 8.90% | 9.80% | |

| 12:30 | USD | PPI Core M/M Aug | 0.40% | 0.30% | 0.20% | 0.30% |

| 12:30 | USD | PPI Core Y/Y Aug | 7.30% | 7.40% | 7.60% | 7.70% |

| 12:30 | CAD | Manufacturing Sales M/M Jul | -0.90% | -1.00% | -0.80% | -0.10% |

| 14:30 | USD | Crude Oil Inventories | 1.9M | 8.8M |