USD/JPY Closing in 150 as Traders Pricing in Two More 75bps Fed Hike This Year – Action Forex

There were so many important headlines last week. USD/JPY surged to new 32-year high with support from stronger than expected CPI, and as 10-year yield broke 4% handle. Japan maintained their stance that they will act resolutely on market volatility, without actual intervention. DOW staged a historic 1500pts U-turn on Thursday but gave up much gains just the following day. Sterling rebounded further as the UK delivered episodes of political chaos.

In the end, the Pound was the biggest winner, but Dollar was not too far way. As noted below, markets are already pricing in two more 75bps Fed hikes in November and December. Euro was resiliently the third strongest. When Yen clearly struggled, it’s only the second worst next the Aussie, then followed by Swiss Franc.

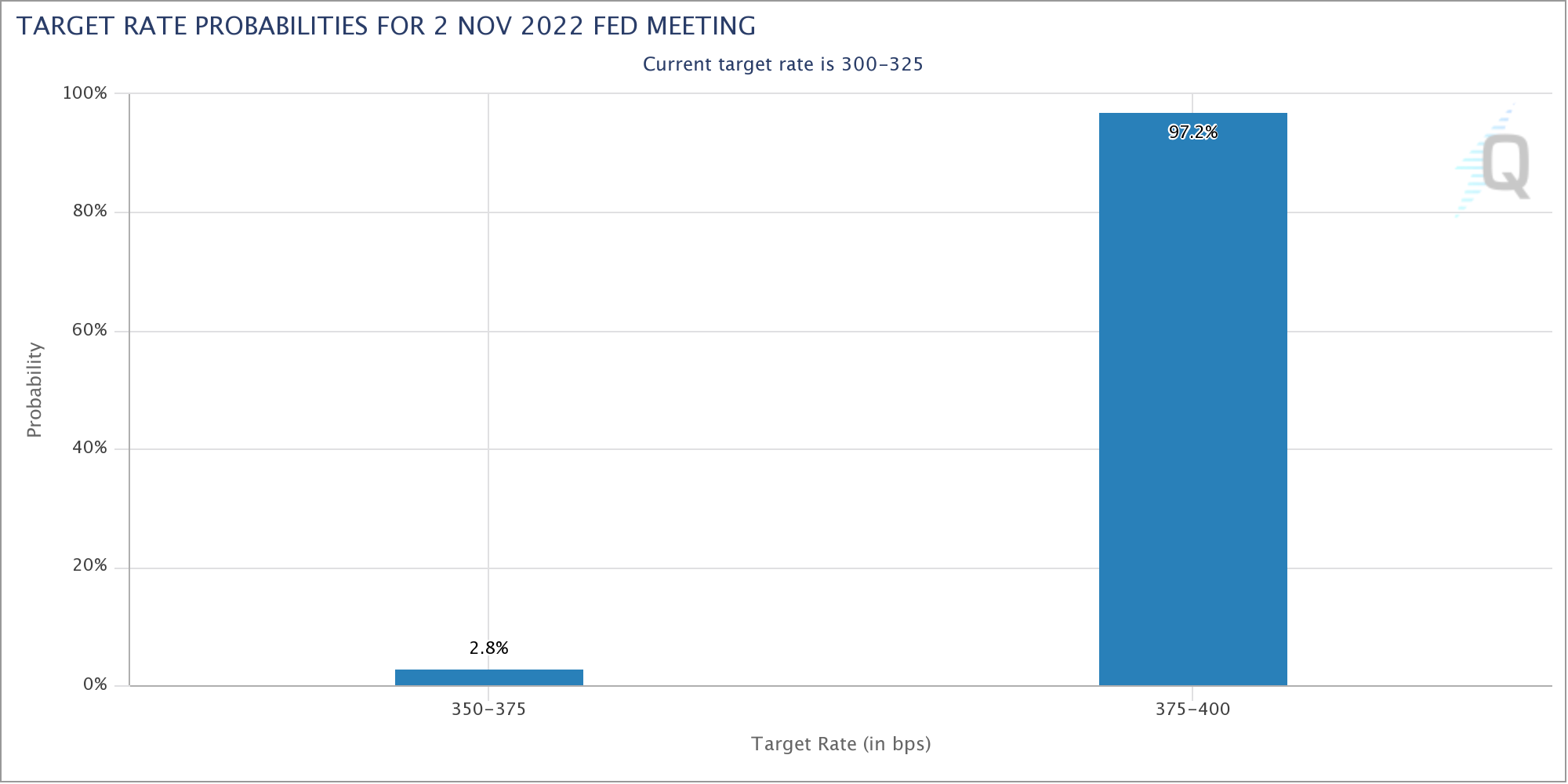

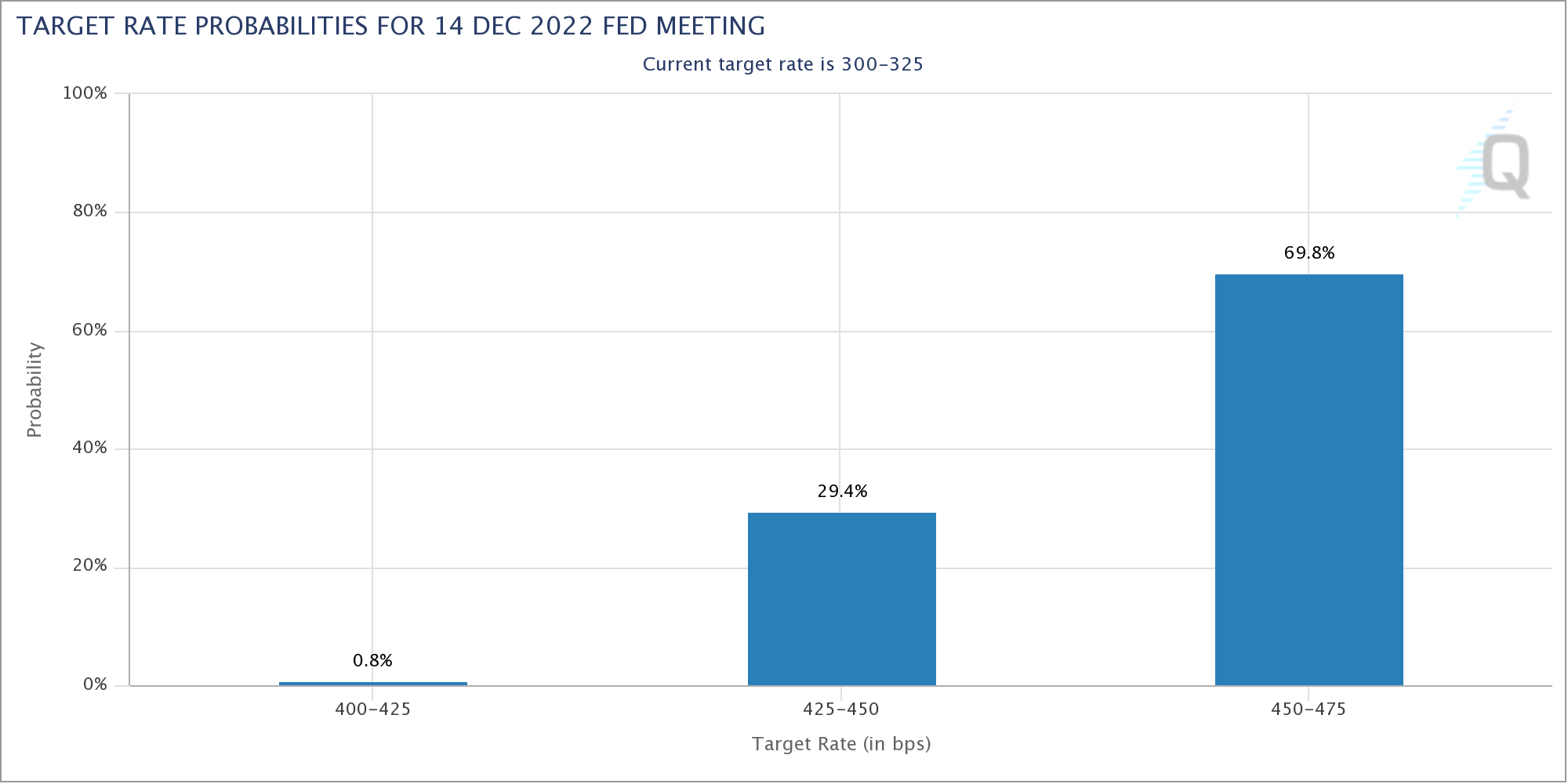

Markets pricing 97% chance of Nov 75bps hike, 70% of Dec 75bps hike

After stronger than expected CPI reading in the US, investors added their bets continuation of aggressive tightening by Fed ahead. Such expectations were affirmed by FOMC minutes which highlighted policymakers’ concern on persistent inflation, and the cost of doing too little. Fed fund futures are now pricing in 97.2% chance of 75bps hike to 3.75-4.00%.

{kind=link}

Indeed, there’s also nearly 70% chance of 75bps hike to 4.50-4.75% at December 14 meeting.

{kind=link}

DOW and NASDAQ staying bearish despite rebound attempts

US stocks staged a strong rebound on Thursday after CPI release, but reversed much gains on Friday. DOW was rejected by 30454.46 resistance, and the development keeps near term outlook bearish. That is, another decline should be seen sooner rather than later to 100% projection of 36965.83 to 29653.29 from 34281.36 at 26982.00

{kind=link}

NASDAQ’s recovery was even weaker, and kept below corresponding resistance at 11230.44. Next target is 61.8% projection of 16212.22 to 10565.13 from 13181.08 at 9691.17. Firm break there could prompt downside acceleration to 100% projection at 7633.99.

{kind=link}

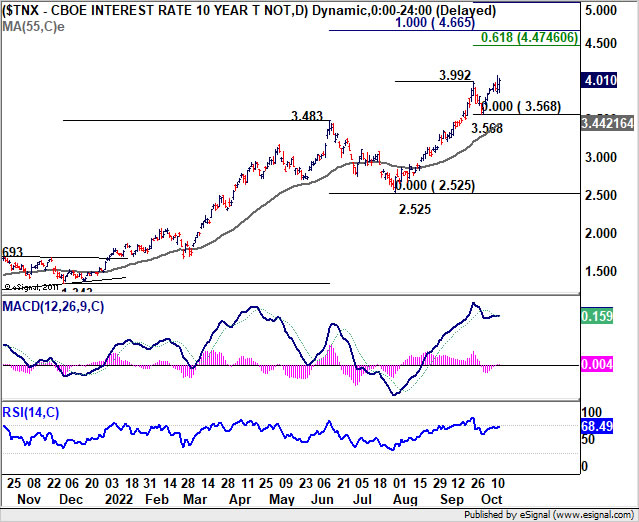

10-year yield extended up trend, closed above 4%

10-year yield’s up trend resumed last week and closed above 4% handle. Upside momentum is not too strong as seen in 4 hour MACD. But further rally is expected anyway. Sustained trading above 4.000 could prompt some upside reacceleration towards 61.8% projection of 2.525 to 3.992 from 3.568 at 4.474 next.

{kind=link}

Dollar index extended consolidation, staying bullish

Dollar index, however, remains bounded in range below 114.77 resistance last week. That’s mainly because Dollar failed to build up momentum against Euro. Still, outlook will stay bullish as long as 55 day EMA (now at 109.98) holds. Break of 114.77 will resume the up trend towards 100% projection of 94.62 to 109.29 from 104.63 at 119.30, which is close to 120 handle.

{kind=link}

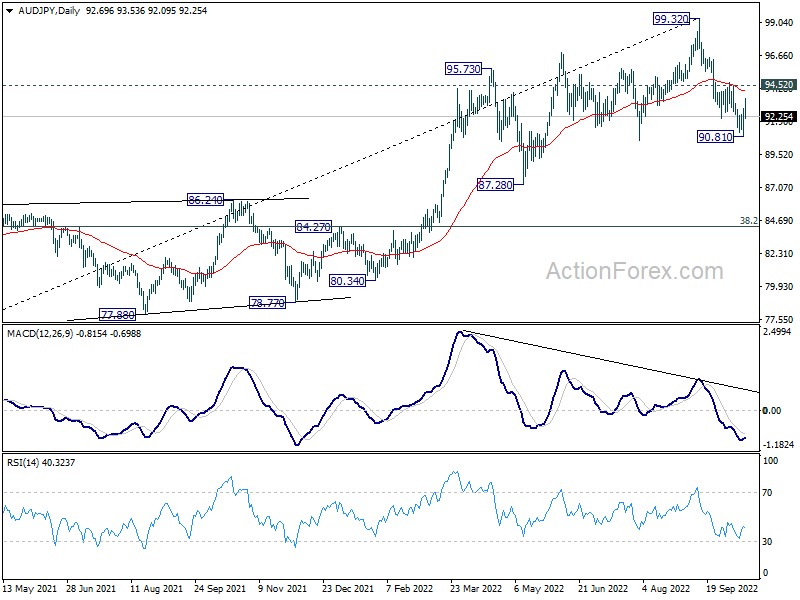

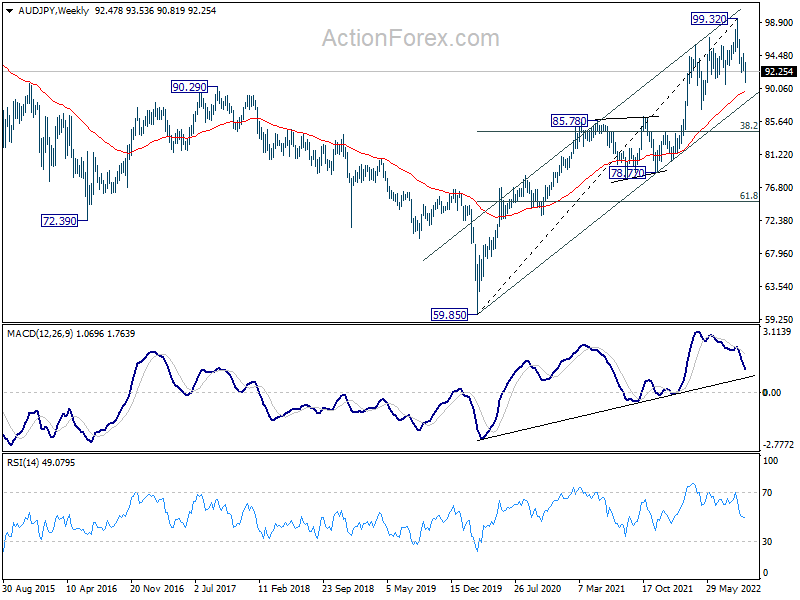

AUD/JPY maintains bearishness as Aussie underperforms the weak Yen

While Yen was clearly a big loser last week, Aussie was even worse. One factor is that RBA has started slowing down its tightening earlier this month, which others are maintaining the same pace. Another factor is the concern over extended slowdown in China’s economy due to its so-called zero-COVID policy, and intensifying tension with the West.

AUD/JPY’s recovery from 90.81 was kept well below 55 day EMA and 94.52 resistance, keeping near term outlook bearish. Considering bearish divergence condition in daily MACD, 99.32 should be a medium term top. Fall from there might either be correcting the up trend from 78.77, or even that from 59.85. In either case, deeper fall is likely to 55 week EMA (now at 89.61). Sustained break there will target 38.2% retracement of 59.85 to 99.32 at 84.24.

{kind=link}

{kind=link}

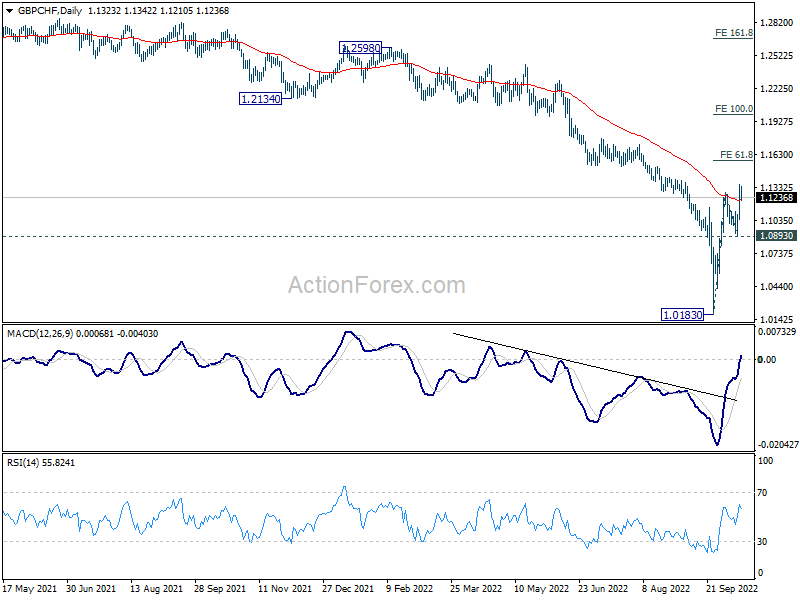

Sterling rebounds further, riding on political chaos

Sterling ended as the best performer, helped much by the political chaos in the UK. In the latest episode, UK Prime Minister Liz Truss sacked her Finance Minister Kwasi Kwarteng, and replaced him by former Foreign and Health Minister Jeremy Hunt. Hunt is now expected to deliver a new budget plan on October 31, which he already indicated that “some taxes will not be cut as quickly as people want, and some taxes will go up.”

As a side note, the development somewhat proves that BoE’s was right in not to panic and rush into emergency action, other than the targeted gilt stabilization operations. After all, the Brits know their country more than the others. It’s now way too soon to predict what BoE would do at the November meeting, at least not before Hunt’s budget, and BoE’s own revision on economic projections.

GBP/CHF extended the rebound from 1.0183 last week and the close above 55 day EMA is a positive sign. Further rally is now in favor as long as 1.0893 support holds. The key near term hurdle is 61.8% projection of 1.0183 to 1.1283 from 1.0893 at 1.1573. Sustained break there could prompt upside acceleration to 100% projection at 1.1993, which is above 55 week EMA.

{kind=link}

{kind=link}

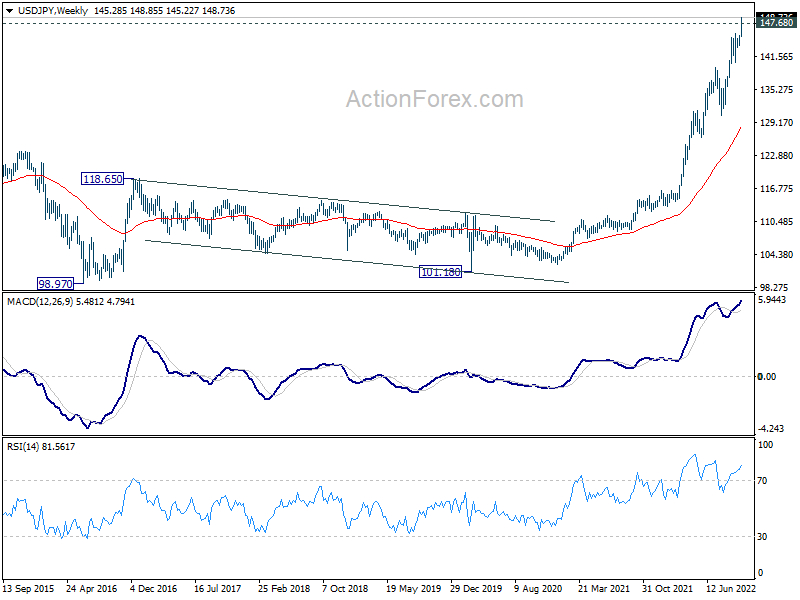

USD/JPY Weekly Outlook

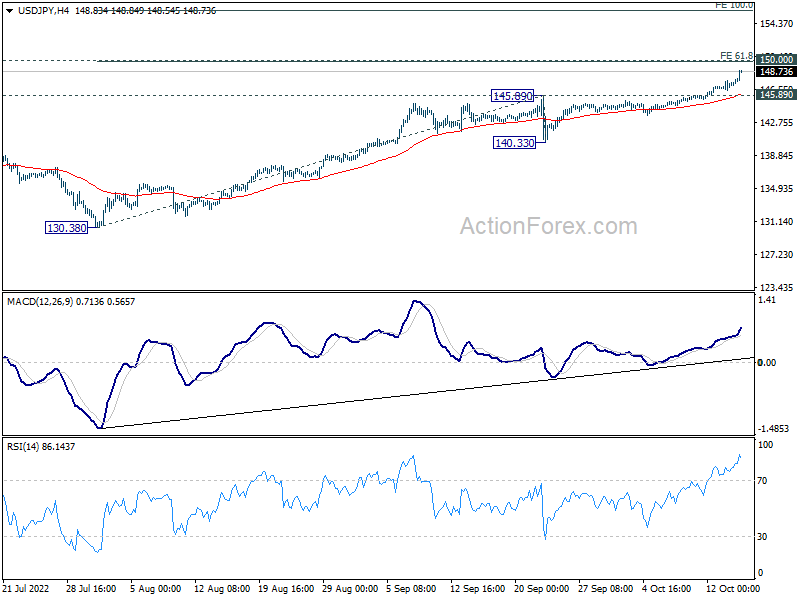

USD/JPY’s up trend resumed last week and reached high as high 148.85, breaking 147.68 long term resistance. There is no clear sign of topping yet. Initial bias stays on the upside this week for 61.8% projection of 130.38 to 140.33 from 145.89 at 149.91. Beware that Japan might intervene again there close to 150 psychological level. Nevertheless, break of 145.89 resistance turned support is needed to confirm short term topping. Otherwise, outlook will remain bullish in case of retreat.

{kind=link}

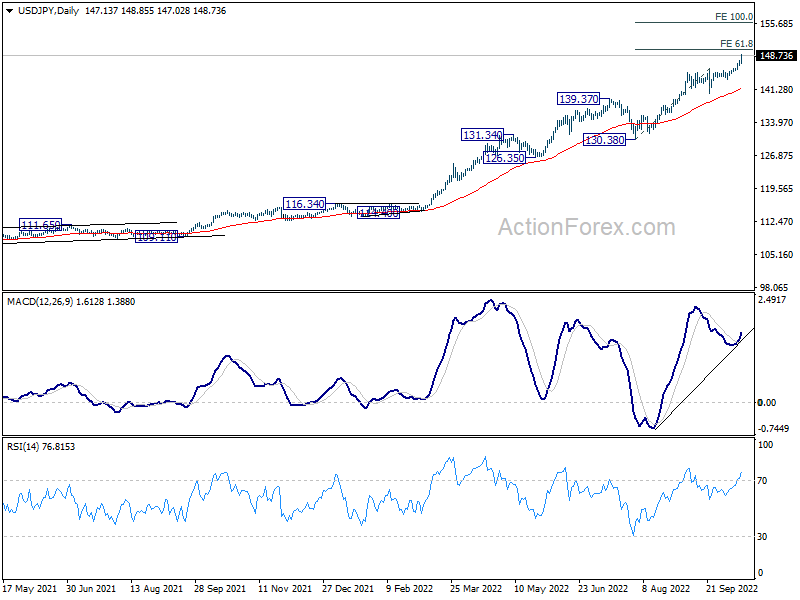

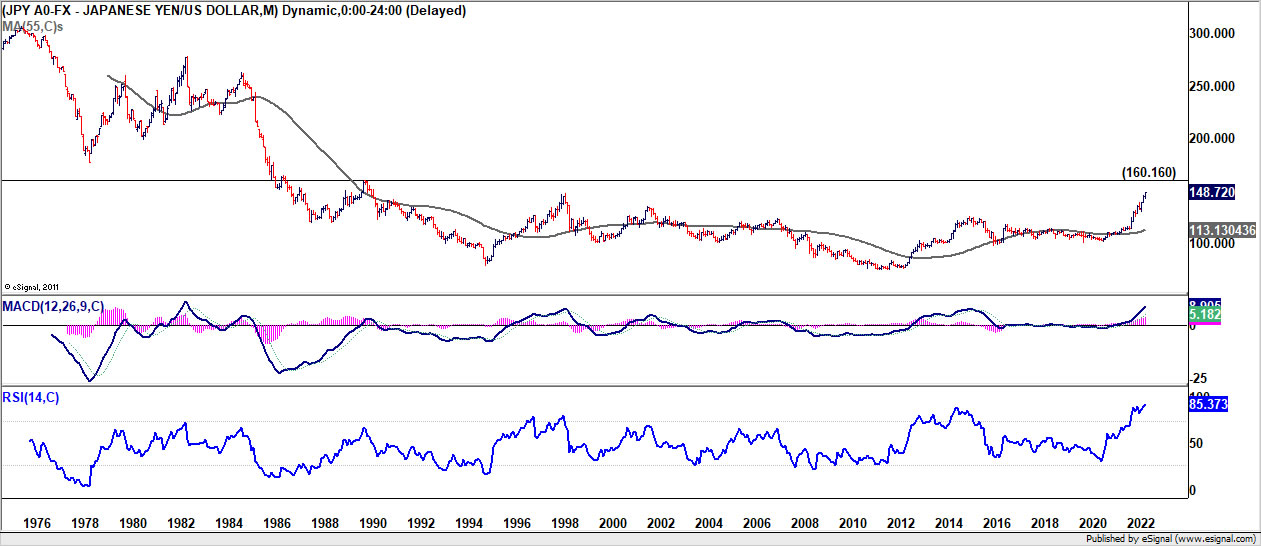

In the bigger picture, up trend from 101.18 is still in progress, as part of the whole up trend from 75.56 (2011 low). 147.68 (1998 high) was already met and there is not clearly sign of topping yet. In any case, break of 139.37 resistance turned support is needed to be the first sign of medium term topping. Otherwise, further rise is in favor to next target at 160.16 (1990 high).

{kind=link}

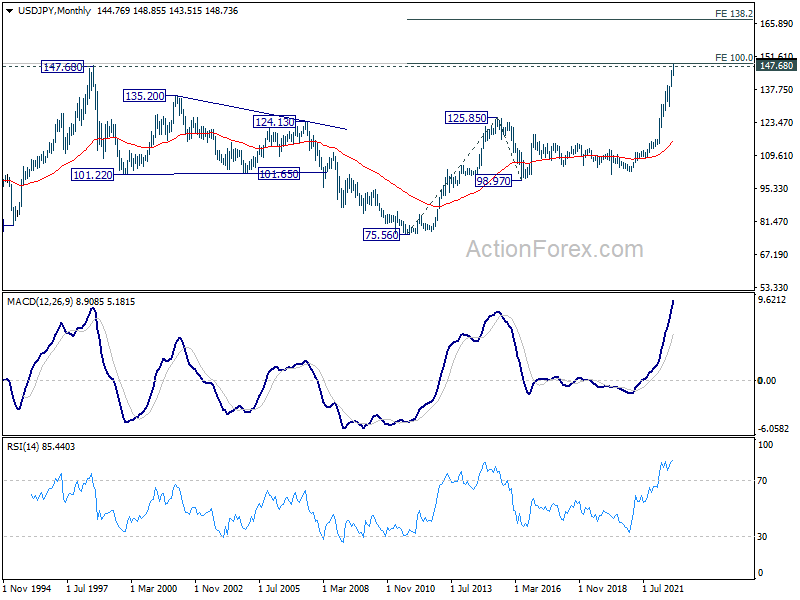

In the long term picture, rise from 101.18 is seen as part of the up trend from 75.56 (2011 low). Sustained break of 100% projection of 75.56 (2011 low) to 125.85 (2015 high) from 98.97 at 149.26, will pave the way to 138.2% projection at 168.47. This will remain the favored case as long as 130.38 support holds.

{kind=link}

{kind=link}

{kind=link}