Australian Dollar Rebounds Notably on Employment Data, Resurgence in Copper and Yuan – Action Forex

Australian Dollar is making a notable rebound today, largely supported by strong employment data, rebound in Copper price, and a resurgence in Chinese Yuan. In tandem, New Zealand Dollar is closely trailing the second strongest performer. British Pound languishes as the worst performer, still feeling the drag from yesterday’s lower-than-expected UK CPI Data. Dollar and Japanese Yen are also experiencing weakness, seemingly reacting to the extended rally in US stock markets overnight. Euro and Canadian Dollar display mixed performance at the moment.

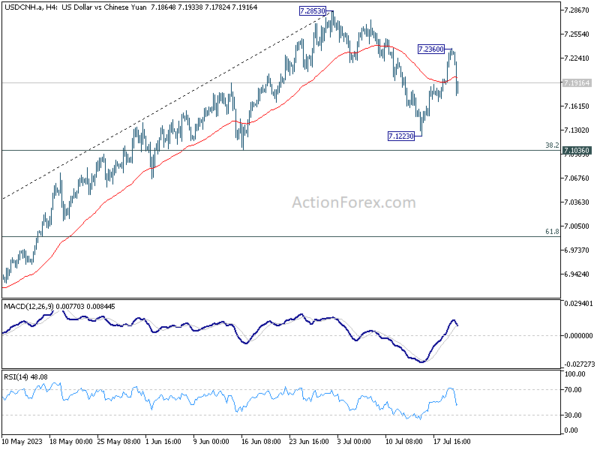

In an interesting development, People’s Bank of China announced an increase in a parameter on cross-border corporate financing under its macro-prudential assessments. This strategic move is aimed at enhancing cross-border financing and continuing to expand the sources of cross-border funds for businesses and financial institutions. Analysts interpret this step as a clear intention to maintain RMB above 7.2 handle.

USD/CNH pull backed sharply from 7.2360 today. But overall technically outlook is unchanged. Price actions from 7.2853 are seen as a corrective pattern for now. Strong support from 55 D EMA (now at 7.132) maintains near term bullishness. As long as 7.1036 cluster support holds (38.2% retracement of 6.810 to 7.2853 at 7.1037), another rise is still in favor through 7.2853 to 7.3745. If realized, resumed selloff in CNH would exert some pressure on Aussie again.

In Asia, Nikkei closed down -1.23%. Hong Kong HSI is down-0.06%. China Shanghai SSE is down -0.84%. Singapore Strait Times is up 0.02%. Japan 10-year JGB yield is down -0.0009 at 0.466. Overnight, DOW rose 0.31%. S&P 500 rose 0.24%. NASDAQ rose 0.03%. 10-year yield dropped -0.0047 to 3.742.

BoE Ramsden: CPI inflation remains much too high

BoE Deputy Governor Dave Ramsden said yesterday, “CPI inflation has begun to fall significantly but remains much too high. The Monetary Policy Committee has consistently stressed that monetary policy decisions will address the risk of more persistent strength in domestic wage and price settling.”

He went on to warn, “If there is evidence of more persistent pressures, then further tightening in monetary policy would be required.”

Ramsden also mentioned BoE’s efforts in reducing its holdings of gilts and corporate bonds, which he expects to decrease by a total of GBP 100B by October. However, he pointed out that the central bank has almost completely run off its portfolio of corporate debt, possibly paving way for it to sell more government bonds.

In light of these factors, Ramsden stated, “These factors support a carefully considered increase in the pace of reduction in the stock of gilts in the 12 months ahead.” However, he also stressed caution, noting, “I emphasize careful — like the MPC, I want Quantitative Tightening (QT) to set a gradual and predictable pace for unwind and to let it operate in the background, after all.”

Japan’s export to US up 11.7% yoy in Jun, to EU up 15%, to China down -11%

Japan’s exports rose by 1.5% yoy to JPY 8744B in June. The significant rise in exports to US by 11.7% yoy and to EU by 15.0% yoy was offset by the -11.0% yoy decline in exports to China (marking the most significant drop since January).

Rise in US-bound exports was primarily driven by shipments of cars and mining machinery. Meanwhile, dip in exports to China was attributed the decreased shipments of steel, chips, and nonferrous metal, which led to an overall double-digit decline.

Japan’s imports contracted by -12.9% yoy to JPY 8701B. The decrease in value of imports is primarily linked to drop in crude, coal, and liquefied natural gas.

As a result, Japan recorded a trade surplus of JPY 43B, the first such instance in nearly two years since July 2021.

In seasonally adjusted term, exports rose 3.3% mom to JPY 8269B. Imports rose 0.5% mom to JPY 8822B. Trade balance reported JPY -553B deficit, versus expectation of JPY -550B.

Australia employment grew 32.6k, but demand met by people working more hours

Australian’s June employment data showed persistent tightness in the job markets. The 32.6k growth in employment significantly surpassed expectations of 15.0k. Employment-population ratio remained at record high. Monthly hours worked outpaced employment growth, suggesting that labor demand was met by people working more hours.

Among the 32.6k job growth, rise of 39.3k full-time employment was offset by a decrease of -6.7k in part-time roles. Unemployment rate remained steady at 3.5%, below expectation of 3.6%. Participation rate dipped slightly from 66.9% to 66.8%. Monthly hours worked rose 0.3% mom, faster than growth in employment at 0.2% mom.

Bjorn Jarvis, ABS head of labour statistics, stated: “The rise in employment in June saw the employment-to-population ratio remain at a record high 64.5 per cent, reflecting a tight labour market in which employment has recently increased in line with population growth.”

He further emphasized that the current labour market is stronger than it was prior to the pandemic. Jarvis elaborated, “In addition to there being over a million more employed people than before the pandemic, a much higher share of the population is employed. In June 2023, 64.5 per cent of people 15 years or older were employed, an increase of 2.1 percentage points since March 2020.”

Jarvis also highlighted the ongoing demand for labour, saying: “The strength in hours worked since late 2022, relative to employment growth, shows the demand for labour is continuing to be met, to some extent, by people working more hours.”

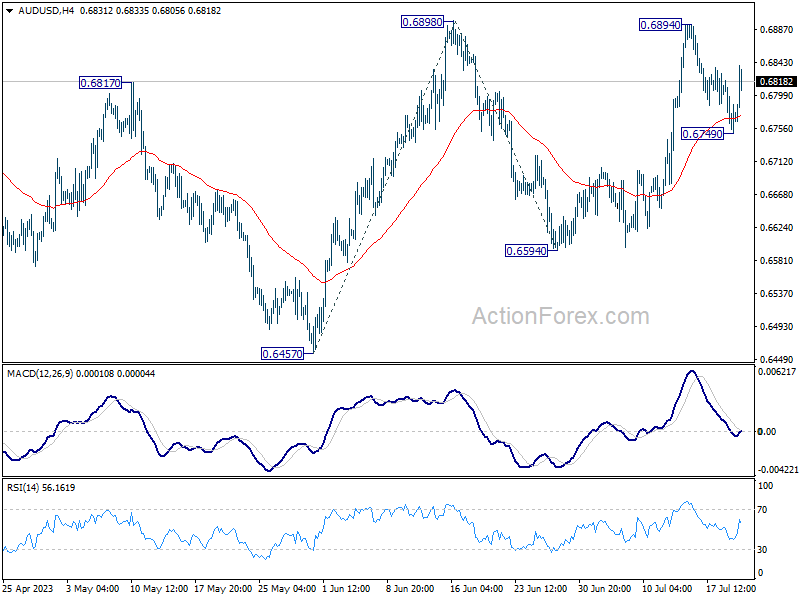

AUD/USD Daily Report

Daily Pivots: (S1) 0.6741; (P) 0.6780; (R1) 0.6811; More…

AUD/USD rebounds notably after drawing support from 55 4H EMA, but stays below 0.6894/8 resistance zone. Intraday bias remains neutral for the moment. On the upside, decisive break of 0.6898 resistance will firstly confirm resumption of rise from 0.6457. Secondly, that should also confirm completion of the fall from 0.7156 at 0.6457. Next target will be 100% projection of 0.6457 to 0.6898 from 0.6594 at 0.7035, and then 0.7156 resistance.

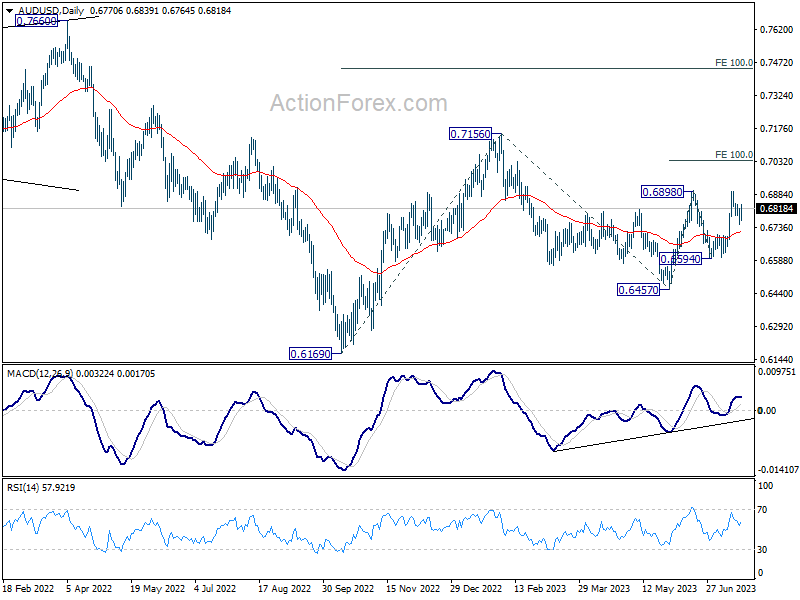

In the bigger picture, price actions from 0.7156 are seen as a correction to the rebound from 0.6169 (2022 low). Break of 0.6898 resistance will argue that rise from 0.6169 is ready to resume through 0.7156. Next target will be 100% projection of 0.6169 to 0.7156 from 0.6457 at 0.7444. For now, this will be the favored case as long as 55 D EMA (now at 0.6703) holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance (JPY) Jun | -0.55T | -0.66T | -0.78T | -0.77T |

| 01:30 | AUD | NAB Business Confidence Q2 | -3 | -4 | ||

| 01:30 | AUD | Employment Change Jun | 32.6K | 15.0K | 75.9K | 76.5K |

| 01:30 | AUD | Unemployment Rate Jun | 3.50% | 3.60% | 3.60% | 3.50% |

| 06:00 | CHF | Trade Balance (CHF) Jun | 4.82B | 4.23B | 5.48B | |

| 06:00 | EUR | Germany PPI M/M Jun | -0.30% | -0.40% | -1.40% | |

| 06:00 | EUR | Germany PPI Y/Y Jun | 0.10% | 0.00% | 1.00% | |

| 08:00 | EUR | Eurozone Current Account (EUR) May | 2.5B | 3.6B | ||

| 12:30 | USD | Initial Jobless Claims (Jul 14) | 245K | 237K | ||

| 12:30 | USD | Philadelphia Fed Manufacturing Jul | -15.5 | -13.7 | ||

| 14:00 | USD | Existing Home Sales Jun | 4.27M | 4.30M | ||

| 14:00 | EUR | Eurozone Consumer Confidence Jul P | -16 | -16 | ||

| 14:30 | USD | Natural Gas Storage | 45B | 49B |