Swiss Franc Tumbles on SNB Cut; Sterling Falters as Hawks Retreat – Action Forex

Swiss Franc is trading as the day’s most significant loser in the wake of SNB’s surprising decision to cut interest rates. This move, along with a substantial downward revision of inflation forecasts, is seen by some economists as a strategic effort by SNB to alleviate the burden of a high exchange rate on Switzerland’s export-driven economy. Speculation is rife among economists about the possibility of another rate reduction in June, particularly if ECB commences its policy easing by then.

British Pound also faced downward pressure as the second worst performer, following BoE decision to maintain its interest rate unchanged. Notably, two previously hawkish members abandoned their stance on calling for a hike. Yet BoE provided no definitive guidance on rate reductions. Despite some progress in reducing inflation, service sector prices continue to be a concern, remaining stubbornly high.

The Australian Dollar stands out as the day’s strongest currency, buoyed by impressive employment data and PMI improvements, hinting at less likelihood of an immediate RBA rate cut. Meanwhile, Yen is making a modest recovery from its sharp post-BoJ losses earlier in the week, and Dollar is regaining some ground lost to yesterday’s risk-on sentiment. Euro and Canadian Dollar held their ground in the market’s middle tier.

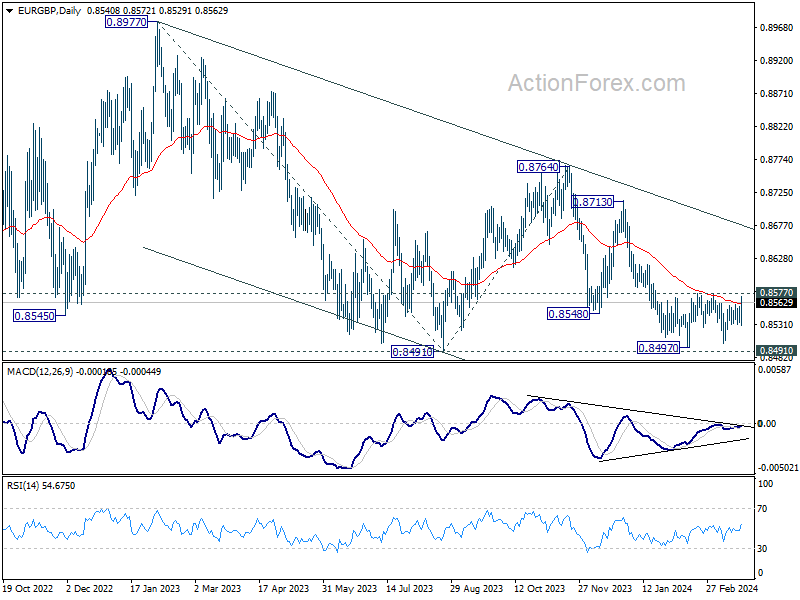

Technically, one focus now is whether EUR/GBP could ride on the currency wave of Sterling selloff. Firm break of 0.8577 resistance will be an indication of near term bullish reversal, and target medium term trend line resistance at around 0.8670.

In Europe, at the time of writing, FTSE is up 1.58%. DAX is up 0.39%. CAC is up 0.01%. UK 10-year yield is down -0.0468 at 4.078. Germany 10-year yield is down -0.027 at 2.410. Earlier in Asia, Nikkei rose 2.03% to new record. Hong Kong HSI rose 1.93%. China Shanghai SSE fell -0.08%. Singapore Strait Times rose 1.35%. Japan 10-year JGB yield rose 0.0086 to 0.740.

BoE maintains status quo as hawks relinquish rate hike demands

BoE maintained the Bank Rate at 5.25% as widely expected. The decision was made by an 8-1 vote, with Swati Dhingra singularly advocating for a reduction again. Notably, previous hawks Jonathan Haskel and Catherine Mann adjusted their positions, refraining from advocating for hikes this round.

BoE noted that February’s CPI inflation rate of 3.4% was marginally lower than forecasted in the the latest Monetary Policy Report. Despite a decline in services consumer price inflation, it remains significantly high. Nevertheless, most measures of short-term inflation expectations are on a downtrend.

With the government’s decision to freeze fuel duty, CPI is projected to dip slightly below 2% mark in the second quarter. However, a slight uptick is anticipated in the latter half of the year.

UK PMI manufacturing hits 20-month high, services ease slightly

UK PMI Manufacturing rose from 47.5 to 49.9 in March, above expectation of 47.9, a 20-month high. PMI Services fell slightly from 53.8 to 53.4, below expectation of 53.8. PMI Composite ticked down from 53.0 to 52.9.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, interprets the data as evidence of UK’s recovery from the recession in the latter half of 2023. The aggregate business activity for Q1 suggests 0.25% GDP growth, marking the best quarter since mid-last year

Despite the optimistic growth indicators, inflation remains a pressing issue, particularly in the services sector, where “stubbornly sticky” inflation pressures continue. Moreover, the manufacturing sector saw “renewed inflation”.

While the overall inflation rate is expected to decline in the coming months, March’s PMI data point to “elevated underlying price pressures,” possibly influencing BoE to exercise caution. Williamson, suggests that a decisive shift towards lower interest rates should only occur once there is clear evidence of moderating wage growth.

SNB cuts interest rate, sharply slashes inflation forecasts

In a surprising move, SNB announced a -25bps cut in its policy rate, bringing it down to 1.50%. This decision also introduced a tiered system for the remuneration of banks’ sight deposits held at SNB. Deposits up to a specified threshold will earn interest at the policy rate, while those exceeding this limit will attract only 1.0% higher rate. Furthermore, SNB affirmed its readiness to intervene in the foreign exchange market if deemed necessary.

The rationale behind the rate cut, as outlined by the SNB, is the “effective” management of inflation over the past two and a half years, which has allowed inflation rates to settle below the 2% mark for several months. This achievement aligns with the SNB’s definition of price stability and sets the stage for a conducive economic environment in the foreseeable future.

The new conditional inflation forecasts are revised sharply lower even with a lower policy rate. SNB project a modest increase in inflation from 1.2% in Q1 to 1.5% in Q2 of this year, followed by a decline to 1.2% in Q1 2025, and a further decrease to 1.1% in the second half of 2026.

Eurozone PMI composite ticks up to 49.9, price development not enough to alter ECB’s course

Eurozone PMI Manufacturing from 46.5 to 45.7 in March, below expectation of 47.0. PMI services, on the other hand rose from 50.2 to 51.5, above expectation of 50.5 a 9-month high. PMI Composite ticked up from 49.2 to 49.9, also a 9-month high.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, highlighted the “clear weakness” in manufacturing, attributing it largely to Germany’s industrial performance. On a brighter note, the further expansion in the services PMI is considered a “positive development.”

From a monetary policy perspective, ECB may find some solace in the report’s implications on inflationary pressures. Notably, the services sector, which is typically sensitive to wage dynamics, has not seen a further escalation in price pressures.

However, these developments, as de la Rubia notes, are “not enough” to alter the ECB’s tentative plan to commence rate cuts in June, rather than an earlier move in April.

Also released, France PMI Manufacturing fell from 47.1 to 45.8. PMI Services fell from 48.4 to 47.8. PMI Composite fell from 48.1 to 47.7.

Germany PMI Manufacturing fell from 42.5 to 41.6. PMI Services rose from 48.3 to 49.8. PMI Composite rose from 46.3 to 47.4.

BoJ’s Ueda assures continued accommodative monetary stance following rate hike

Addressing the parliament today, BoJ Governor Kazuo Ueda articulated the rationale behind this week’s exit from the long-standing negative interest rate policy and the subsequent rate hike. This move marks a significant shift for Japan’s monetary policy, which had been entrenched in a negative interest rate environment for eight years.

Ueda pointed out, “We could have waited until inflation is completely at 2% for a long period of time. But if we did so, it’s unclear whether inflation would have stayed at 2%. We might have seen a sharp increase in upside price risks,” highlighting the preemptive nature of the BoJ’s action.

The decision was influenced by recent trends in service prices and substantial wage increases resulting from annual wage negotiations, indicating a strengthening cycle of wage growth and inflation in Japan.

Despite this historical step, Ueda underscored that Japan’s inflation expectations for the medium and long term are “still in the process of accelerating towards 2%”. He assured that BoJ remains committed to supporting the economy and prices “by maintaining accommodative monetary conditions for the time being”.

He also hinted at future adjustments, stating, “As we exit our massive stimulus program, we will gradually shrink the size of our balance sheet and at some point reduce the size of our government bond buying.”

Japan’s PMI composite rises to 52.3, strengthening activity and intensifying price pressures

Japan’s PMI Manufacturing saw a modest increase from 47.2 to 48.2 in March, while PMI Services surged to from 52.9 to 54.9, its highest level since last May. Composite PMI, which combines both sectors, also climbed from 50.6 to 52.3, reaching its peak since last August.

Usamah Bhatti, Economist at S&P Global Market Intelligence, underscored the private sector’s regained momentum at the end of Q1. The expansion was predominantly driven by service providers, while manufacturers experienced a continued, though less severe, contraction.

Alongside this economic revival, Japan is facing a “renewed intensification of price pressures,” with the rate of input price inflation hitting a five-month high. This uptick was particularly pronounced among service providers, although manufacturers also reported “stubbornly high input prices”. Many firms opted to pass these increased costs onto customers, leading to the highest output charge inflation since last August.

Australia employment surges 116.5k, unemployment rate dives to 3.7%

Australia employment grew strongly by 116.5k in February, well above expectation of 40.2k. Full-time jobs rose 78.2k while part-time jobs rose 38.3k.

Unemployment rate fell sharply from 4.1% to 3.7%, below expectation of 4.0%. Participation rate rose 0.1% to 66.7%. Monthly hours worked also rose 2.8% mom.

Australia PMI composite rises to 11-month, another blow to RBA rate cut expectations

Australia PMI Manufacturing PMI dropped to a 46-month low of 46.8. Conversely, PMI Services climbed to an 11-month peak of 53.5, with the Composite PMI also reaching an 11-month high at 52.4.

Warren Hogan, Chief Economic Advisor at Judo Bank, highlighted that Composite Output Index’s increase for the fourth consecutive month signifies the economy’s rebound from the cyclical slowdown experienced in 2023. Meanwhile However, inflation remains a concern, with service sector readings indicating persistently high producer and consumer prices.

Hogan noted that the results are “another blow to rate-cut expectations” for RBA. The rebound in economic activity, coupled with inflation exceeding targets, not only diminishes the likelihood of rate reductions, but also raises the possibility of further monetary tightening in 2024. This aligns with recent warnings from RBA.

New Zealand in technical recession as Q4 GDP contracts -0.1% qoq

New Zealand’s economy has officially entered technical recession, with GDP contracting by -0.1% qoq in Q4, below expectation of 0.0% qoq. This decline follows -0.3% contraction in Q4, marking two consecutive quarters of negative growth.

GDP per capita declined decline of -0.7% qoq, while real gross national disposable income saw a -1.4% qoq drop.

The contraction was not uniformly felt across all sectors. Of the sixteen industries analyzed, eight experienced growth, notably the rental, hiring, and real estate services sector, alongside public administration, safety, and defense.

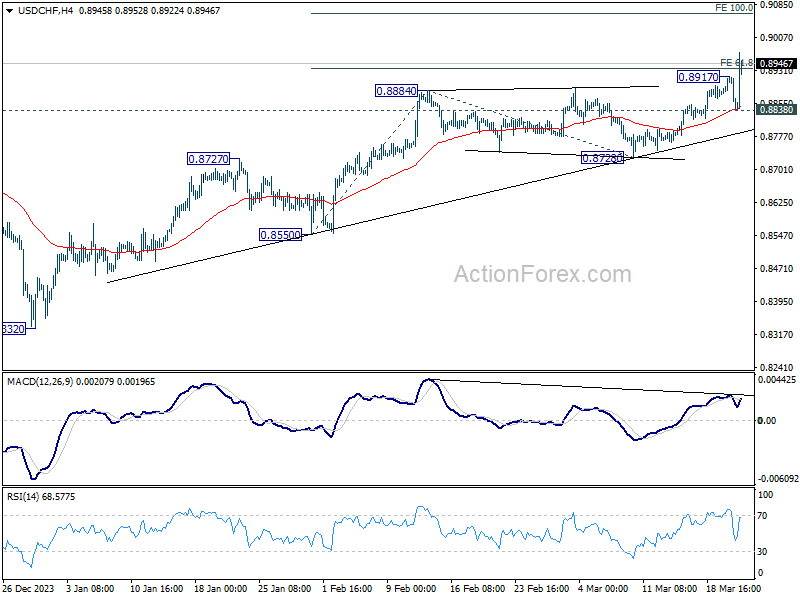

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8846; (P) 0.8882; (R1) 0.8905; More….

USD/CHF’s rally resumed after drawing support from 55 4H EMA, and breaks through 0.8917. Intraday bias is back on the upside. Next target is 100% projection projection of 0.8550 to 0.8884 from 0.8728 at 0.9062. On the downside, below 0.88338 minor support will turn intraday bias neutral again. But still, outlook will remain bullish as long as 0.8728 support holds.

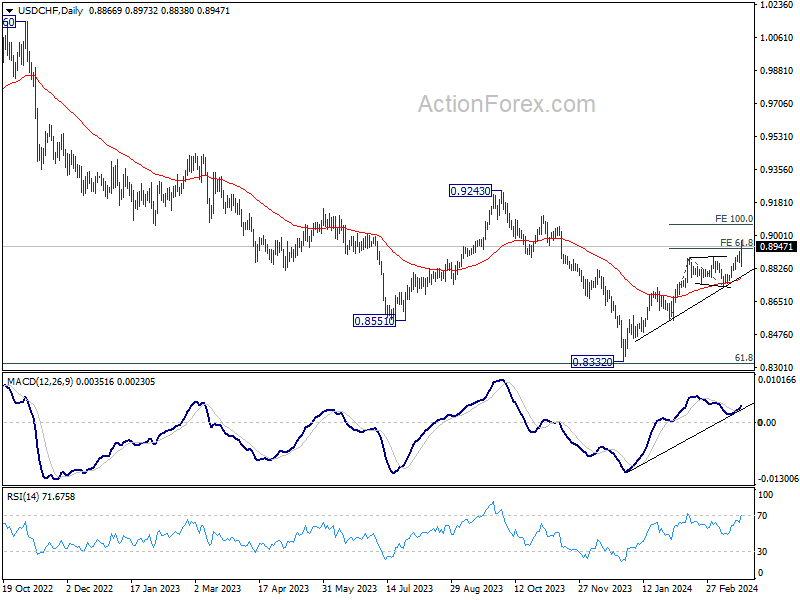

In the bigger picture, price actions from 0.8332 medium term bottom as seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8555 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | GDP Q/Q Q4 | -0.10% | 0.00% | -0.30% | |

| 22:00 | AUD | Manufacturing PMI Mar P | 46.8 | 47.8 | ||

| 22:00 | AUD | Services PMI Mar P | 53.5 | 53.1 | ||

| 23:50 | JPY | Trade Balance (JPY) Feb | -0.45T | -0.85T | 0.24T | 0.01T |

| 00:30 | JPY | Manufacturing PMI Mar P | 48.2 | 47.5 | 47.2 | |

| 00:30 | AUD | Employment Change Feb | 116.5K | 40.2K | 0.5K | 15.3K |

| 00:30 | AUD | Unemployment Rate Feb | 3.70% | 4.00% | 4.10% | |

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Feb | 7.5B | 5.2B | -17.6B | -17.0B |

| 08:15 | EUR | France Manufacturing PMI Mar P | 45.8 | 47.3 | 47.1 | |

| 08:15 | EUR | France Services PMI Mar P | 47.8 | 48.6 | 48.4 | |

| 08:30 | EUR | Germany Manufacturing PMI Mar P | 41.6 | 43.5 | 42.5 | |

| 08:30 | EUR | Germany Services PMI Mar P | 49.8 | 48.9 | 48.3 | |

| 08:30 | CHF | SNB Interest Rate Decision | 1.50% | 1.75% | 1.75% | |

| 09:00 | CHF | SNB Press Conference | ||||

| 09:00 | EUR | ECB Economic Bulletin | ||||

| 09:00 | EUR | Eurozone Current Account (EUR) Jan | 39.4B | 32.3B | 31.9B | |

| 09:00 | EUR | Eurozone Manufacturing PMI Mar P | 45.7 | 47 | 46.5 | |

| 09:00 | EUR | Eurozone Services PMI Mar P | 51.1 | 50.5 | 50.2 | |

| 09:30 | GBP | Manufacturing PMI Mar P | 49.9 | 47.8 | 47.5 | |

| 09:30 | GBP | Services PMI Mar P | 53.4 | 53.8 | 53.8 | |

| 12:00 | GBP | BoE Interest Rate Decision | 5.25% | 5.25% | 5.25% | |

| 12:00 | GBP | MPC Official Bank Rate Votes | 0–1–8 | 0–1–8 | 2–1–6 | |

| 12:30 | CAD | New Housing Price Index M/M Feb | 0.10% | 0.10% | -0.10% | |

| 12:30 | USD | Initial Jobless Claims (Mar 15) | 210K | 210K | 209K | |

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Mar | 3.2 | 0.2 | 5.2 | |

| 12:30 | USD | Current Account (USD) Q4 | -195B | -209B | -200B | |

| 13:45 | USD | Manufacturing PMI Mar P | 51.9 | 52.2 | ||

| 13:45 | USD | Services PMI Mar P | 52 | 52.3 | ||

| 14:00 | USD | Existing Home Sales Feb | 3.94M | 4.00M | ||

| 14:30 | USD | EIA Natural Gas Storage Change (Mar 15) | 5B | -9B |