Precious Metals Shine as Global Markets Await Central Bank Decisions and Data – Action Forex

As Asian session unfolded, the forex markets have been relatively quiet. Precious metals, on the other hand, are making headlines with Gold soaring above new record high above 2350 mark and Silver also rallies significantly. Nikkei is having a notable rebound even though 40k psychological level could remain a strong resistance to cap upside. Oil prices dip slightly on news that Israel is withdrawing more soldiers from southern Gaza, but the retreat is so far limited.

In the currency markets, Dollar and Euro are showing some strength while Swiss Franc and Yen are lagging behind. Today’s trading might remain subdued due to a lack of significant economic data from North America. Yet this could be just the calm before storm. The week ahead is packed with crucial events, including policy decisions from the RBNZ, BoC, and ECB, as well as key data releases like the FOMC minutes, US CPI, and UK GDP, which are poised to inject volatility into the markets.

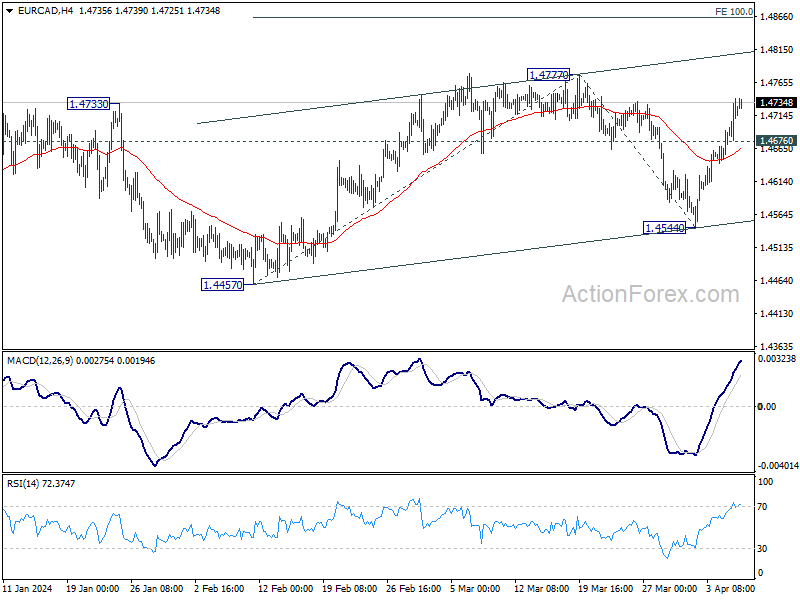

Technically, EUR/CAD would be an interesting one in the next couple of days. Bias is now on the upside after last week’s rally. Further rally is expected as long as 1.4676 minor support holds, to 1.4777 resistance. Firm break there will resume the whole rebound from 1.4457 and target near term channel resistance (now at 1.4809), and probably further to 100% projection of 1.4457 to 1.4777 from 1.4544 at 1.4864.

In Asia, at the time of writing, Nikkei is up 0.76%. Hong Kong HSI is down -0.09%. China Shanghai SSE is down -0.17%. Singapore Strait Times is down -0.05%. Japan 10-year JGB yield is up 0.0146 at 0.786.

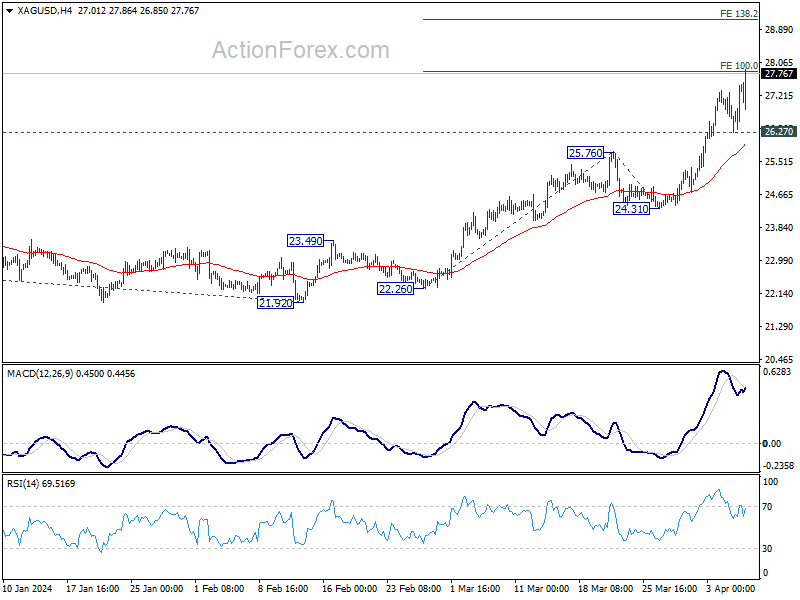

Silver surges with eyes on 30 key cluster resistance

Silver’s up trend continues in Asian session today and hits the highest level since mid-2021. For now, near term outlook will stay bullish as long as 26.27 support holds. Next target is 138.2% projection of 22.26 to 25.76 from 24.31 at 29.14. However, Silver could start to feel heavy above this level, and establish a top around there.

Current rise from 21.92 is part of the up trend from 17.54 (2022 low). Overbought condition could cap the upside, at least on first attempt, around 30 cluster resistance level. That include 30 psychological number, 2021 high at 30.07, and 100% projection of 17.54 to 26.12 from 21.92 at 30.50.

Japan’s nominal wages rise 1.8% yoy in Feb, real wages down -1.3% yoy

Japan’s nominal labor cash earnings rose by 1.8% yoy in February, aligning with market expectations and marking a 26-month streak of increases. Monthly wages saw 2.0% yoy increase, with regular pay rising by 2.2% yoy. However, over-time pay decreased of -1.0% yoy, and special payments fell significantly by -5.5% yoy.

Real wages fell by 1.3% yoy, marking the 23rd consecutive month of decline. This trend underscores the continuing issue of rising living costs eroding purchasing power of Japanese workers,

A Ministry of Health, Labor, and Welfare official noted, “We will monitor how growth in nominal pay will develop while price gains are weighing down real wages.”

RBNZ, BoC, ECB, FOMC Minutes, US CPI, UK GDP as highlights of the week

This upcoming week is a busy one globally with three central banks in three regions – RBNZ, BoC, and ECB – set to announce their interest rate decisions. Market participants are bracing for these announcements, alongside a series of influential economic data releases that could sway market sentiment and monetary policy outlooks.

RBNZ is expected to maintain OCR at 5.50%. A recent Reuters poll revealed a divided forecast among economists, with a slight majority of 15 to 19 anticipating the first rate reduction by the end of Q3. Others, 14 economists, expect a hold until Q4 or later. Financial institutions like Bank of New Zealand, ASB Bank, and Kiwibank are projecting a Q4 cut, with ANZ and Westpac suggesting a push into Q1 and Q2 2025 respectively. Given this backdrop, RBNZ is unlikely to alter its current narrative significantly at this meeting. Observers look through to next meeting with new economic projections set to be released in May.

BoC is similarly poised to keep its policy rate unchanged at 5.00%. Last week’s weak job data has fueled increasing market bets for a mid-year rate cut, with expectations for a June reduction now surpassing 75%. January’s and February’s inflation figures showing a return to within the 1-3% target range add to the anticipation that the BoC could commence interest rate reductions by mid-year. Governor Tiff Macklem’s statements post-meeting will be scrutinized for any signals of the central bank’s next move.

ECB is anticipated to hold main refinancing rate at 4.50% and deposit rate at 4.00%. The majority of ECB official are leaning towards a June cut, contingent on supportive Q1 wage data available in May. A Bloomberg survey highlights a broader anticipation of gradual easing, with economists forecasting a consistent 25ps reduction each quarter, to lower deposit rate to 2.25% by the end of 2025. Market pricing, characteristically more aggressive, are pricing in an approximate 90bps of easing within this year alone. But for now, it’s unlikely for Lagarde to talk about anything concrete beyond June, other than laying the groundwork for the first reduction.

Minutes from the FOMC‘s March session will also be closely scrutinized. The dot plot released at the meeting showed a tight split among policymakers, with 10 pencilling in three rate reductions this year, whereas nine leaned towards two or fewer. Notably, there were 2 members who envisioned no cuts at all, and 2 others who foresaw just a single cut. The minutes would hopefully offer deeper insight into the Committee’s deliberations, clarifying the rationale behind the varied projections and the key factors influencing members’ outlooks.

Furthermore, a host of economic data, headlined by US CPI will play a crucial role in shaping expectations for Fed’s June decision. Other notable releases, including US PPI and University of Michigan consumer sentiment, UK GDP, and China’s inflation data, will also command attention.

Here are some highlights of the week:

- China CPI, PPI, inflation.

- Monday: Japan cash earnings, current account; Swiss unemployment rate; Germany industrial production trade balance; Eurozone Sentix investor confidence.

- Tuesday: New Zealand NZIER business confidence; Australia Westpac consumer sentiment, NAB business confidence; japan consumer confidence.

- Wednesday: Japan PPI; RBNZ rate decision; Italy retail sales; US CPI, FOMC minutes; BoC rate decision.

- Thursday: Australia inflation expectations; China CPI, PPI; Italy industrial production; ECB rate decision; US PPI, jobless claims.

- Friday: New Zealand BNZ manufacturing; China trade balance; Germany CPI final; UK GDP, production, trade balance; US import prices, U of Michigan consumer sentiment.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8988; (P) 0.9029; (R1) 0.9061; More….

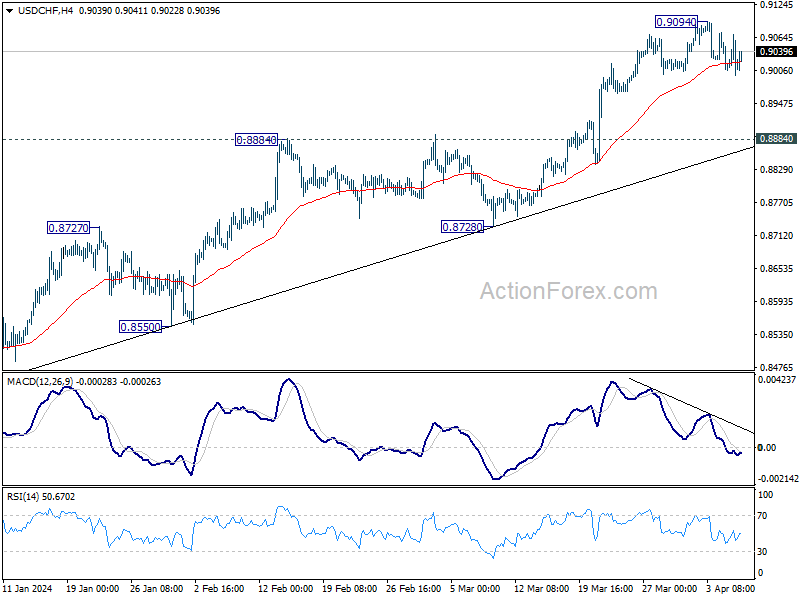

USD/CHF is staying in consolidation below 0.9094 and intraday bias remains neutral. Deeper decline cannot be ruled out, but outlook will stay bullish as long as 0.8884 resistance turned support holds. On the upside, break of 0.9094 will resume larger rise from 0.8332 to 0.9243 key resistance.

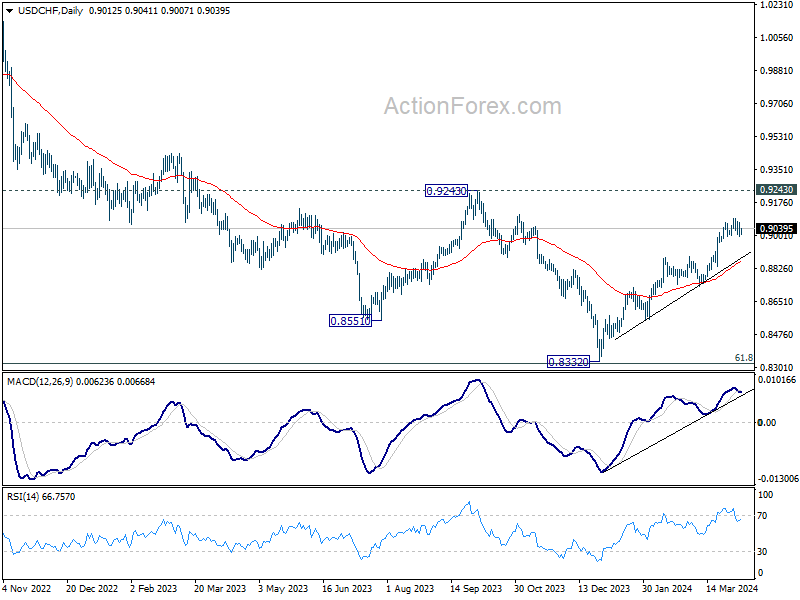

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8728 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Feb | 1.80% | 1.80% | 2.00% | |

| 23:50 | JPY | Current Account (JPY) Feb | 1.37T | 1.99T | 2.73T | 2.75T |

| 05:00 | JPY | Eco Watchers Survey: Current Mar | 51.6 | 51.3 | ||

| 05:45 | CHF | Unemployment Rate Mar | 2.20% | 2.20% | ||

| 06:00 | EUR | Germany Industrial Production M/M Feb | 0.60% | 1.00% | ||

| 06:00 | EUR | Germany Trade Balance (EUR) Feb | 25.1B | 27.5B | ||

| 08:30 | EUR | Eurozone Sentix Investor Confidence Apr | -8.3 | -10.5 |