Kiwi Unfazed by Business Confidence Slide, Aussie Maintains Solid Ground – Action Forex

New Zealand Dollar traded broadly higher in Asian session, despite revelation of significant downturn in business confidence for Q1. Kiwi bears seemed to be lightening up their short positions in anticipation of RBNZ rate decision tomorrow, which is broadly expected to maintain interest rate at 5.50%. The market’s recent aggressive speculation on an early rate cut by RBNZ is tempered by the likelihood that the central bank will resist such expectations. Any shift in stance is unlikely for tomorrow, and would be delayed until its next meeting in May, with a fresh set of economic projections as guidance.

Australian Dollar also showed some strength, outperforming Kiwi slightly despite facing headwinds from persistently weak consumer sentiment indicators. The resilience in business conditions data and gradual easing in inflationary pressures would contribute to the cautious stance by RBA against early rate cuts. Besides, Aussie’s performance is further bolstered by the recent strong rally in copper prices and the general rebound in Asian stock markets today.

Japanese Yen remains under pressure, though without significant selling momentum at this stage. Japanese Finance Minister Shunichi Suzuki emphasized at a news conference that while the country does not target specific currency levels, it values the stability of exchange rates that reflect economic fundamentals. This statement suggests a continued vigilance against undue volatility, keeping Yen bears cautious of intervention. At the same time, there is clear lack of buying interest on Yen for a rebound.

Elsewhere, Dollar, Euro, and Sterling are mixed as the market’s are holding their bets towards upcoming key events. These include US CPI data release tomorrow, ECB rate decision on Thursday, and UK GDP on Friday.

Technically, a short term bottom should be in place at 0.5938 in NZD/USD with break of 0.6037 support turned resistance. Further rebound is mildly in favor for now, but strong resistance should be seen between 55 D EMA (now at 0.6078) and channel resistance (now at 0.6148) to cap upside. Below 0.5894 minor support will argue that fall from 0.6368 is ready to resume through 0.5938.

In Asia, at the time of writing, Nikkei is up 0.78%. Hong Kong HSI is up 0..55%. China Shanghai SSE is down -0.15%. Singapore Strait Times is up 0.87%. Japan 10-year JGB yield is down -0.0005 at 0.791. Overnight, DOW fell -0.03%. S&P 500 fell -0.04%. NASDAQ rose 0.03%. 10-year yield rose 0.069 to 4.378.

NZ NZIER business confidence tumbles, high interest rates deepen pessimism

In Q1, New Zealand’s business community signaled a stark downturn in confidence, with NZIER business confidence index plunging from -9.9 to -23.7 . This dramatic drop is accompanied by reversal in firms’ trading activity expectations for the coming quarterly, from 6.6 to -11.5, as well as retrospective decline in past three months’ trading activity from 6.7 to -23.2.

NZIER attributes this downturn to the effect of heightened interest rates, which appear to be fulfilling their role in tempering demand to alleviate inflationary pressures. Moreover, the looming uncertainty surrounding the new Government’s fiscal strategies, particularly in terms of spending adjustments and cutbacks in the public sector, is exacerbating business caution.

Detailed further illuminates the current economic challenges, with a net 11% of firms having reduced their workforce in the March quarter, albeit with slightly positive hiring intentions moving forward. Investment intentions are also on the downturn, with a net 14% of businesses intending to cut back on plant and machinery investment, and a net 8% planning to curtail investment in buildings over the next year.

Australia Westpac consumer sentiment falls to 82.4, prolonged pessimism

Australia Westpac Consumer Sentiment Index marked a decrease of -2.4% mom to 82.4 in April. This downturn extends the index’s streak below the neutral threshold of 100 to nearly two years, underscoring a prolonged period of consumer pessimism.

Westpac’s analysis attributes the lack of recovery in consumer sentiment primarily to the ongoing inflationary pressures that have gripped Australia. Over the past three years, consumer prices have risen significantly, outpacing wage growth by six percentage points. This inflationary trend, coupled with the notable rise in interest rates and increased tax burdens, has significantly strained household incomes, subjecting them to prolonged financial duress.

As attention turns to RBA’s next meeting in May, Westpac anticipates no change to the official cash rate. This forecast hinges significantly on the upcoming March quarter CPI update, due on April 24, which is expected to play a crucial role in shaping the RBA’s stance.

Australia NAB business confidence rises to 1, cost pressures show slight relief

Australia NAB Business Confidence rose from 0 to 1 in March. Business Conditions fell from 10 to 9. Trading Conditions and employment conditions held steady at 15 and 6 respectively. But profitability conditions decline notably from 10 to 6.

Alan Oster, NAB’s Chief Economist, pointed out the unusual situation where business conditions have been “a little above average” and confidence “a little below average” for an extended period. This, according to Oster, reflects a cautious outlook among firms regarding the future, even as the economy shows signs of resilience.

Further details from the report indicate a softening in cost pressures. Labor cost growth decelerated to 1.6% on quarterly equivalent basis, down from 2.0%. Purchase cost growth slowed to 1.4% from 1.8%. Additionally, there was a moderation in product price growth to 0.7% from 1.2%, with retail price growth slightly reducing to 1.3% from 1.4%. Despite these easing pressures, cost concerns remain high, with retail price growth still elevated.

Oster interprets these figures as being aligned with expectations that the journey towards inflation normalization will be “gradual”. Q1 PI result later in April is expected to further reinforced this view.

Looking ahead

France trade balance and US NFIB small business index are the only feature of the day.

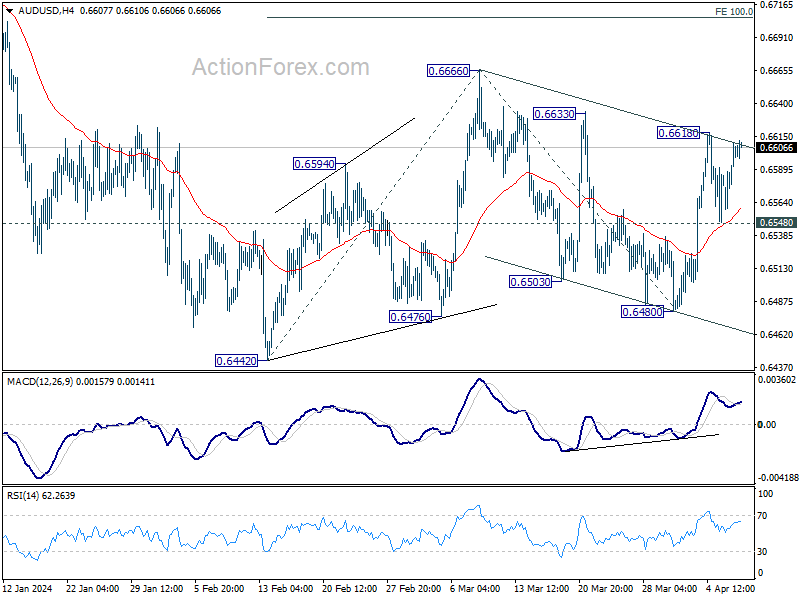

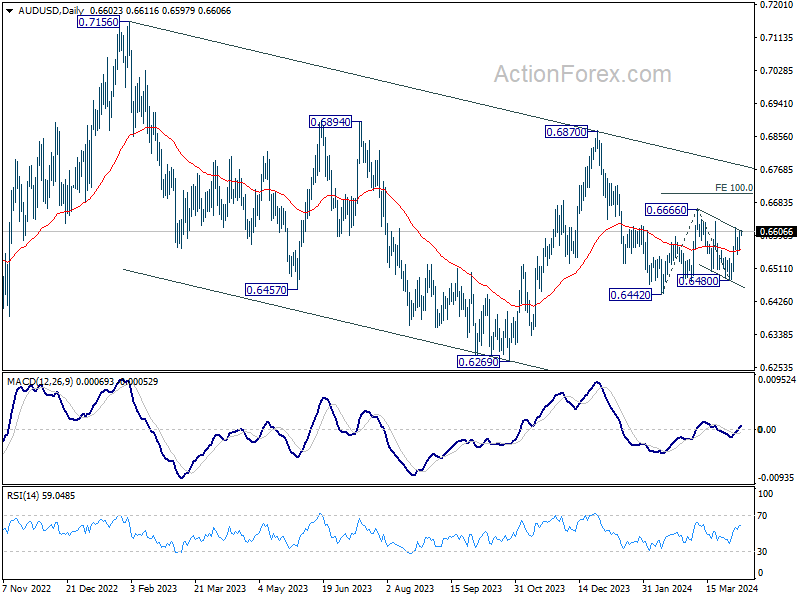

AUD/USD Daily Report

Daily Pivots: (S1) 0.6573; (P) 0.6592; (R1) 0.6623; More….

Intraday bias in AUD/USD remains neutral first. On the upside, break of 0.6618 resistance will affirm the case that rise from 0.6480 is the third leg of the pattern from 0.6442 low. Intraday bias will be back on the upside for 0.6666 resistance, and then 100% projection of 0.6442 to 0.6666 from 0.6480 at 0.6704. Nevertheless, break of 0.6480 support will bring retest of 0.6442 low instead.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which might still be in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:00 | NZD | NZIER Business Confidence Q1 | -25 | -2 | ||

| 23:01 | GBP | BRC Like-For-Like Retail Sales Y/Y Mar | 3.20% | 1.80% | 1.00% | |

| 00:30 | AUD | Westpac Consumer Confidence Apr | -2.40% | -1.80% | ||

| 01:30 | AUD | NAB Business Confidence Mar | 1 | 0 | ||

| 01:30 | AUD | NAB Business Conditions Mar | 9 | 10 | ||

| 05:00 | JPY | Consumer Confidence Mar | 39.5 | 39.7 | 39.1 | |

| 06:00 | JPY | Machine Tool Orders Y/Y Mar P | -8.00% | |||

| 06:45 | EUR | France Trade Balance (EUR) Feb | -7.0B | -7.4B | ||

| 10:00 | USD | NFIB Business Optimism Index Mar | 90.2 | 89.4 |