Forex Markets Await Direction with Key US Economic Data on the Horizon – Action Forex

In a typical Monday’s Asian trading session, the forex markets remained relatively subdued, with only modest movements observed. A mild sense of risk aversion was noted in the stock markets of Hong Kong and China, which exerted slight downward pressure on commodity currencies. This sentiment was largely driven by the disappointing official China PMI manufacturing data released over the weekend, which reported a fourth consecutive month of contraction. However, the impact on the markets was somewhat mitigated by the relatively better Caixin PMI manufacturing data, providing a partial offset to the overall negative outlook.

Looking ahead, this week will be pivotal in shaping market expectations for Fed’s policy easing path for the remainder of the year. A rate cut is almost certain after Fed Chair Jerome Powell stated at the Jackson Hole Symposium that the “time has come” for a policy adjustment. However, there is still considerable uncertainty regarding the magnitude of the initial cut and the pace of any subsequent reductions. Key indicators such as ISM manufacturing and services indexes, along with the all-important non-farm payrolls report, are expected to offer critical insights into the Fed’s next steps.

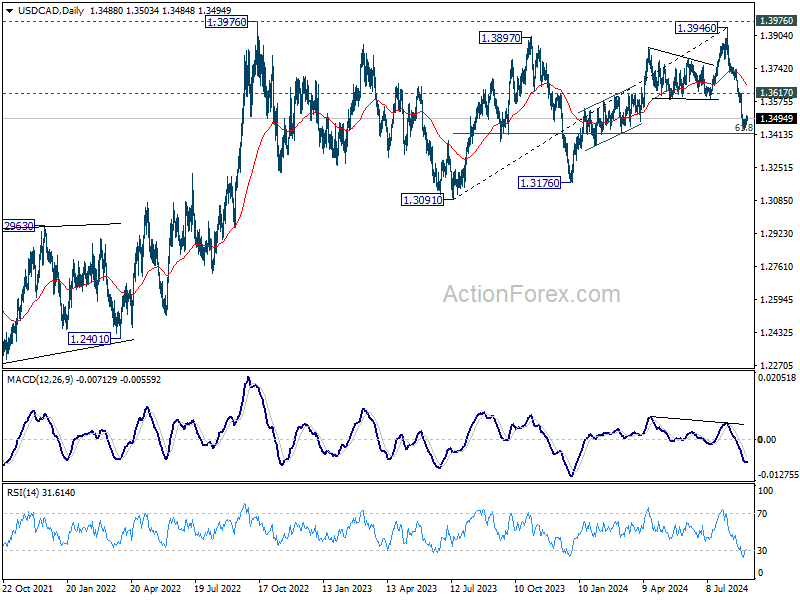

A key currency pair to monitor this week is USD/CAD, as BoC is widely expected to announce its third consecutive interest rate cut. Technically, decline from 1.3946 is seen as a falling leg inside the range pattern from 1.3976 (2022 high). The fall halted just ahead of 61.8% retracement of 1.3091 to 1.3946 at 1.3418. Further decline is in favor as long as 1.3617 resistance holds. Firm break of 1.3418 will target 1.3091/3176 support zone next.

In Asia, at the time of writing, Nikkei is up 0.16%. Hong Kong HSI is down -1.79%. China Shanghai SSE is down -0.68%. Singapore Strait Times is up 0.31%. Japan 10-year JGB yield rose 0.0186 to 0.912.

Japan’s PMI manufacturing finalized at 49.8, close to stabilization amid rising cost burdens

Japan’s Manufacturing PMI for August was finalized at 49.8, showing a slight improvement from July’s 49.1, but still indicating a marginal contraction. S&P Global noted that the sector is moving closer to stabilization, with a renewed rise in production. This marks the first increase in purchasing activity in two years.

According to Usamah Bhatti at S&P Global Market Intelligence, the latest figures paint a “mixed picture” as the sector hovers near stabilization. The renewed rise in production and a softer decline in new orders have encouraged firms to increase staffing levels, while the pace of destocking has slowed. Additionally, there have been signs of improved supplier performance, particularly in the availability of inputs like electrical components.

However, the data also pointed to significant cost pressures, with the strongest rise in input costs since April 2023. Despite this, companies have been reluctant to pass these higher costs onto customers fully, leading to the slowest rate of charge inflation since mid-2021.

China’s Caxin PMI manufacturing rises to 50.4, modest return to expansion

China’s Caixin PMI Manufacturing rose slightly in August, reaching 50.4 from July’s 49.8, signaling a modest return to expansion. The improvement reflects faster output growth and stabilization in employment after an 11-month decline. Meanwhile, average selling prices and input costs continued to decline, indicating ongoing deflationary pressures within the sector.

Wang Zhe, Senior Economist at Caixin Insight Group, noted that while PMI manufacturing returned to expansionary territory, the growth remains “limited”. He highlighted the significant challenges China faces in stabilizing its economic growth, particularly given the government’s ambitious annual targets. Key issues include weak domestic demand, uncertainties in external demand, and low market optimism, all of which could hinder sustained growth.

In contrast, the official NBS data released over the weekend painted a more subdued picture. NBS PMI Manufacturing fell from 49.5 to 49.1 in August, indicating a deeper contraction in the sector. While PMI Non-Manufacturing ticked up slightly from 50.1 to 50.3, the PMI Composite dropped for the fifth consecutive month, landing at 50.1—the lowest since December 2022.

NBS statistician Zhao Qinghe attributed the decline in manufacturing to several factors, including extreme weather, off-season production in certain industries, insufficient demand, and fluctuations in commodity prices.

NFP to steer Fed’s easing path, BoC to lower rates again

This week holds significant implications for Fed ahead of its September 17-18 meeting, as key economic indicators, including the ISM manufacturing and services reports, and the all-important non-farm payroll data, are set to be released.

The labor market, in particular, is under scrutiny following Fed Chair Jerome Powell’s recent remarks at the Jackson Hole symposium, where he emphasized the commitment to maintaining a robust labor market while progressing toward price stability.

Powell explained that with the labor market already less tight than pre-pandemic conditions, Fed does not anticipate it to be a major source of inflationary pressure in the near term. He also emphasized that policymakers “do not seek or welcome further cooling in labor market conditions”.

So all in all, any marked deterioration in employment conditions could prompt Fed to adopt a more aggressive easing stance.

Besides, the markets could be particularly sensitive to the upcoming NFP too. Last month’s data sparked concerns by triggering the Sahm Rule, a reliable recession indicator, and prompted huge selloff in the stock markets. Unemployment rate’s jump from 4.1% to 4.3% in July pushed the three-month average above the 12-month low by more than the critical 0.5% threshold, a level historically associated with the onset of a recession.

This development raises the stakes for this week’s report, as a further increase in unemployment could reinforce fears of a deeper economic downturn and, at the same time, force Fed’s hand in policy adjustment.

In parallel, global markets are also focused on BoC, which is widely expected to cut its interest rate by 25 bps for the third consecutive meeting, bringing the rate down to 4.25%. A recent Reuters survey indicated unanimous expectation among economists for this outcome, with a majority predicting additional cuts in October and December, lowering rates to 3.75% by year-end. BoC Governor Tiff Macklem’s comments will be closely monitored for further dovish signals. Meanwhile, Canadian employment data is also set to be released this week.

In Europe, the focus will be on Switzerland’s CPI and GDP data. Markets are currently assigning a 70% probability of a 25 basis point rate cut by SNB at its next meeting on September 26. There is also a 30% chance of a more substantial 50 bps reduction. These expectations hinge on upcoming Swiss CPI and GDP data, which, if weaker than expected, could bolster the case for a larger cut.

Australia’s Q2 GDP figures will provide critical insight ahead of RBA’s next meeting on September 24. Despite the global trend towards easing, RBA has indicated that it is unlikely to reduce rates this year. Such expectations wouldn’t change barring any disastrous GDP results. Australian traders will also keep an eye on China’s Caixin PMI data, given its potential impact on the Australian economy.

Here are some highlights for the week

- Monday: Japan PMI manufacturing final; Australia building permits; China Caixin PMI manufacturing; Swiss retail sales; Eurozone PMI manufacturing final; UK PMI manufacturing final.

- Tuesday: New Zealand terms of trade; Japan monetary base; Australia current account; Swiss CPI, GDP; Canada PMI manufacturing; US ISM manufacturing.

- Wednesday: Australia GDP; China Caixin PMI services; Eurozone PMI services final, PPI; UK PMI services final; Canada trade balance, BoC rate decision; US trade balance, factory orders, Fed’s Beige Book.

- Thursday: Japan average cash earnings; Australia trade balance; Swiss unemployment rate; UK PMI construction; Eurozone retail sales; US ADP employment, jobless claims; ISM services.

- Friday: Japan household spending leading indicators; Germany industrial production, trade balance; France trade balance, industrial production; Swiss foreign currency reserves, SECO consumer climate; Eurozone GDP revision; Canada employment, Ivey PMI; US non-farm payrolls.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6739; (P) 0.6778; (R1) 0.6803; More...

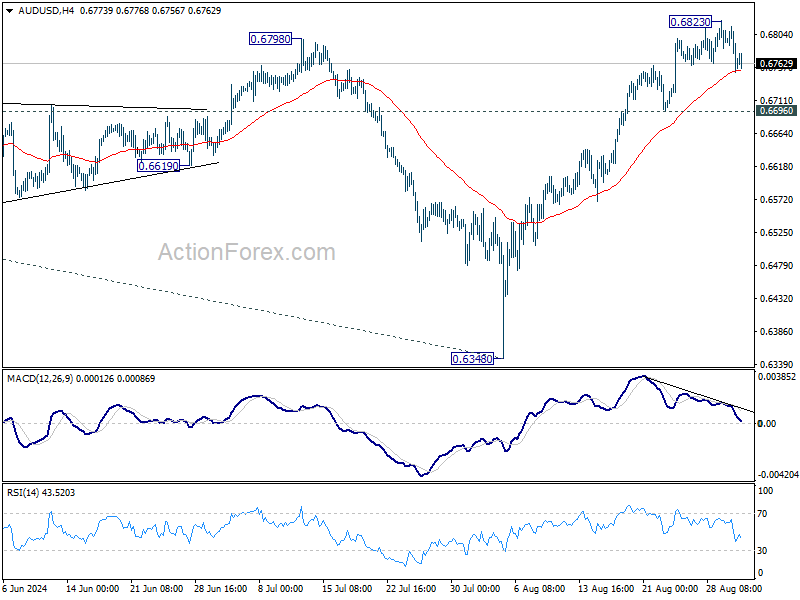

AUD/USD is extending the consolidation pattern from 0.6823 and intraday bias remains neutral. On the upside, break of 0.6823 will target 0.6870 resistance. Firm break there will target 100% projection of 0.6269 to 0.6870 from 0.6348 at 0.6949. However, break of 0.6696 support will indicate short term topping, on bearish divergence condition in 4H MACD, and turn bias back to the downside for deeper pullback.

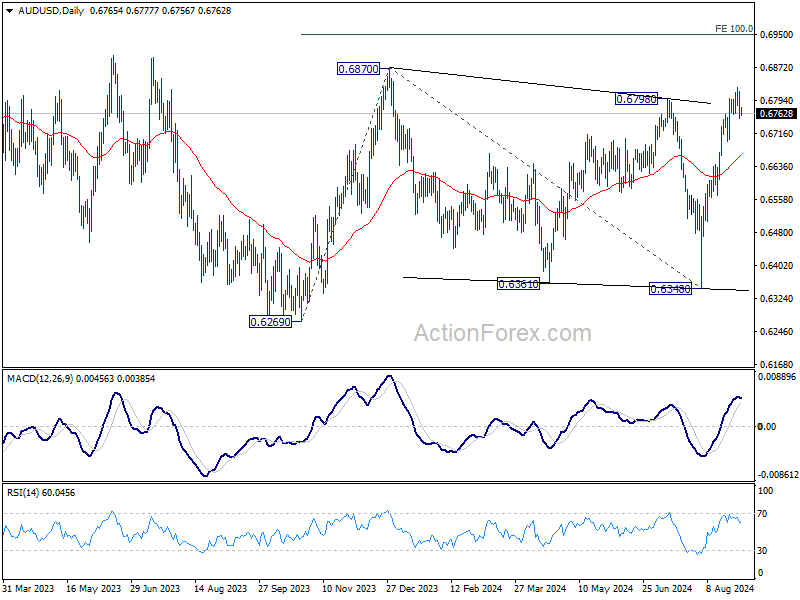

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with rise from 0.6269 as the third leg. Firm break of 0.6798/6870 resistance zone will target 0.7156 resistance. In case of another fall, strong support should be seen from 0.6169/6361 to bring rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Capital Spending Q2 | 7.40% | 9.90% | 6.80% | |

| 00:30 | JPY | Manufacturing PMI Aug F | 49.8 | 49.5 | 49.5 | |

| 01:30 | AUD | Company Gross Operating Profits Q/Q Q2 | -5.30% | -0.40% | -2.50% | |

| 01:30 | AUD | Building Permits M/M Jul | 10.40% | 2.40% | -6.50% | -6.40% |

| 01:45 | CNY | Caixin Manufacturing PMI Aug | 50.4 | 50.0 | 49.8 | |

| 06:30 | CHF | Retail Sales Y/Y Jul | -0.20% | -2.20% | ||

| 07:30 | CHF | Manufacturing PMI Aug | 43.7 | 43.5 | ||

| 07:50 | EUR | France Manufacturing PMI Aug F | 42.1 | 42.1 | ||

| 07:55 | EUR | Germany Manufacturing PMI Aug F | 42.1 | 42.1 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Aug F | 45.6 | 45.6 | ||

| 08:30 | GBP | Manufacturing PMI Aug F | 52.5 | 52.5 |