Global Markets Cool as Fed Boost Fades, Caution Dominates Late August Trade – Action Forex

Global market sentiment has cooled to start the week, with major European indexes trading mildly lower alongside softer U.S. futures. The lift from Fed Chair Jerome Powell’s dovish pivot appears to have run its course for now, leaving investors more hesitant during the final days of August.

While some profit-taking is likely, the prospect of a steep pullback looks limited given markets are firmly priced for a September Fed cut. At the same time, traders are wary of adding fresh exposure ahead of next week’s crucial U.S. jobs data, which could determine whether the Fed follows through on easing at its September 16–17 meeting.

Currency markets reflected the cautious tone, with overall activity sluggish. Aussie led gains, followed by Kiwi and Loonie, all of which face key domestic events this week including RBA minutes, Australia CPI, New Zealand business confidence, and Canada GDP.

On the weaker side, Yen underperformed, trailed by Euro and Swiss Franc. The Yen will be sensitive to Friday’s Tokyo CPI, while Switzerland releases GDP later in the week. Euro showed little reaction to today’s German Ifo survey. Sterling Dollar hold mid-pack positions.

In Europe, UK is on holiday. DAX is down -0.26%. CAC is down -0.73%. Germany 10-year yield is up 0.047 at 2.773. Earlier in Asia, Nikkei rose 0.41%. Hong Kong HSI rose 1.94%. China Shanghai SSE rose 1.51%. Singapore Strait Times rose 0.08%. Japan 10-year JGB yield rose 0.002 to 1.621.

German Ifo business climate edges higher to 89.0, recovery still weak

Germany’s Ifo business climate index rose modestly in August, climbing to 89.0 from 88.6 and beating expectations of 88.3. The improvement was driven by stronger expectations, with the sub-index rising to 91.6 from 90.7. Current assessment slipped from 86.5 to 86.4. Ifo said sentiment among companies has “brightened slightly,” but warned that the recovery “remains weak.”

Sector details painted a mixed picture. Manufacturing sentiment deteriorated further from -11.9 to -12.2, with firms less satisfied about current conditions and order intake still showing no signs of growth, though capital goods makers saw noticeable improvement.

Services dipped from 2.8 to 2.6 as expectations turned cautious despite a stronger current situation. Trade slumped from -20.3 to -21.4 on weaker performance. Construction slipped from -14.3 to -15.3, as firms were less satisfied with current conditions even as their outlook improved.

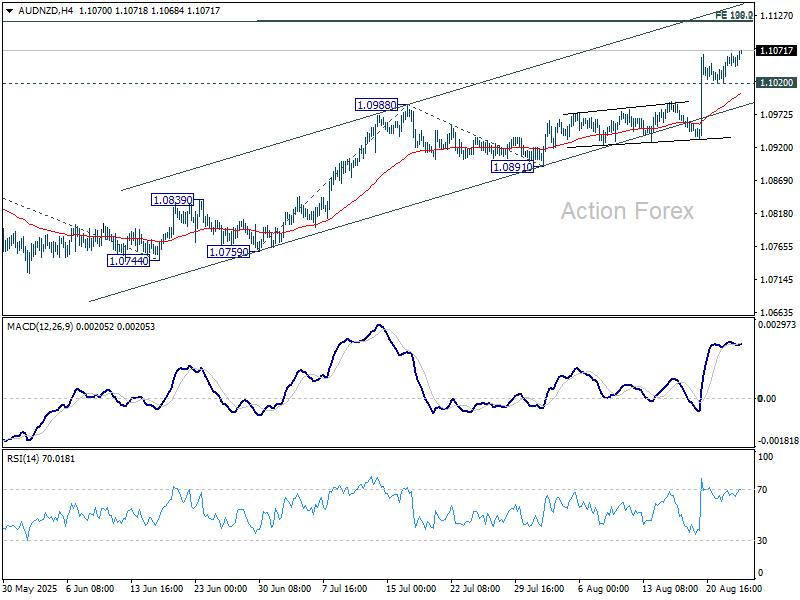

AUD/NZD rally intact, busy week with RBA minutes, Aussie CPI and NZ confidence

AUD/NZD could see sharp moves this week as markets digest a run of significant releases from both economies. RBA minutes on Tuesday, Australia’s monthly July CPI on Wednesday, and New Zealand’s ANZ business confidence survey on Thursday are possible movers.

In New Zealand, Q2 retail sales offered an upside surprise today. Headline volumes rose 0.5% qoq, beating expectations of 0.2%, while ex-auto sales jumped 0.7% qoq, defying forecasts of contraction. However, the Kiwi failed to capitalize, remaining pressured after last week’s dovish RBNZ decision. Markets have since shifted toward expecting two more rate cuts before the easing cycle ends.

RBNZ Governor Christian Hawkesby reinforced that view by stressing that both remaining policy meetings this year are “live.” This leaves scope for either two consecutive cuts in 2025, or one this year and one early next year, depending on how upcoming economic data evolves.

Meanwhile, the RBA appears more deliberate. After cutting 25bps earlier this month, the new projections signaled that one additional cut this year and two in 2026 remain the likely path under current assumptions. November is seen as the more appropriate window for action, allowing time to absorb Q3 CPI data. This week’s minutes and July’s monthly CPI release will be important checks on whether that outlook holds.

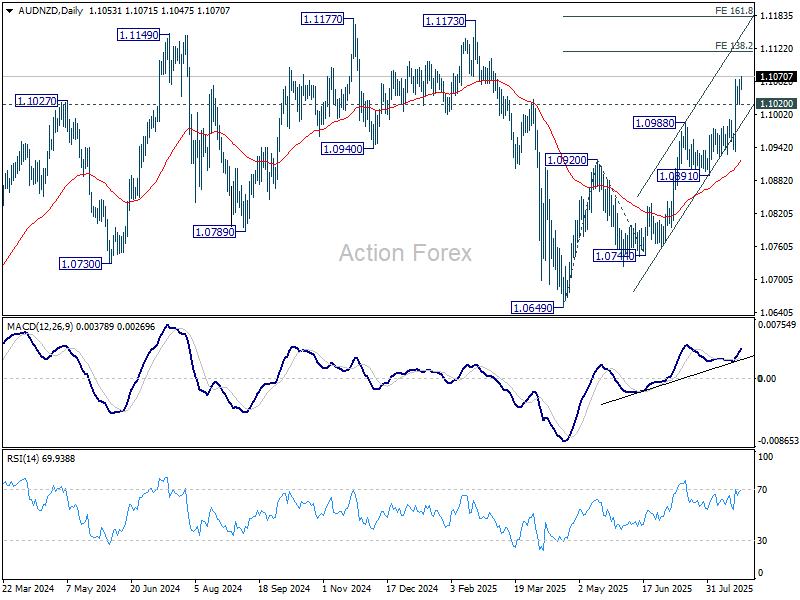

Technically, AUD/NZD’s near-term rally remains intact, supported by firm momentum on D MACD. As long as 1.1020 holds, further gains are likely, with scope toward the 138.2% projection of 1.0649 to 1.0920 from 1.0744 at 1.1119.

However, there is no clear sign of medium term range breakout yet. Hence, AUD/NZD would likely lose momentum above 1.119. Upside should be capped by 161.8% projection at 1.1182, which is slightly above key resistance of 1.1177 (2024 high).

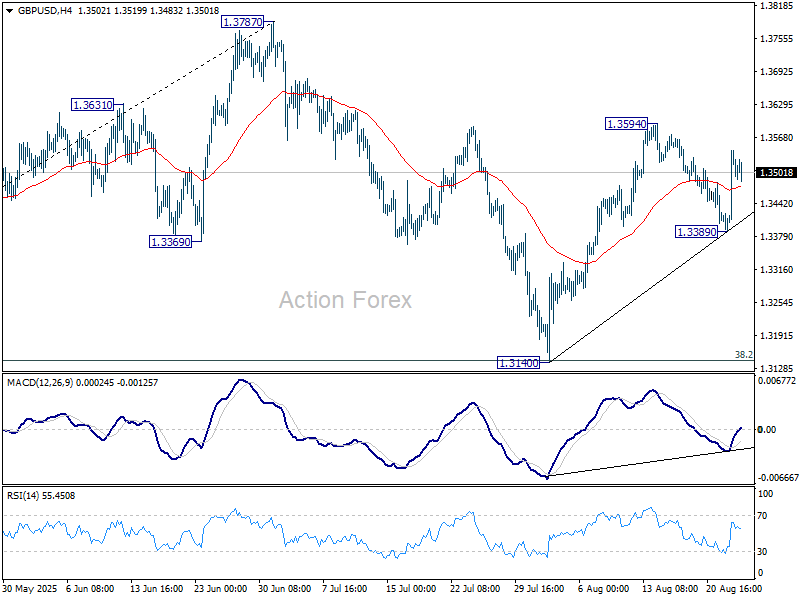

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3431; (P) 1.3487; (R1) 1.3584; More…

GBP/USD is still bounded in range of 1.3389/3594 and intraday bias stays neutral. Overall, price actions from 1.3787 high are seen as a corrective pattern. On the upside, break of 1.3594 will resume the rebound from 1.3140 to retest 1.3787 high. Firm break there will resume the larger up trend. For now, risk will stay on the upside as long as 1.3389 support holds, in case of retreat.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3073) holds, even in case of deep pullback.