Reciprocal Tariffs Take Effect; China Hit with 104% Rate – Action Forex

The rebound in US stock markets proved short-lived, with major indexes slipping back into the red by the end of Tuesday’s session. NASDAQ led the losses, as sentiment turned increasingly fragile. Asian markets followed suit, opening lower with large intraday volatility across the region. Concerns about a global recession continue to weigh heavily on investors’ minds, particularly as the commodity complex offers no reprieve—oil prices plunged to fresh four-year lows on fears of a steep demand collapse.

Gold, traditionally a safe haven, is fighting to hold above the 3000 psychological level. The safe-haven metal has been benefiting from the market’s defensive posture. In the currency space, Dollar extended its slide, joined by other risk-sensitive currencies including Aussie, Kiwi and Loonie. Sterling wasn’t spared either. Meanwhile, Euro, Yen, and Swiss Franc are holding firm as traders flock toward relative safety amid escalating trade tensions.

The key driver of current market anxiety is the formal implementation of US reciprocal tariffs today, with the most aggressive action aimed at China. An eye-watering 104% effective tariff rate now applies to Chinese imports, effectively escalating the bilateral conflict into a full-blown trade war. Adding fuel to the fire, US President Donald Trump signed an executive order tripling tariff rates on low-value Chinese packages shipped through international postal systems.

This rapidly escalating standoff between the world’s two largest economies marks a dangerous phase in global trade, with both nations seemingly unwilling to blink first. The economic fallout remains difficult to quantify at this stage, but the longer the impasse drags on, the more serious the risks to global growth and supply chains. Perhaps most troubling is the collateral damage to third-party nations, which are now caught between the crosshairs of US-China economic warfare.

More tariff action is on the horizon. Adding more fuel to the fire, Trump indicated during a political dinner that a major new round of tariffs targeting pharmaceuticals would be announced “very shortly.” These measures are expected to be aimed at shifting pharmaceutical production out of China and back into the US, with rates speculated to reach 25% or higher. The move has sparked concern not only about inflation in drug prices but also about global supply chain disruptions in the healthcare sector.

Elsewhere, Canada confirmed its retaliation, implementing 25% tariffs on US-made vehicles. Japan, another major trading partner, is bracing for heightened scrutiny. Finance Minister Katsunobu Kato noted that exchange rate policies may enter upcoming discussions, indicating that Washington’s pressure on currencies—particularly Yen—could be a brewing flashpoint.

Technically, an immediate focus in on 1.0741 in GBP/CHF as selloff accelerates further this week. Firm break there will solidify the case that corrective pattern from 1.0183 has already completed, be it counted as at 1.1675 or 1.1501. Larger down trend should then be ready to resume through 1.0183 (2022 low).

In Asia, at the time of writing, Nikkei is down -4.14%. Hong Kong HSI is down -1.43%. China Shanghai SSE is up 0.21%. Singapore Strait Times is down -2.44%. Japan 10-year JGB yield is down -0.024 at 1.255. Overnight, DOW fell -0.84%. S&P 500 fell -1.57%. NASDAQ fell -2.15%. 10-year yield rose 0.107 to 4.262.

RBNZ cuts 25bps, trade barriers as downside risk to both growth and inflation

RBNZ delivered a widely expected 25bps cut in the Official Cash Rate, bringing it to 3.50%. The policy statement highlighted that the recently announced global trade barriers create “downside risks to the outlook for economic activity and inflation” in New Zealand.

The central bank noted that with inflation close to the midpoint of its target range, it is in the “best position” to respond to economic shifts. RBNZ added it has “has scope to lower the OCR further as appropriate”, depending on how the impact of tariffs evolves.

This leaves the door wide open for further easing, particularly if global economic headwinds intensify or domestic data disappoints.

NZD/USD edged lower earlier today with broad risk aversion, but there is no particular selloff after RBNZ’s decision.

Technically, the breach of 0.5515 support suggests that recent fall from 0.6378 is resuming. Near term risk will stay on the downside as long as 0.5644 resistance holds. Next target is 61.8% projection of 0.6378 to 0.5515 from 0.5852 at 0.5319.

But more importantly, sustained trading below 0.5467 (2020 low) would confirm resumption of whole downtrend from 0.8835 (2014 high). That would pave the way to 61.8% projection of 0.7463 to 0.5511 from 0.6378 at 0.5172 in the medium term.

Fed’s Goolsbee: Tariff shock far exceeds expectations; Daly calls for caution

Chicago Fed President Austan Goolsbee and San Francisco Fed President Mary Daly both sounded cautious overnight amid rising uncertainty from the unfolding global tariff war.

Goolsbee highlighted the unexpected magnitude of the tariff impact, calling them a “way bigger” shock than anticipated. He likened them to a “negative supply shock” and acknowledged that Fed’s appropriate policy response is unclear.

He warned of ripple effects through slower consumer and business activity, especially in a post-pandemic economy still scarred by past inflationary surges.

Meanwhile, Daly struck a more measured tone, noting that while she is “a little concerned” about the inflationary effects of tariffs, she emphasized Fed’s current policy is well-positioned and policymarkers can “just tread slowly and tread carefully.”

“The thing that’s really important is you stay steady in the boat while you think about not what’s happening over the last two days, but the net effect of the slate of changes that any administration wants to take,” she added.

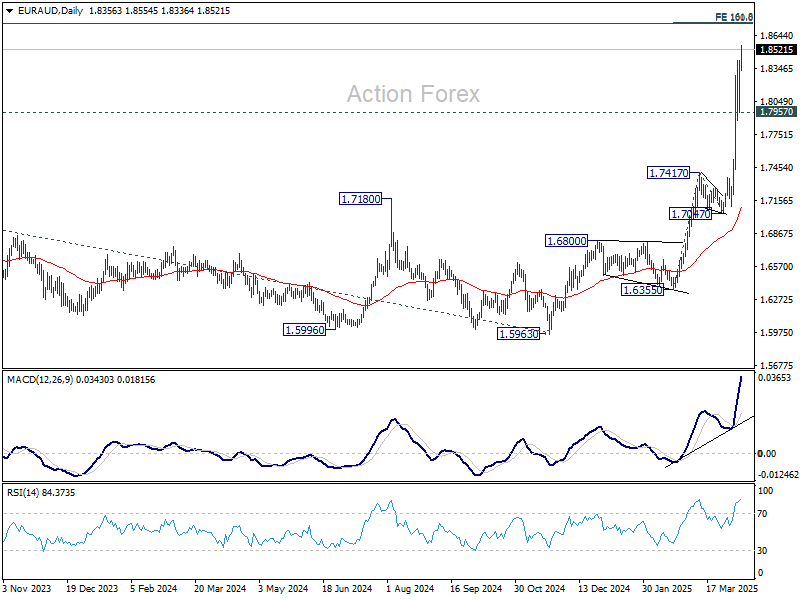

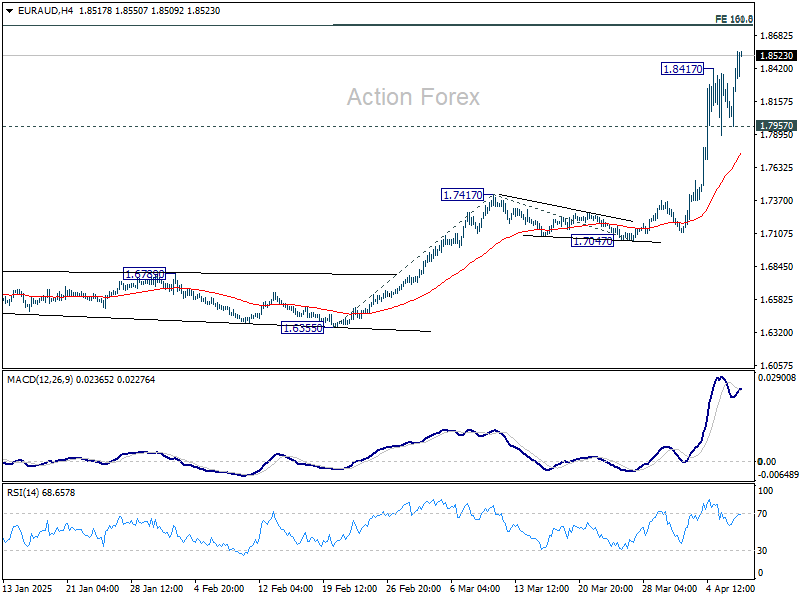

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.8097; (P) 1.8259; (R1) 1.8560; More…

EUR/AUD’s rally resumed after brief retreat and intraday bias is back on the upside. Current up trend should target 161.8% projection of 1.6355 to 1.7417 from 1.7047 at 1.8765 next. On the downside, below 1.7957 minor support could now indicate short term topping, possibly on bearish divergence condition in 4H MACD, and bring lengthier consolidations.

In the bigger picture, up trend from 1.4281 (2022 low) is in progress, and in reacceleration phase as seen in W MACD. Next target is 100% projection of 1.4281 to 1.7062 from 1.5963 at 1.8744. Firm break there will pave the way to 138.2% projection at 1.9806, which is close to 1.9799 (2020 high). Outlook will remain bullish as long as 1.7417 resistance turned support holds even in case of deep pullback.