Recovery in Dollar and Yen Capped, Downside Prospects in Euro

The forex markets are staying in mostly consolidation in Asian session. Recovery in Dollar and Yen is so far rather weak, capped by resilient market sentiment. S&P 500 closed at new record high while DOW was not far behind. Major Asian indexes are also trading higher after China’s Evergrande averted default for now after remitting funds for a key interest payment ahead of a 30-day grace period that ends tomorrow. As for the week, Kiwi and Aussie are so far the strongest, followed by Swiss Franc. Dollar, Yen and Loonie are the weakest. Euro is mixed but has the potential to weaken further in crosses.

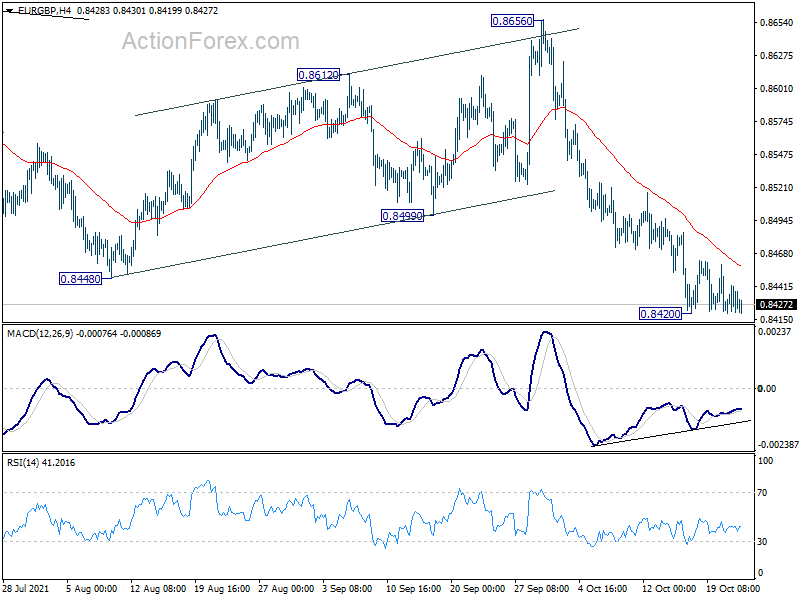

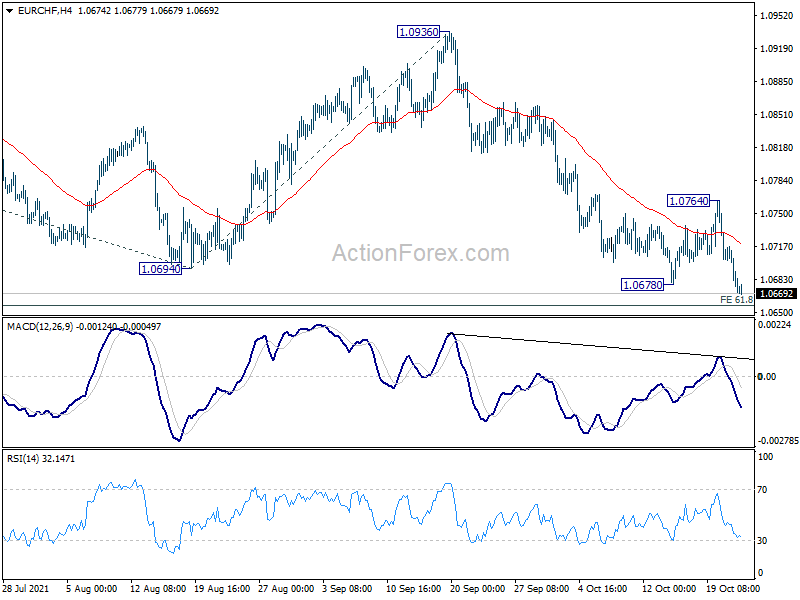

Technically, we’d continue to monitor 132.13 and 156.58 minor support levels in EUR/JPY and GBP/JPY. Break of these levels could signal more sustainable rebound in Yen. Also, as EUR/CHF has resumed recent fall through 1.0678 temporary low already, break of 0.8420 temporary low in EUR/GBP could signal more broad-based weakness in Euro.

{kind=link}

In Asia, at the time of writing, Nikkei is up 0.83%. Hong Kong HSI is up 0.51%. China Shanghai SSE is up 0.09%. Singapore Strait Times is up 0.29%. Japan 10-year JGB yield is up 0.0041 at 0.094. Overnight, DOW dropped -0.02%. S&P 500 rose 0.30% to new record at 4549.78. NASDAQ rose 0.62%. 10-year yield jumped 0.040 to 1.676.

Japan PMI manufacturing rose to 53.0, returned to growth

Japan PMI Manufacturing rose to 53.0 in October, up from September’s 51.5, above expectation of 51.6. PMI Services rose to 50.7, up from 47.8. PMI Composite rose to 50.7, up from 47.9.

Usamah Bhatti, Economist at IHS Markit, said: “Activity at Japanese private sector businesses returned to expansion territory at the start of the fourth quarter of 2021… Panel members commonly associated the slight recovery to a reduction in COVID-19 cases and looser pandemic restrictions.

“Private sector businesses also noted an increase in aggregate new business for the first time since April, assisted by a quicker rise in export orders. That said, firms continued to highlight sustained supply chain pressures and material shortages. As a result, input prices rose at the fastest rate in over 13 years. This contributed to the sharpest rise in output charges since July 2018.”

Also release, Japan all item CPI rose to 0.2% yoy in September, up from -0.4% yoy. CPI core (ex-food), rose to 0.1% yoy, up from 0.0% yoy. However, CPI core-core (ex-food, energy) was unchanged at -0.5% yoy.

Australia PMI composite rose sharply to 52.2, back in expansion

Australia PMI Manufacturing rose to 57.3 in October, up from September’s 56.8. PMI Services jumped sharply to 52.0, up from 45.5. PMI Composite rose to 52.2, up from 46.0. All are four-month highs.

Jingyi Pan, Economics Associate Director at IHS Markit, said: “Composite PMI indicated that the Australian economy is back in expansion in October as the easing of COVID-19 restrictions and plans for further opening up of the Australian economy restored confidence and rejuvenated economic activity…

“Higher demand however translated to greater strains on the supply chain… Meanwhile employment levels rose at a slower rate with reports of constraints when trying to hire staff. These are issues that may persist in the short- to medium- term for firms as they take their time to clear.”

RBA Lowe: Inflation not to sustain unless feeding through to wages

RBA Governor Philip Lowe at Universidad de Chile’s Conference that he didn’t expect the current rise in inflation to sustain, unless it led to higher wages growth.

“Is it going to reset expectations about what type of wage growth people should get, or will the spike dissipate and we will go back to the type of labour market outcomes we’ve seen before the pandemic?” Lowe said. “So there is quite a lot of uncertainty around that issue, but we are watching very carefully.”

BoE Pill: Nov MPC meeting is finely balanced, live

BoE’s new Chief Economist Huw Pill said UK inflation is likely to rise “close to or even slightly above 5 per cent” early next year. And, “that’s a very uncomfortable place for a central bank with an inflation target of 2 per cent to be.”

As for market expectation of a November rate hike, Pill declined to disclose his stance, and just said it’s “finely balanced”, “November is live”. And he added, “maybe there’s a bit too much excitement in the focus on rates right now”.

“The big picture is, I think, there are reasons that we don’t need the emergency settings of policy that we saw after the intensification of the pandemic,” said Pill. “The settings that we now have are supportive settings. The need for support has diminished, as this bridge has been built and largely traversed.”

Fed Bostic penciled in a rate hike in Q3, maybe early Q4 of 2022

Atlanta Fed Raphael Bostic told CNBC he has “penciled in” a rate increase in “late third, maybe early fourth” quarter of 2022. “Our experience from the pandemic has really frankly surprised to the upside,” he added “I’ve really adjusted my expectations moving forward.”

Bostic expected the supply chain disruptions to “last longer than we expected”. He said, “the labor markets are not going to get to equilibrium as quick as we hoped, but demand was also going to stay high and that combination was going to mean we’re going to have inflationary pressures.” It’s becoming “clearer and clearer” inflation pressure “is going to last into 2022.”

Looking ahead

UK will release retail sales and PMIs. Eurozone will release PMIs too. Later in the day, Canada will release retail sales while US will release PMIs.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0657; (P) 1.0689; (R1) 1.0705; More….

EUR/CHF’s break of 1.0678 support indicates resumption of larger down trend from 1.1149. Intraday bias is back on the downside for 61.8% projection of 1.1149 to 1.0694 from 1.0936 at 1.0655. Firm break there will pave the way to 100% projection at 1.0481, which is close to 1.5050 key long term support. On the upside, break of 1.0764 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

{kind=link}

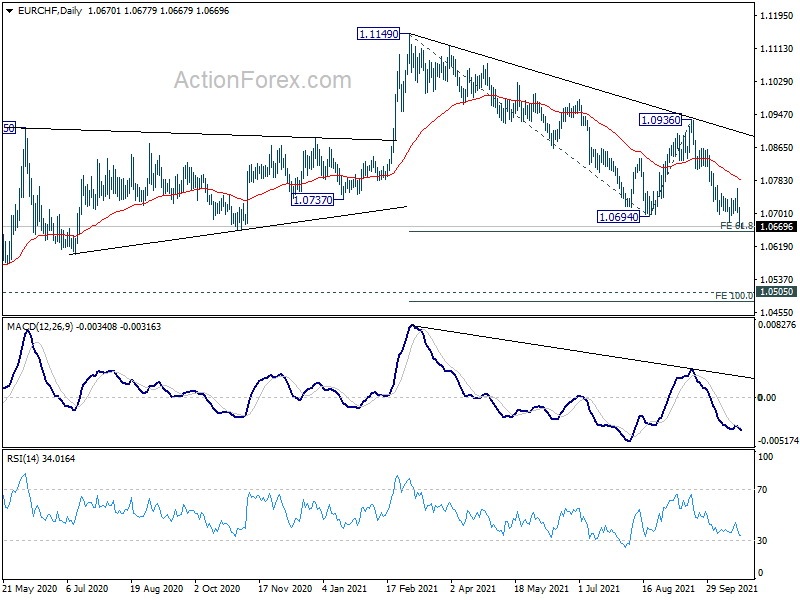

In the bigger picture, the rejection by 55 week EMA maintains medium term bearishness. Fall from 1.1149 (2021 high) is currently seen as the second leg of the patter from 1.0505 (2020 low) first. Hence, in case of deeper fall, we’d look for strong support from 1.0505 to bring rebound. However, sustained break of 1.0505 will resume the long term down trend from 1.2004 (2018 high). Also, medium term outlook will now be neutral at best as long as 1.0936 resistance holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:00 | AUD | Manufacturing PMI Oct P | 57.3 | 56.8 | ||

| 22:00 | AUD | Services PMI Oct P | 52.0 | 45.5 | ||

| 23:01 | GBP | GfK Consumer Confidence Oct | -17 | -16 | -13 | |

| 23:30 | JPY | National CPI Core Y/Y Sep | 0.10% | 0.10% | 0.00% | |

| 00:30 | JPY | Manufacturing PMI Oct P | 53.0 | 51.6 | 51.5 | |

| 06:00 | GBP | Retail Sales M/M Sep | 0.70% | -0.90% | ||

| 06:00 | GBP | Retail Sales Y/Y Sep | 0.00% | |||

| 06:00 | GBP | Retail Sales ex-Fuel M/M Sep | -1.20% | |||

| 06:00 | GBP | Retail Sales ex-Fuel Y/Y Sep | -0.90% | |||

| 07:15 | EUR | France Manufacturing PMI Oct P | 54.3 | 55 | ||

| 07:15 | EUR | France Services PMI Oct P | 55.3 | 56.2 | ||

| 07:30 | EUR | Germany Manufacturing PMI Oct P | 56.8 | 58.4 | ||

| 07:30 | EUR | Germany Services PMI Oct P | 55.2 | 56.2 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Oct P | 57.3 | 58.6 | ||

| 08:00 | EUR | Eurozone Services PMI Oct P | 55.4 | 56.4 | ||

| 08:30 | GBP | Manufacturing PMI Oct P | 55.6 | 57.1 | ||

| 08:30 | GBP | Services PMI Oct P | 54.5 | 55.4 | ||

| 12:30 | CAD | Retail Sales M/M Aug | -0.60% | |||

| 12:30 | CAD | Retail Sales ex Autos M/M Aug | -1% | |||

| 13:45 | USD | Manufacturing PMI Oct P | 60.5 | 60.7 | ||

| 13:45 | USD | Services PMI Oct P | 55.3 | 54.9 |