Tariffs and Doves Drive Dollar Lower, Split BoE to Cut – Action Forex

Dollar came under pressure again in Asian session, deepening this week’s selloff as traders digested a flood of tariff developments and dovish commentary from Fed officials. While Asian equity markets held steady with modest gains, the currency markets showed clearer directional bias, with the greenback slipping alongside Swiss Franc and Yen. Euro, Aussie and Kiwi firmed up, while risk sentiment in equities remained somewhat cautious but resilient.

Overnight, multiple Fed speakers leaned toward affirming a rate cut in September. While they avoided endorsing a faster pace of easing, the tone shift was clear: concern is growing about labor market softness, and inflation—while still elevated—is no longer the primary fear. That aligns with the Fed’s June dot plot, which already signaled two cuts in H2 2025. Additional dovish commentary in coming days may not shift pricing much unless it opens the door to three cuts.

Meanwhile, the macro backdrop was quickly overtaken by a fresh round of US tariff moves. President Donald Trump surprised markets by announcing a second 25% tariff on Indian imports, citing continued oil purchases from Russia. The latest round comes on top of duties scheduled to begin Thursday and reflects a dramatic escalation in secondary sanctions enforcement.

In parallel, Trump raised the possibility of targeting China next, depending on what unfolds in coming days. He said “It may happen” when asked if similar tariffs could be imposed on Beijing, after citing dissatisfaction with China’s handling of Russian trade ties. That adds extra uncertainty ahead of the August 12 deadline to finalize a long-term truce following the US-China framework agreement struck in May and updated in June.

In a signal of shifting geopolitical alignment, Indian Prime Minister Narendra Modi is reportedly planning a visit to China for the August 31 Shanghai Cooperation Organisation summit. It would be his first trip to Beijing in over seven years, and comes at a time when New Delhi’s ties with Washington are rapidly fraying. The move may indicate India is hedging its bets diplomatically amid escalating US trade threats.

Japan also found itself blindsided. According to a Kyodo report, contrary to earlier assumptions, the 15% US country-specific tariff on Japanese imports will not replace existing duties, but will stack on top of them. A White House official clarified that Tokyo had misunderstood the bilateral deal’s terms. That gives the EU preferential treatment over Japan and adds to Tokyo’s frustration. Japanese officials have not yet announced a response, but the development adds strain to what was seen as a stable alliance.

Switzerland, meanwhile, failed in its last-ditch effort to avert crippling 39% tariffs. President Karin Keller-Sutter returned from Washington without meeting Trump or any top trade official. With over 60% of Swiss exports affected, the government has called an emergency meeting to formulate a response.

The tech space is now at the center of the tariff war. Trump confirmed a 100% tariff on chip imports unless companies build in the US. While the criteria remain vague, this marks the most aggressive sector-specific measure yet. Apple’s new USD 100B investment pledge in the US was cited as validation of the policy. Major global chipmakers, including TSMC and Nvidia, are already expanding US production, but the tariff scope remains uncertain.

In Asia, at the time of writing, Nikkei is up 0.43%. Hong Kong HSI is up 0.50%. China Shanghai SSE is up 0.12%. Singapore Strait Times is up 0.81%. Japan 10-year JGB yield is down -0.009 at 1.492. Overnight, DOW rose 0.18%. S&P 500 rose 0.73%. NASDAQ rose 1.21%. 10-year yield rose 0.024 to 4.220.

Fed doves gain ground as Cook, Collins highlight drag from uncertainty

In a panel discussion overnight, Fed Governor Lisa Cook described July’s weaker-than-expected jobs report as “concerning” and noted that the pattern of downward revisions to payroll figures was “somewhat typical of turning points.”

Cook warned that uncertainty is now acting like a tax on businesses, with executives spending more time managing ambiguity than making forward-looking decisions. “This is deadweight loss,” she said.

Boston Fed President Susan Collins supported that view, stating the uncertainty burden is “top of mind” for firms across sectors. She pointed out that the effects extend beyond capital spending, with many businesses now hesitant to adjust pricing strategies due to a lack of visibility. “There’s still a wait-and-see,” Collins said.

The shared emphasis from two Fed officials underscores how economic ambiguity is increasingly viewed as a constraint on both employment and inflation dynamics. While neither Cook nor Collins offered direct policy guidance, their comments will reinforce expectations that the Fed is growing more open to easing, particularly if labor and business activity remain sluggish into the fall.

Fed’s Daly: Rate cut likely soon as labor market risks mount

San Francisco Fed President Mary Daly said overnight that she expects the central bank will need to cut interest rates “in the coming months,” citing a gradually cooling economy and persistent downside risks in the labor market. “I would see additional slowing as unwelcome,” Daly warned, adding that the labor market tends to “fall quickly and hard” once momentum is lost.

Daly also downplayed the inflationary impact of US tariffs, saying they pose only a short-term threat. Excluding tariff effects, she noted, inflation has been “gradually trending down,” and should continue to ease given restrictive policy and moderating demand.

Fed’s Kashkari reaffirms case for two cuts, says economy slowing

Minneapolis Fed President Neel Kashkari reiterated his view that two rate cuts in 2025 remain a reasonable base case, telling CNBC overnight that “the economy is slowing — and that means, in the near term, it may become appropriate to start adjusting the federal-funds rate.” The comment aligns with growing expectations for a September cut, especially after last week’s soft jobs data.

However, Kashkari’s remarks are broadly consistent with the position he laid out in June, when he wrote in an essay that tariff impacts may be more muted than feared due to corporate adaptations and exemptions. At the time, he argued that these offsetting forces would allow inflation to ease gradually, supporting a measured policy adjustment.

In both June and today’s comments, Kashkari has signaled a preference for patience but also preparedness. Barring any surprises, his base case still assumes a September move, followed by another later in the year.

RBNZ survey signals one more cut, then long pause ahead

RBNZ’s August Survey of Expectations suggests the central bank will likely cut rates only once more in 2025, but the outlook beyond that remains cautious. The OCR is forecast to decline from 3.25% to 3.02% by September 2025 — consistent with a single 25bps move, likely in this month’s meeting. By June 2026, it’s seen at 2.86%, implying a second cut is possible in H1 2026, but far from assured.

Inflation expectations continue to ease gradually. One-year-ahead CPI forecasts slipped from 2.41% to 2.37%, while two-year-ahead projections fell marginally from 2.29% to 2.28%. Wage inflation expectations were mixed, with one-year views dropping to 2.61% while two-year expectations rose to 2.88%, implying confidence that wage pressures will not reignite inflation risks over the medium term.

The unemployment outlook also improved slightly, with expectations for joblessness falling across all time horizons. Despite soft growth conditions, respondents see GDP rising 1.66% over the next year and 2.16% the year after. Taken together, the survey points to a slow-moving easing cycle ahead, starting with one cut likely later this year, followed by a potentially long pause.

Strong oil, soybean demand drives China import spike, cuts surplus

China’s July trade data surprised to the upside, with exports rising 7.2% yoy and imports jumping 4.1% yoy — the largest annual gain in over a year. Strong commodity demand underpinned the figures, as soybean imports surged 18.5% yoy and crude oil shipments rose 11.5% yoy.

The trade surplus came in at USD 98.2 B, narrower than the expected USD 107.9B, suggesting stronger domestic demand helped balance trade flows.

While the numbers offer a positive signal for global demand, investors remain focused on the looming August 12 deadline to finalize a lasting trade agreement with the US. The strong data may give Beijing some negotiating leverage, but uncertainty remains high.

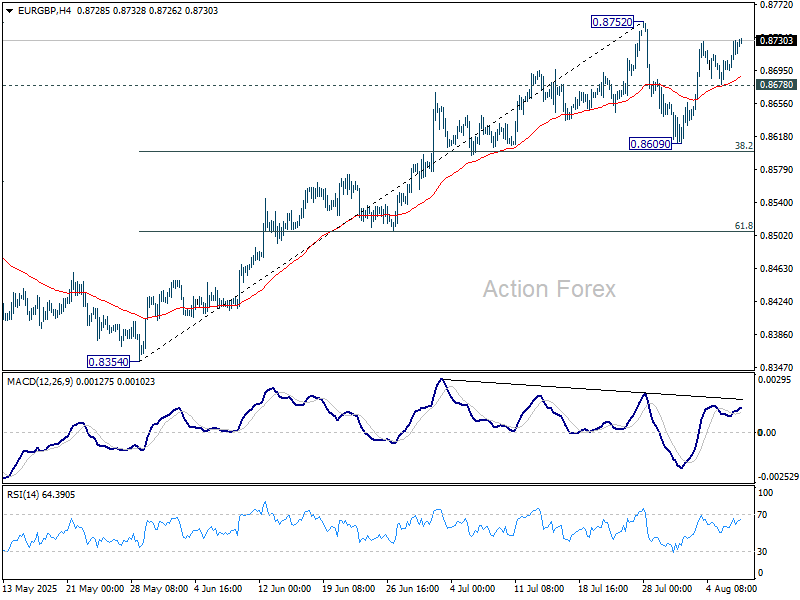

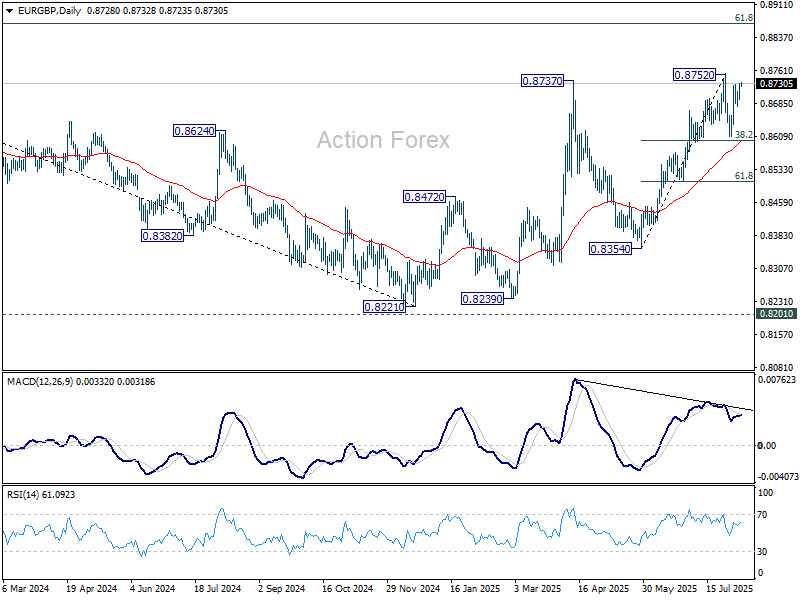

BoE to cut as doves, hawks, and moderates collide, EUR/GBP set for wild swings

BoE is set to cut interest rates by 25bps to 4.00% today, continuing its steady easing cycle that began a year ago. The decision would mark the fifth rate cut since last August. Crucially, today’s announcement will also include updated economic forecasts that could shed light on how far the BoE is willing—or able—to go with further easing.

With UK GDP shrinking in both April and May, the need for additional support is evident. The IMF recently warned that UK economic growth could stall at just 0.1% for both Q3 and Q4, setting the stage for stagflation.

However, inflation remains a concern. Headline CPI rose 3.6% in June—well above the 2% target—and any upward revision in today’s CPI forecasts could tighten the BoE’s policy space. If projections inch toward 4%, it would significantly complicate any aggressive easing path.

The decision is also likely to see a notable division within the Monetary Policy Committee. Hawks like Huw Pill and Catherine Mann may vote to hold rates, while doves such as Swati Dhingra and Alan Taylor could push for a deeper 50bps cut. Even Deputy Governor Dave Ramsden is seen as a potential dovish swing vote. Any unexpected alignment or dissent could shift market pricing for future BoE moves.

Volatility in EUR/GBP is expected with the rate decision. Technically, it is currently extending the rebound from 0.8609 towards 0.8752 resistance. Strong break there will confirm resumption of whole rally from 0.8221 towards 0.8867 fibonacci level. However, break of 0.8678 support will extend the corrective pattern from 0.8752 towards 0.8609 support again.

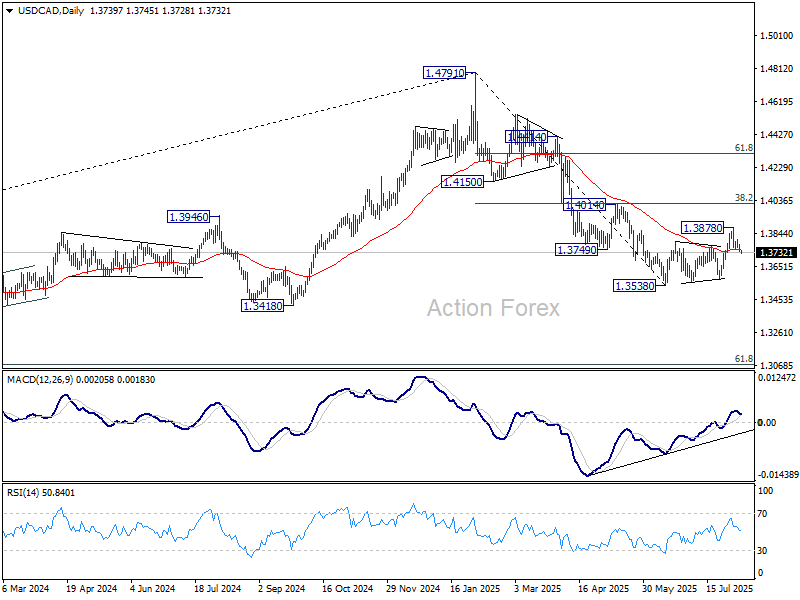

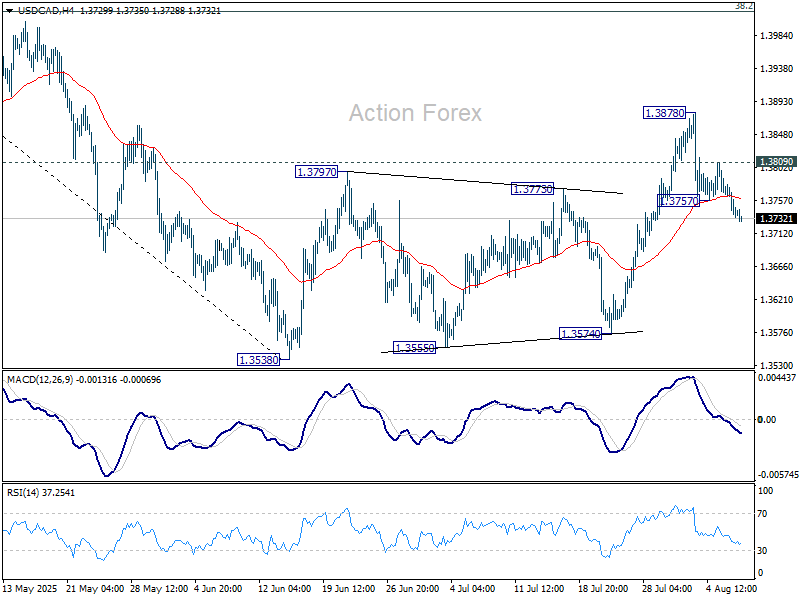

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3724; (P) 1.3752; (R1) 1.3769; More…

USD/CAD’s fall from 1.3878 resumed by breaking through 1.3757 temporary low and intraday bias is back on the downside. Current development suggests that corrective rebound from 1.3538 has completed with three waves up to 1.3878. Deeper fall should be seen to retest 1.3538 low. On the upside, however, above 1.3809 will dampen this view and turn bias neutral again.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.