Trade Tensions Drag Dollar While Oil Jumps on OPEC+ Hold – Action Forex

Risk sentiment remains fragile as the US session gets underway, with equity markets under pressure from renewed tariff threats. European stocks are particularly heavy after US President Donald Trump threatened to double tariffs on imported steel. UK equities, however, are finding some support from Prime Minister Keir Starmer’s announcement of increased defense spending.

In the currency markets, Dollar is under broad pressure, currently the weakest performer of the day as traders react to the heightened trade uncertainty again. Loonie and Swiss Franc are also underperforming. Kiwi leads gains, followed by Yen and Aussie. Sterling and Euro sit in the middle.

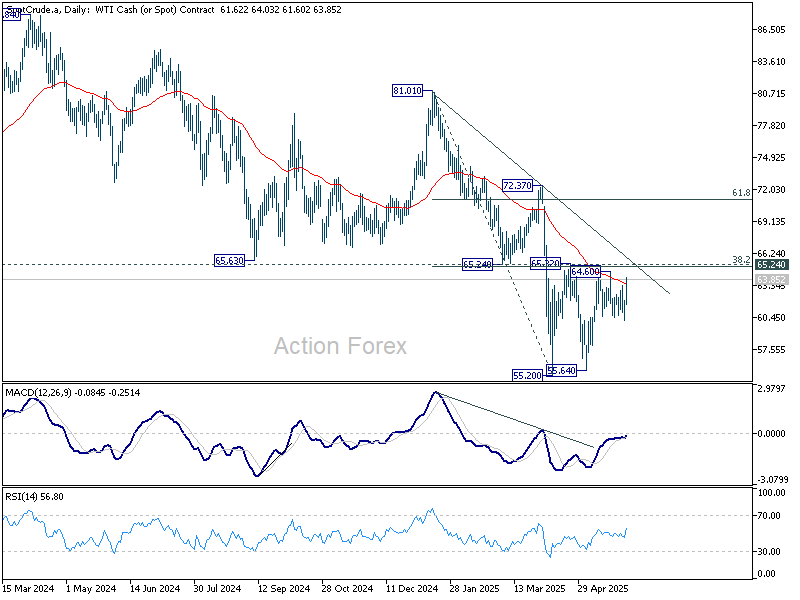

Meanwhile, oil prices have jumped after OPEC+ confirmed it would maintain output increases in July at pace of 411k barrels per day. Markets had been wary of a possible larger hike, as hinted by sources late last week. That outcome would have likely sparked a sharp bearish gap on Monday’s open. The restraint from OPEC+ has thus supported a modest rebound in crude.

Technically, despite the rebound, WTI crude remains capped below key cluster resistance at 65.24 (38.2% retracement of 81.01 to 55.20 at 65.05. As long as this resistance zone holds, outlook will stay bearish for down trend resumption through 55.20 at a later stage. Nevertheless, firm break of 65.05/24 would bring strong rally to 61.8% retracement at 71.15, with risk of bullish trend reversal.

In Europe, at the time of writing, FTSE is up 0.08%. DAX is down -0.45%. CAC is down -0.58%. UK 10-year yield is up 0.025 at 4.674. Germany 10-year yield is up 0.036 at 2.541. Earlier in Asia, Nikkei fell -1.30%. Hong Kong HSI fell -0.57%. Singapore Strait Times fell -0.10%. Japan 10-year JGB yield rose 0.004 to 1.509.

UK PMI manufacturing finalized at 46.4, with tentative signs of stabilization

UK manufacturing activity remained in contraction in May, with PMI finalized at 46.4, up modestly from April’s 45.4.

The data indicate that the sector continues to face “major challenges,” according to S&P Global’s Rob Dobson, citing turbulent domestic and global conditions, trade uncertainty, subdued client confidence, and increased wage costs tied to tax changes.

Still, there are early signs that the worst of the downturn may be easing. The indexes for output and new orders have risen for two consecutive months and were stronger than the initial flash estimates, hinting at possible stabilization.

However, Dobson warned that the sector could either steady or slip further depending on how trading conditions evolve in the coming months.

Eurozone PMI manufacturing finalized at 49.4, recovery progressing

Eurozone PMI manufacturing was finalized at 49.4 in May, up from April’s 49.0 and marking the highest level in 33 months.

Production increased across all four major economies: Germany, France, Italy, and Spain, supporting economist Cyrus de la Rubia’s view that the recovery is gaining traction.

De la Rubia also noted that output has now risen for three straight months, reinforcing the view that the recovery is gaining traction. Historical data suggests a 72% chance of another output increase next month.

Falling input costs, driven by lower energy prices, have enabled manufacturers to cut selling prices again, offering the ECB more flexibility for its expected interest rate cuts.

However, the outlook remains clouded by external risks, particularly the threat of higher US tariffs on EU goods. Any escalation in transatlantic trade tensions could quickly derail the fragile rebound.

Swiss GDP grew 0.5% in Q1, pharma exports surge on tariff frontloading

Switzerland’s GDP expanded by 0.5% qoq in Q1, beating market expectations of 0.4% qoq. When adjusted for the impact of major sporting events, GDP growth came in even stronger at 0.8% qoq. The State Secretariat for Economic Affairs noted that the services sector posted broad-based gains and domestic demand remained firm, contributing to the overall solid performance.

A standout was the chemical and pharmaceutical sector, which surged 7.5% in the quarter, driven by a sharp rise in pharmaceutical exports. This lifted overall manufacturing output by 2.1% and goods exports by 5.0%. Notably, exports to the US jumped significantly, suggesting possible front-loading in anticipation of evolving US trade policy.

Japan’s PMI manufacturing finalized at 49.5, firms eye recovery despite trade headwinds

Japan’s PMI Manufacturing was finalized at 49.5 in May, up from April’s 48.7. S&P Global’s Annabel Fiddes noted that business conditions “moved closer to stabilisation,” as declines in sales eased and firms reported improved hiring activity.

Global trade tensions stemming from US tariffs continue to weigh on demand, with businesses citing “increased client hesitancy” and weaker orders.

Despite persistent external challenges around tariffs, sentiment around future output improved, and hiring rose at the fastest pace in over a year.

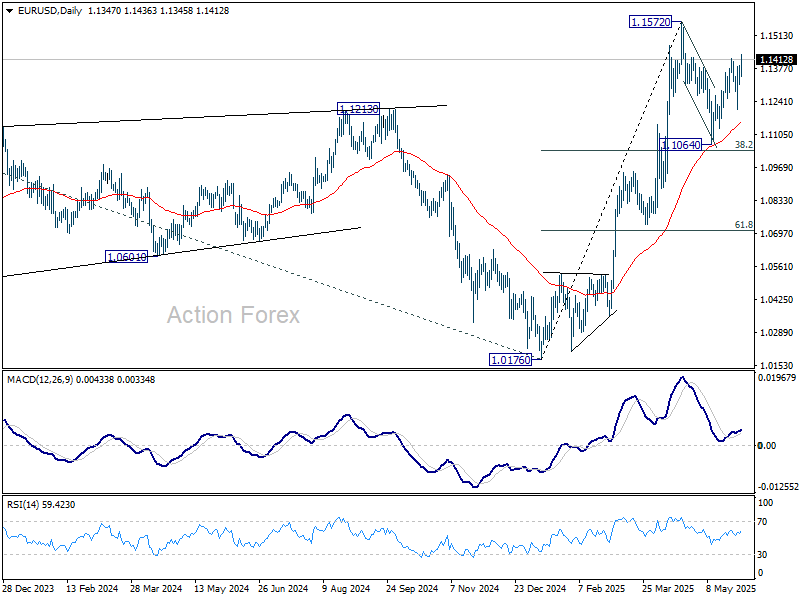

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1310; (P) 1.1350; (R1) 1.1387; More…

Intraday bias in EUR/USD is back on the upside as rebound from 1.1064 resumed by breaking through 1.1417. Further rise would be seen to retest 1.1572. Strong resistance could be seen there to limit upside at first attempt. Below 1.1311 minor support will turn intraday bias neutral first. Nevertheless, decisive break of 1.1572 will confirm larger up trend resumption.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0856) holds.